INTERESTED IN THIS RESEARCH?

Contact our analysts for inquiries, samples, and expert insights.

REPORT OUTLOOK

| Market Size | CAGR | Dominating Region |

|---|---|---|

| USD 78.55 billion by 2029 | 5.11% | Asia Pacific |

| By Material | By Product Type | By Application | By End-User |

|---|---|---|---|

|

|

|

• Hospitals |

SCOPE OF THE REPORT

Abrasives Market Overview

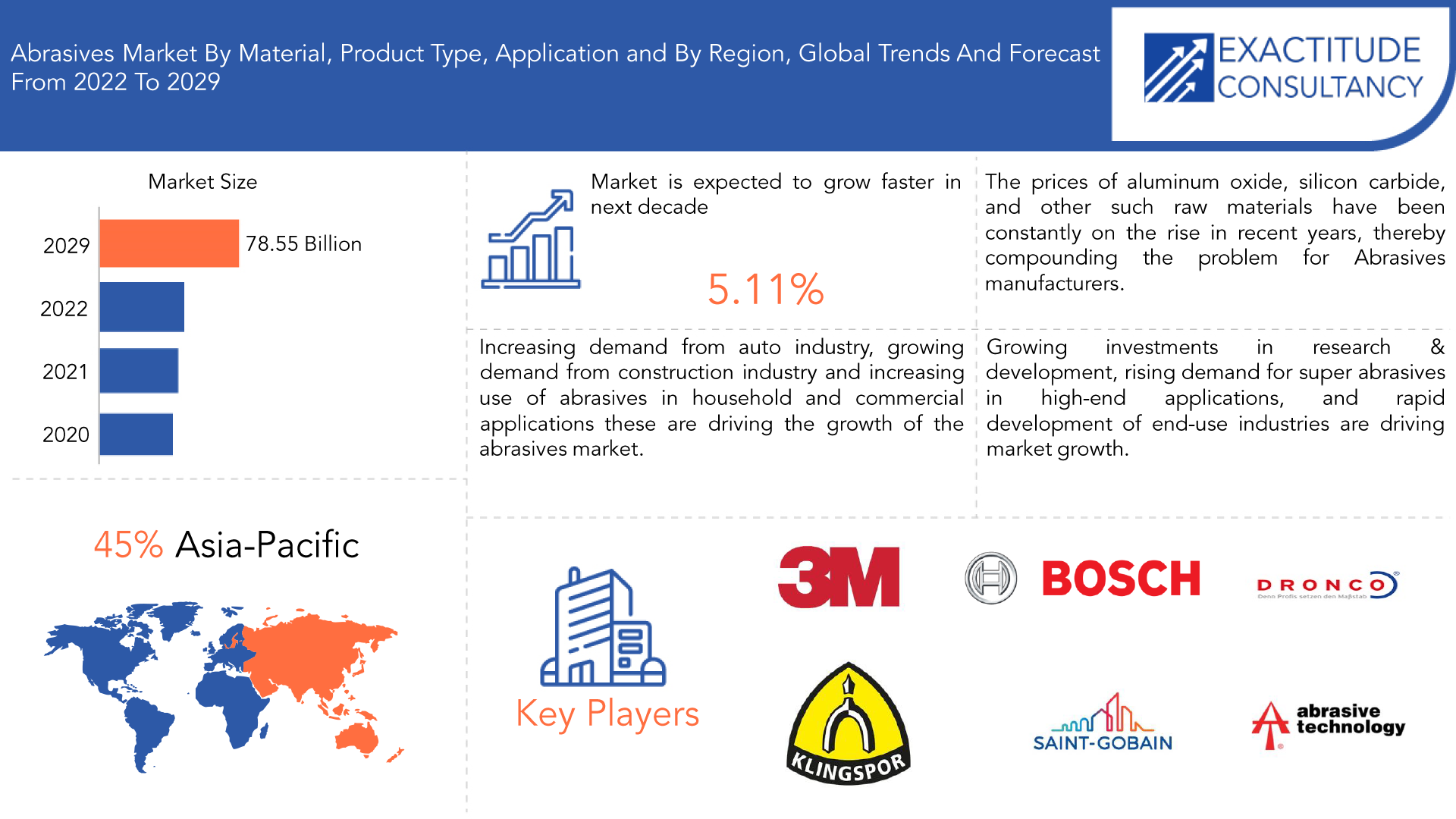

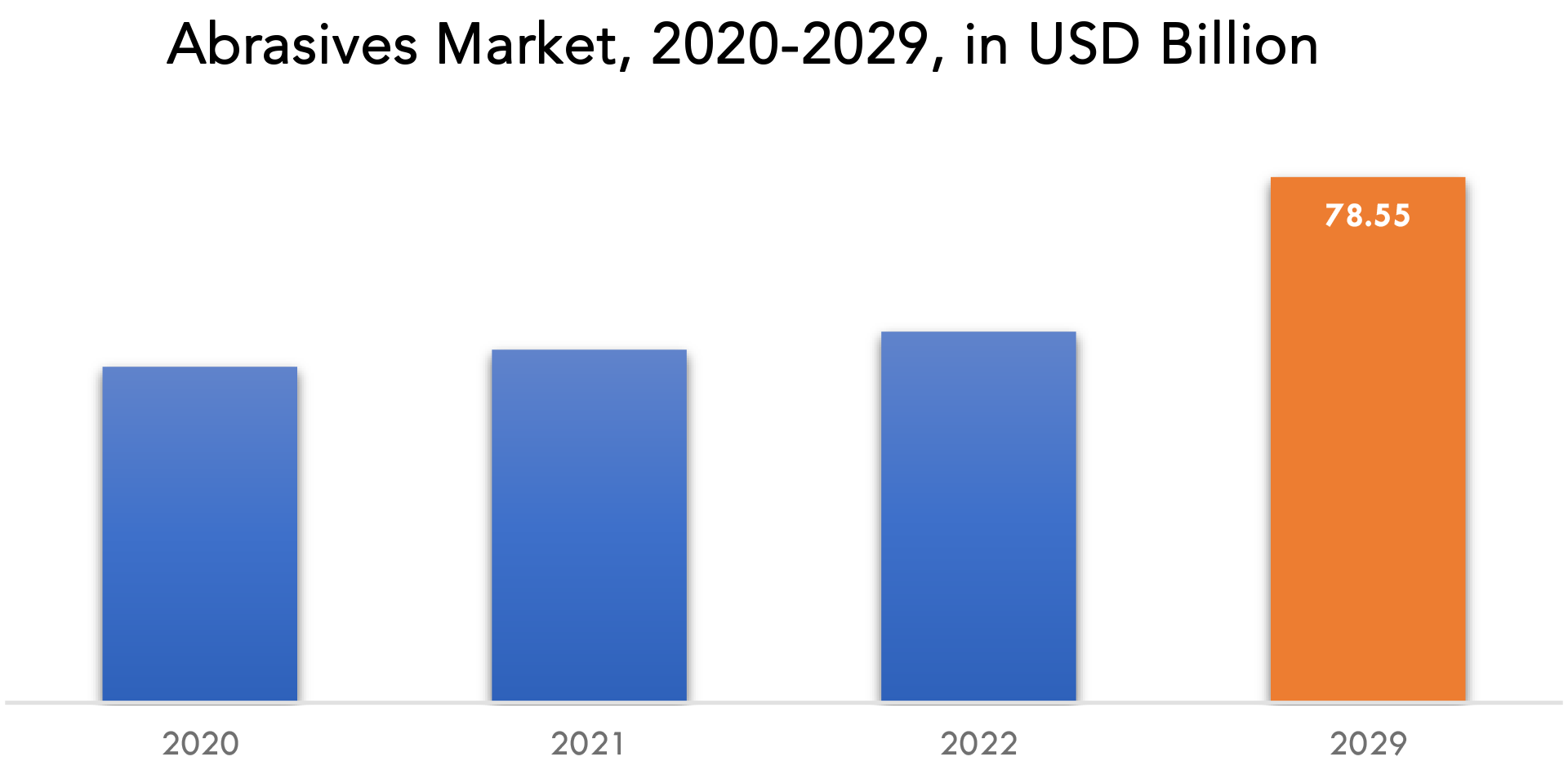

The global abrasives market is projected to reach USD 78.55 billion by 2029 from USD 50.20 billion in 2020, at a CAGR of 5.11 % from 2022 to 2029.

Abrasives materials are hard crystals that can be found in nature or created artificially. This material is typically minerals that are used to finish or shape work pieces by tearing, rubbing, or causing wear. Boron nitride, silicon, aluminum, diamond, glass, and walnut shells are the most used abrasives. Because the abrasives grains can penetrate the hardest metals and alloys, these are specifically used in metalworking. Because of their hardness, abrasives materials are ideal for working with the hardest materials, such as glass, plastics, and stones. It’s also used on soft materials like rubber and wood.

Arking is increasing due to the numerous advantages they provide. Abrasives improve finished product quality, increase production efficiency, and lower costs. The increased use of abrasives in metalworking is also propelling market growth. Abrasives are used in many metalworking processes, including grinding, deburring, polishing, and finishing. Abrasives improve the finished product’s quality by providing a superior surface finish. They also boost production efficiency by shortening cycle times and reducing tool wear. Abrasives also reduce production costs by extending the life of tools and machines.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2029 |

| Base year | 2021 |

| Estimated year | 2022 |

| Forecasted year | 2022-2029 |

| Historical period | 2018-2020 |

| Unit | Value (USD Billion), Volume (Kilotons) |

| Segmentation | By Material, By Product Type, By Application, By Region. |

| By Material |

|

| By Product Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

The abrasives market is vast, with growing demand in emerging economies such as India and Southeast Asian countries. The abrasives market is expanding due to increased demand for high-quality surface finishes and precision machining. Furthermore, the growing demand for lightweight materials in the aerospace and automotive industries is propelling the market forward. The market’s scope is expected to broaden as demand for environmentally friendly abrasives grows.

These include increased growth in the automotive and aerospace industries, increased home improvement spending, and increased use of abrasives in metalworking. The automotive and aerospace industries are major drivers of the Abrasives Market. These industries require abrasives for a variety of applications such as finishing, polishing, and grinding. The automotive industry is expected to grow slowly in the coming years, whereas the aerospace industry is expected to grow rapidly. This will increase demand for abrasives. Another important driver of the Abrasives Market is the home improvement industry. Homeowners are increasingly undertaking renovation and improvement projects that necessitate the use of abrasives.

Rapid urbanization, inflating income levels and the rising global population have boosted the sales of automobiles worldwide. This, along with the increasing utilization of abrasives for reducing CO2 emissions of high-performance engines and noise levels in automobiles, is strengthening the growth of the market. Moreover, the thriving electronics and manufacturing industries act as another growth-inducing factor. Abrasives are used in these industries to scrape the metal in small amounts for manufacturing semiconductors and other electronic equipment with precision. The automotive industry is the largest end-user of Abrasives, accounting for over 50% of the global demand. The aerospace industry is the second-largest end-user of Abrasives, accounting for around 15% of the global demand. Abrasives products are needed in large quantities by both industries due to the nature of their operations. These industries are forecast to continue to grow at a healthy rate over the next few years, which will drive up demand for abrasives products. In addition, new applications for Abrasives are constantly being developed in both industries, which will further boost demand. The home improvement sector is another key driver of the abrasives Market.

The competition from low-cost abrasives products made in nations with reduced labor costs is one of the major obstacles. These inexpensive goods can affect production quality because they frequently fall short of the high standards set by expensive abrasives. The fluctuating cost of the raw materials used to make abrasives goods is another issue that the abrasives market must deal with. Because of the rising demand and supply chain disruptions brought on by geopolitical variables, the prices of raw materials used to make abrasives, such as silicon carbide and aluminum oxide, have been fluctuating. Abrasives makers find it challenging to plan their production schedules and pricing strategies as a result of this volatility.

The creation of environmentally friendly abrasives products is one of the key opportunities in the abrasives industry. Abrasives producers now have the chance to create new products that satisfy consumers’ increasing demand for abrasives that are less damaging to the environment. Businesses that can create and sell sustainable abrasives goods have a great chance to seize a developing market niche.

Abrasives Market Segment Analysis

The global abrasives market is segmented by material, product, application, and region.

Based on material, the abrasives market is segmented into natural, synthetic. Synthetic abrasives account for most of the abrasives market. Synthetic abrasives are a raw material or chemical precursor treatment product. These materials include synthetic diamonds, silicon carbide, and alumina. Natural abrasives are widely used in a variety of household, industrial, and technological operations as a result of the growing consumer shift towards organic produce. These include corundum, diamond, and emery, which can be mined and prepared for use with less variation because they occur naturally. The increasing use of this type of product in the automotive sector is the primary driver of market growth.

The natural segment of the Abrasives Market is estimated to have held the second-largest share in 2021 in terms of value. Over the forecast period, this segment is expected to grow at a moderate rate. Natural abrasives have been used for many years in a variety of applications such as transportation, construction, and manufacturing. Alumina, silicon carbide, and other raw materials are commonly used in the production of natural abrasives. There are numerous advantages to using natural abrasives, which is contributing to the segment’s growth. When compared to synthetic counterparts, some of these advantages include superior finishing, longer life, and improved heat resistance.

Based on product type, the abrasives market is segmented into bonded, coated, super. Coated Abrasives had the largest market share in 2021 and is expected to grow at the fastest CAGR during the forecast period. Coated Abrasives are in high demand due to their wide range of applications in a variety of end-use industries, including automotive and transportation, metal fabrication, machinery, electronics, and woodworking. Abrasives with coatings are made up of an abrasives grain, a backing material, and a binder resin. They are used for metals, plastics, composites, aluminum alloys, glass ceramics, and stone grinding, sanding, polishing, and finishing operations.

Bonded abrasives are used for a variety of tasks such as grinding, cutting, polishing, and finishing. In 2021, this segment held the second-largest market share in the Abrasives Market. Bonded Abrasives are in high demand due to their flexibility and versatility. Bonded abrasives come in a variety of shapes and sizes, making them suitable for use on a wide range of surfaces. Bonded Abrasives can also be custom-made to meet the specific needs of customers. Bonded abrasives are also simple to use and require little training. One of the key factors driving the growth of this market segment is the increased use of bonded Abrasives in the automotive sector. Super abrasives are in high demand in applications such as precision edging in automotive, construction, and woodworking tools. Grinding wheels or rectification tools are used in the automotive and construction industries to shape too fragile or too hard materials such as glass, ceramic compounds, and others.

Based on application, the abrasives market is segmented into automotive, electrical & electronics, metal fabrication, machinery, and others. Metal fabrication is the market’s largest contributor and is expected to grow at a healthy CAGR during the forecast period. This type of fabrication is used to create metal structures by bending, cutting, and assembling them. Cut-off saws, also known as chop saws, are used to shape metals using this item. Steel-cutting abrasives discs are used in these saws. Additional metal fabrication products include fiber discs and flap discs, which are primarily used for smoothing and grinding metal surfaces.

The automotive industry is expected to expand rapidly. Abrasives material is typically used as grinding wheels and grinding segments to smooth or roughen the surface for polishing, fitting, or painting. The increasing applications for deburring, cleaning, and repairing auto parts will drive segment growth.

Abrasives Market Players

The global abrasives market key players include 3M Company, Robert Bosch GmbH, DRONCO GmbH, Klingspor AG, Saint-Gobain Abrasives, Inc., Carborundum Universal Limited, Asahi Diamond Industrial Co., Ltd., Fujimi Incorporated, Cabot Microelectronics Corporation., Ltd., Abrasives Technology, Inc., Noritake Co., Limited, Deerfos Co., Ltd., Sia Abrasives Industries AG.

Recent News

3 February 2022 – Carborundum Universal Ltd (CUMI), through its subsidiary CUMI Abrasives GmbH, based in Germany, announced a contract to purchase 100% stake in RHODIUS Abrasives. This acquisition is expected to enhance the geographical expanse of the company.

Oct. 28, 2021: 3M, which pioneered the car industry’s paint repair process over a century ago, was once again established the bar for the future of automatic paint repair. For their groundbreaking invention, the 3MTM Finesse-itTM Robotic Paint Repair System team earned one of the industry’s most distinguished awards.

Who Should Buy? Or Key stakeholders

- Regional agencies and research organizations

- Investment research firm

- Government Bodies

- Technology Investors

- Investors/Shareholders

- Automobile OEMs

- Construction companies

- Metal Fabrication vendors

- End-Users

Abrasives Market Regional Analysis

The abrasives market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).

- North America: includes the US, Canada, Mexico

- Asia Pacific: includes China, Japan, South Korea, India, Australia, ASEAN, and Rest of APAC

- Europe: includes UK, Germany, France, Italy, Spain, Russia, and Rest of Europe

- South America: includes Brazil, Argentina, and Rest of South America

- Middle East & Africa: includes Turkey, UAE, Saudi Arabia, South Africa, and Rest of MEA

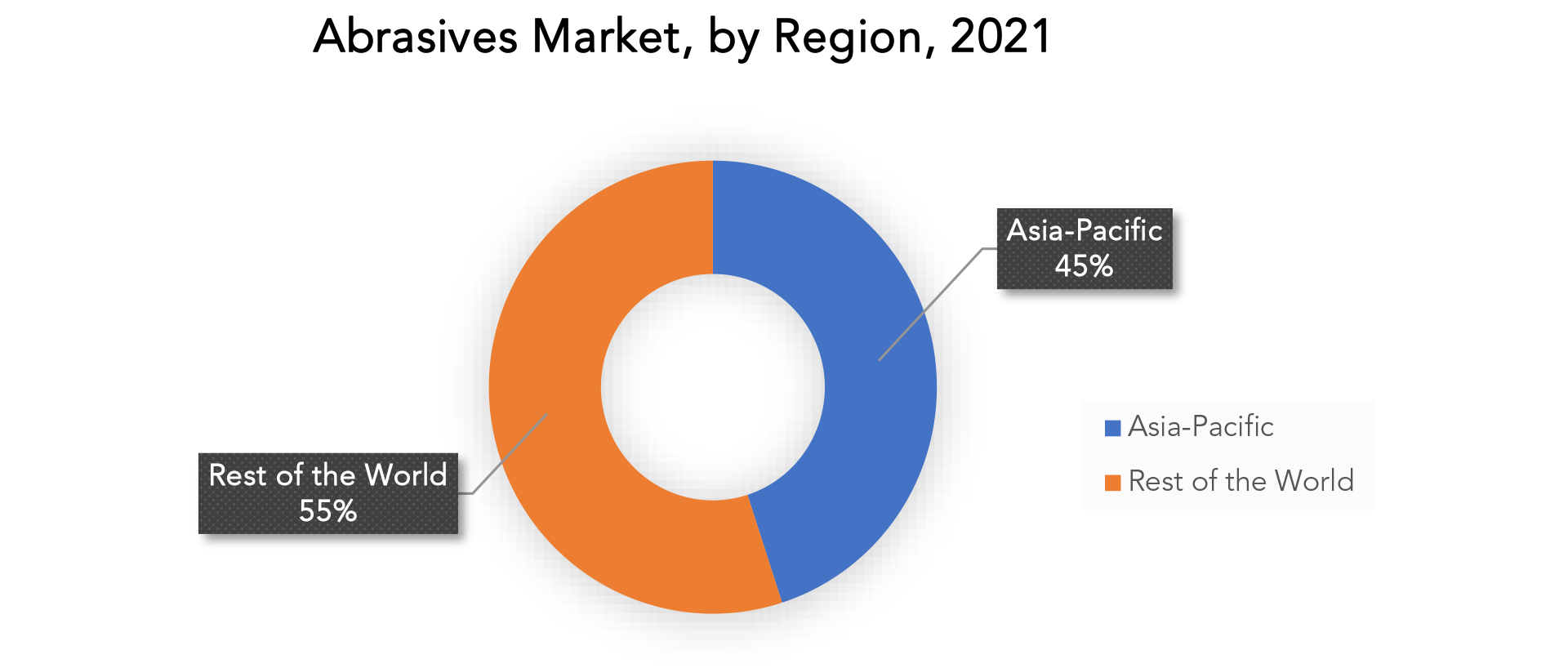

The Asia Pacific region is the market’s largest contributor and is expected to grow at a healthy CAGR during the forecast period. This expansion can be attributed to increased regional economic development, rapid industrialization, and growth in automotive, metal fabrication, and machinery. India, China, Japan, and South Korea are the major contributors to regional market growth. Furthermore, the growing automotive sectors in India and China are important factors for regional market growth. According to Statista, China has one of the world’s largest automobile markets.

North America is expected to see dynamic growth in the abrasives market during the forecast period because of its massive aerospace and defence industries. Furthermore, the presence of large automotive manufacturers and machinery industries in the United States is a major factor driving North America’s abrasives market growth. Europe is expected to experience significant growth in the Abrasives video market during the forecast period. Automobile production is concentrated in Europe, which raises overall product consumption. Furthermore, a high level of cleaning and maintenance services for these cars is a significant factor that will foster market expansion in the area.

Mexico, Argentina, and Brazil are the major countries in South America that will support market growth. The region’s growth can be attributed to the expanding automotive, aerospace, construction, and furniture industries. During the forecast period, the Middle East and Africa market is expected to grow significantly. Rising demand for woodworking, solid surface grinding and polishing, and metal fabrication in the region will support market growth in the coming years.

Key Market Segments: Abrasives Market

Abrasives Market by Material, 2020-2029, (USD Billion) (Kilotons)

- Natural

- Synthetic

Abrasives Market by Product Type, 2020-2029, (USD Billion) (Kilotons)

- Bonded

- Coated

- Super

Abrasives Market by Application, 2020-2029, (USD Billion) (Kilotons)

- Automotive

- Electrical & Electronics

- Metal Fabrication

- Machinery

- Others

Abrasives Market by Region, 2020-2029, (USD Billion) (Kilotons)

- North America

- Europe

- Asia Pacific

- South America

- Middle East And Africa

Important Countries In All Regions Are Covered

Exactitude Consultancy Services Key Objectives

- Increasing sales and market share

- Developing new technology

- Improving profitability

- Entering new markets

- Enhancing brand reputation

Key Question Answered

- What is the expected growth rate of the abrasives market over the next 7 years?

- Who are the major players in the abrasives market and what is their market share?

- What are the end-user industries driving demand for market and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-Pacific, Middle East, and Africa?

- How is the economic environment affecting the abrasives market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the abrasives market?

- What is the current and forecasted size and growth rate of the global abrasives market?

- What are the key drivers of growth in the abrasives market?

- What are the distribution channels and supply chain dynamics in the abrasives market?

- What are the technological advancements and innovations in the abrasives market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the abrasives market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the abrasives market?

- What are the product offerings and specifications of leading players in the market?

- What is the pricing trend of abrasives in the market and what is the impact of raw material prices on the price trend?

Table of Content

- INTRODUCTION

- MARKET DEFINITION

- MARKET SEGMENTATION

- RESEARCH TIMELINES

- ASSUMPTIONS AND LIMITATIONS

- RESEARCH METHODOLOGY

- DATA MINING

- SECONDARY RESEARCH

- PRIMARY RESEARCH

- SUBJECT-MATTER EXPERTS’ ADVICE

- QUALITY CHECKS

- FINAL REVIEW

- DATA TRIANGULATION

- BOTTOM-UP APPROACH

- TOP-DOWN APPROACH

- RESEARCH FLOW

- DATA SOURCES

- DATA MINING

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET OUTLOOK

- MARKET DRIVERS

- MARKET RESTRAINTS

- MARKET OPPORTUNITIES

- IMPACT OF COVID-19 ON ZERO LIQUID DISCHARGE SYSTEMS MARKET

- PORTER’S FIVE FORCES MODEL

- THREAT FROM NEW ENTRANTS

- THREAT FROM SUBSTITUTES

- BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER OF CUSTOMERS

- DEGREE OF COMPETITION

- INDUSTRY VALUE CHAIN ANALYSIS

- GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET OUTLOOK

- GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION, THOUSAND UNITS), 2020-2029

- CONVENTIONAL

- HYBRID

- GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION, THOUSAND UNITS), 2020-2029

- PRETREATMENT PROCESS

- FILTRATION PROCESS

- EVAPORATION PROCESS

- CRYSTALLIZATION PROCESS

- GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION, THOUSAND UNITS), 2020-2029

- REVERSE OSMOSIS (RO)

- ULTRAFILTRATION (UF)

- EVAPORATION

- CRYSTALLIZATION

- GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION, THOUSAND UNITS), 2020-2029

- WASTEWATER TREATMENT

- DESALINATION

- GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION, THOUSAND UNITS), 2020-2029

- POWER GENERATION

- TEXTILES

- CHEMICALS AND PETROCHEMICALS

- PHARMACEUTICALS

- MINING

- FOOD AND BEVERAGES

- GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY REGION (USD BILLION, THOUSAND UNITS), 2020-2029

- NORTH AMERICA

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

- COMPANY PROFILES* (BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCTS OFFERED, RECENT DEVELOPMENTS)

- AQUATECH INTERNATIONAL

- ALFA LAVAL AB

- TOSHIBA INFRASTRUCTURE SYSTEMS AND SOLUTIONS CORPORATION

- H2O GMBH

- AQUARION AG

- VEOLIA WATER TECHNOLOGIES

- ION EXCHANGE LTD.

- SUEZ WATER TECHNOLOGIES & SOLUTIONS

- GEA GROUP AG

- U.S. WATER SERVICES, INC.

- PRAJ INDUSTRIES LTD

- SAFBON WATER TECHNOLOGY

- SALTWORKS TECHNOLOGIES INC

- PETRO SEP CORPORATION

- CONDORCHEM S.P.A *THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 2 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 3 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 4 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 5 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 6 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 7 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 8 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 9 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 10 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 11 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 12 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY REGION (THOUSAND UNITS) 2020-2029

TABLE 13 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 14 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY COUNTRY (THOUSAND UNITS) 2020-2029

TABLE 15 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 16 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 17 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 18 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 19 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 20 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 21 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 22 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 23 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 24 NORTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 25 US ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 26 US ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 27 US ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 28 US ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 29 US ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 30 US ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 31 US ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 32 US ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 33 US ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 34 US ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 35 CANADA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 36 CANADA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 37 CANADA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 38 CANADA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 39 CANADA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 40 CANADA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 41 CANADA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 42 CANADA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 43 CANADA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 44 CANADA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 45 MEXICO ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 46 MEXICO ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 47 MEXICO ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 48 MEXICO ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 49 MEXICO ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 50 MEXICO ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 51 MEXICO ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 52 MEXICO ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 53 MEXICO ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 54 MEXICO ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 55 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 56 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY COUNTRY (THOUSAND UNITS) 2020-2029

TABLE 57 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 58 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 59 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 60 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 61 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 62 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 63 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 64 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 65 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 66 SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 67 BRAZIL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 68 BRAZIL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 69 BRAZIL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 70 BRAZIL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 71 BRAZIL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 72 BRAZIL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 73 BRAZIL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 74 BRAZIL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 75 BRAZIL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 76 BRAZIL ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 77 ARGENTINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 78 ARGENTINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 79 ARGENTINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 80 ARGENTINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 81 ARGENTINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 82 ARGENTINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 83 ARGENTINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 84 ARGENTINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 85 ARGENTINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 86 ARGENTINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 87 COLOMBIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 88 COLOMBIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 89 COLOMBIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 90 COLOMBIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 91 COLOMBIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 92 COLOMBIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 93 COLOMBIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 94 COLOMBIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 95 COLOMBIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 96 COLOMBIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 97 REST OF SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 98 REST OF SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 99 REST OF SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 100 REST OF SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 101 REST OF SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 102 REST OF SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 103 REST OF SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 104 REST OF SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 105 REST OF SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 106 REST OF SOUTH AMERICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 107 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 108 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY COUNTRY (THOUSAND UNITS) 2020-2029

TABLE 109 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 110 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 111 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 112 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 113 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 114 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 115 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 116 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 117 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 118 ASIA-PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 119 INDIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 120 INDIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 121 INDIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 122 INDIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 123 INDIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 124 INDIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 125 INDIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 126 INDIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 127 INDIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 128 INDIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 129 CHINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 130 CHINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 131 CHINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 132 CHINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 133 CHINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 134 CHINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 135 CHINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 136 CHINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 137 CHINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 138 CHINA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 139 JAPAN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 140 JAPAN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 141 JAPAN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 142 JAPAN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 143 JAPAN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 144 JAPAN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 145 JAPAN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 146 JAPAN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 147 JAPAN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 148 JAPAN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 149 SOUTH KOREA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 150 SOUTH KOREA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 151 SOUTH KOREA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 152 SOUTH KOREA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 153 SOUTH KOREA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 154 SOUTH KOREA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 155 SOUTH KOREA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 156 SOUTH KOREA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 157 SOUTH KOREA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 158 SOUTH KOREA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 159 AUSTRALIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 160 AUSTRALIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 161 AUSTRALIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 162 AUSTRALIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 163 AUSTRALIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 164 AUSTRALIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 165 AUSTRALIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 166 AUSTRALIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 167 AUSTRALIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 168 AUSTRALIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 169 SOUTH-EAST ASIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 170 SOUTH-EAST ASIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 171 SOUTH-EAST ASIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 172 SOUTH-EAST ASIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 173 SOUTH-EAST ASIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 174 SOUTH-EAST ASIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 175 SOUTH-EAST ASIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 176 SOUTH-EAST ASIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 177 SOUTH-EAST ASIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 178 SOUTH-EAST ASIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 179 REST OF ASIA PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 180 REST OF ASIA PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 181 REST OF ASIA PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 182 REST OF ASIA PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 183 REST OF ASIA PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 184 REST OF ASIA PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 185 REST OF ASIA PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 186 REST OF ASIA PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 187 REST OF ASIA PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 188 REST OF ASIA PACIFIC ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 189 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 190 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY COUNTRY (THOUSAND UNITS) 2020-2029

TABLE 191 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 192 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 193 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 194 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 195 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 196 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 197 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 198 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 199 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 200 EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 201 GERMANY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 202 GERMANY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 203 GERMANY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 204 GERMANY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 205 GERMANY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 206 GERMANY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 207 GERMANY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 208 GERMANY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 209 GERMANY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 210 GERMANY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 211 UK ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 212 UK ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 213 UK ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 214 UK ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 215 UK ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 216 UK ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 217 UK ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 218 UK ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 219 UK ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 220 UK ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 221 FRANCE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 222 FRANCE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 223 FRANCE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 224 FRANCE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 225 FRANCE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 226 FRANCE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 227 FRANCE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 228 FRANCE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 229 FRANCE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 230 FRANCE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 231 ITALY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 232 ITALY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 233 ITALY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 234 ITALY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 235 ITALY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 236 ITALY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 237 ITALY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 238 ITALY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 239 ITALY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 240 ITALY ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 241 SPAIN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 242 SPAIN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 243 SPAIN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 244 SPAIN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 245 SPAIN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 246 SPAIN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 247 SPAIN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 248 SPAIN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 249 SPAIN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 250 SPAIN ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 251 RUSSIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 252 RUSSIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 253 RUSSIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 254 RUSSIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 255 RUSSIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 256 RUSSIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 257 RUSSIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 258 RUSSIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 259 RUSSIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 260 RUSSIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 261 REST OF EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 262 REST OF EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 263 REST OF EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 264 REST OF EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 265 REST OF EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 266 REST OF EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 267 REST OF EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 268 REST OF EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 269 REST OF EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 270 REST OF EUROPE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 271 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 272 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY COUNTRY (THOUSAND UNITS) 2020-2029

TABLE 273 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 274 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 275 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 276 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 277 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 278 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 279 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 280 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 281 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 282 MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 283 UAE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 284 UAE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 285 UAE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 286 UAE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 287 UAE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 288 UAE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 289 UAE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 290 UAE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 291 UAE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 292 UAE ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 293 SAUDI ARABIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 294 SAUDI ARABIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 295 SAUDI ARABIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 296 SAUDI ARABIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 297 SAUDI ARABIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 298 SAUDI ARABIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 299 SAUDI ARABIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 300 SAUDI ARABIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 301 SAUDI ARABIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 302 SAUDI ARABIA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 303 SOUTH AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 304 SOUTH AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 305 SOUTH AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 306 SOUTH AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 307 SOUTH AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 308 SOUTH AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 309 SOUTH AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 310 SOUTH AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 311 SOUTH AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 312 SOUTH AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

TABLE 313 REST OF MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (USD BILLION) 2020-2029

TABLE 314 REST OF MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY SYSTEM (THOUSAND UNITS) 2020-2029

TABLE 315 REST OF MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (USD BILLION) 2020-2029

TABLE 316 REST OF MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY PROCESS (THOUSAND UNITS) 2020-2029

TABLE 317 REST OF MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (USD BILLION) 2020-2029

TABLE 318 REST OF MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY TECHNOLOGY (THOUSAND UNITS) 2020-2029

TABLE 319 REST OF MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 320 REST OF MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY APPLICATION (THOUSAND UNITS) 2020-2029

TABLE 321 REST OF MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 322 REST OF MIDDLE EAST AND AFRICA ZERO LIQUID DISCHARGE SYSTEMS MARKET BY END USER (THOUSAND UNITS) 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 3 BOTTOM-UP APPROACH

FIGURE 4 RESEARCH FLOW

FIGURE 5 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY SYSTEM, USD BILLION, 2020-2029

FIGURE 6 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY PROCESS, USD BILLION, 2020-2029

FIGURE 7 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY TECHNOLOGY, USD BILLION, 2020-2029

FIGURE 8 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY APPLICATION, USD BILLION, 2020-2029

FIGURE 9 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY END USER, USD BILLION, 2020-2029

FIGURE 19 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY REGION, USD BILLION, 2020-2029

FIGURE 11 PORTER’S FIVE FORCES MODEL

FIGURE 12 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY SYSTEM, USD BILLION, 2021

FIGURE 13 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY PROCESS, USD BILLION, 2021

FIGURE 14 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY TECHNOLOGY, USD BILLION, 2021

FIGURE 15 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY APPLICATION, USD BILLION, 2021

FIGURE 16 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY END USER, USD BILLION, 2021

FIGURE 17 GLOBAL ZERO LIQUID DISCHARGE SYSTEMS BY REGION, USD BILLION, 2021

FIGURE 18 MARKET SHARE ANALYSIS

FIGURE 19 AQUATECH INTERNATIONAL: COMPANY SNAPSHOT

FIGURE 20 F5 ALFA LAVAL AB: COMPANY SNAPSHOT

FIGURE 21 TOSHIBA INFRASTRUCTURE SYSTEMS AND SOLUTIONS CORPORATION: COMPANY SNAPSHOT

FIGURE 22 H2O GMBH: COMPANY SNAPSHOT

FIGURE 23 AQUARION AG: COMPANY SNAPSHOT

FIGURE 24 VEOLIA WATER TECHNOLOGIES: COMPANY SNAPSHOT

FIGURE 25 ION EXCHANGE LTD.: COMPANY SNAPSHOT

FIGURE 26 SUEZ WATER TECHNOLOGIES & SOLUTIONS: COMPANY SNAPSHOT

FIGURE 27 GEA GROUP AG: COMPANY SNAPSHOT

FIGURE 28 U.S. WATER SERVICES, INC.: COMPANY SNAPSHOT

FIGURE 29 PRAJ INDUSTRIES LTD: COMPANY SNAPSHOT

FIGURE 30 SAFBON WATER TECHNOLOGY: COMPANY SNAPSHOT

FIGURE 31 SALTWORKS TECHNOLOGIES INC: COMPANY SNAPSHOT

FIGURE 32 PETRO SEP CORPORATION: COMPANY SNAPSHOT

FIGURE 33 CONDORCHEM S.P.A.: COMPANY SNAPSHOT

FAQ

The global abrasives market is projected to reach USD 78.55 billion by 2029 from USD 50.20 billion in 2020, at a CAGR of 5.11 % from 2022 to 2029.

Increasing demand for metal fabrication on account of growth in the manufacturing sector is anticipated to augment abrasives market growth over the forecast period.

The global abrasives market registered a CAGR of 5.11 % from 2022 to 2029.

The Asia-Pacific region is expected to dominate the abrasives market in the future. The growing construction, automotive, aerospace, and electronics industries are all contributing to the market’s massive demand. China’s expansion is primarily driven by rapid expansion in the residential and commercial building sectors, as well as the country’s expanding economy.

In-Depth Database

Our Report’s database covers almost all topics of all regions over the Globe.

Recognised Publishing Sources

Tie ups with top publishers around the globe.

Customer Support

Complete pre and post sales

support.

Safe & Secure

Complete secure payment

process.