INTERESTED IN THIS RESEARCH?

Contact our analysts for inquiries, samples, and expert insights.

REPORT OUTLOOK

| Market Size | CAGR | Dominating Region |

|---|---|---|

| USD 38.6 billion by 2029 | 4.2% | Asia Pacific |

| By Form | By Alkalinity | By End-User |

|---|---|---|

|

|

|

SCOPE OF THE REPORT

Refractories Market Overview

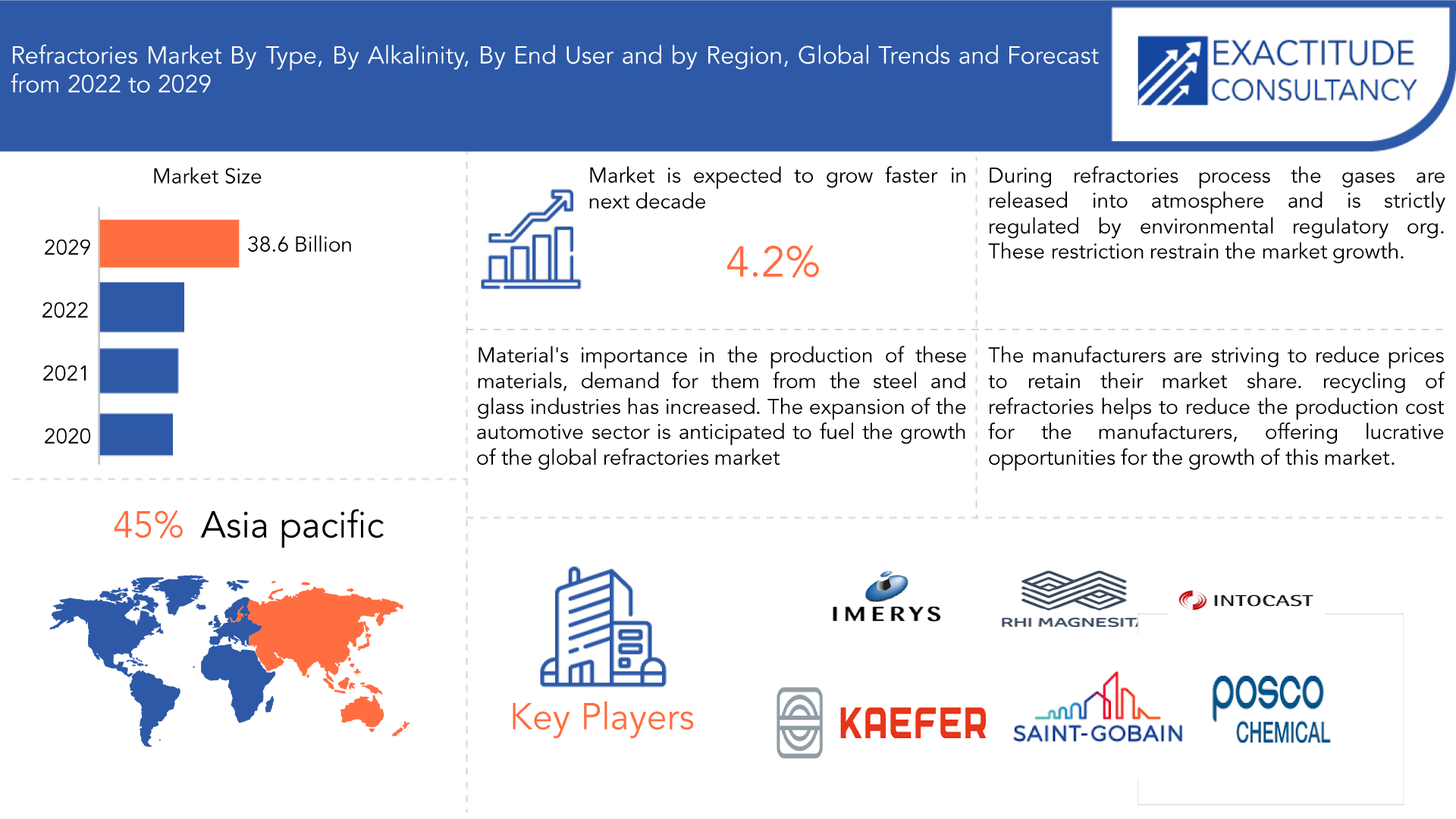

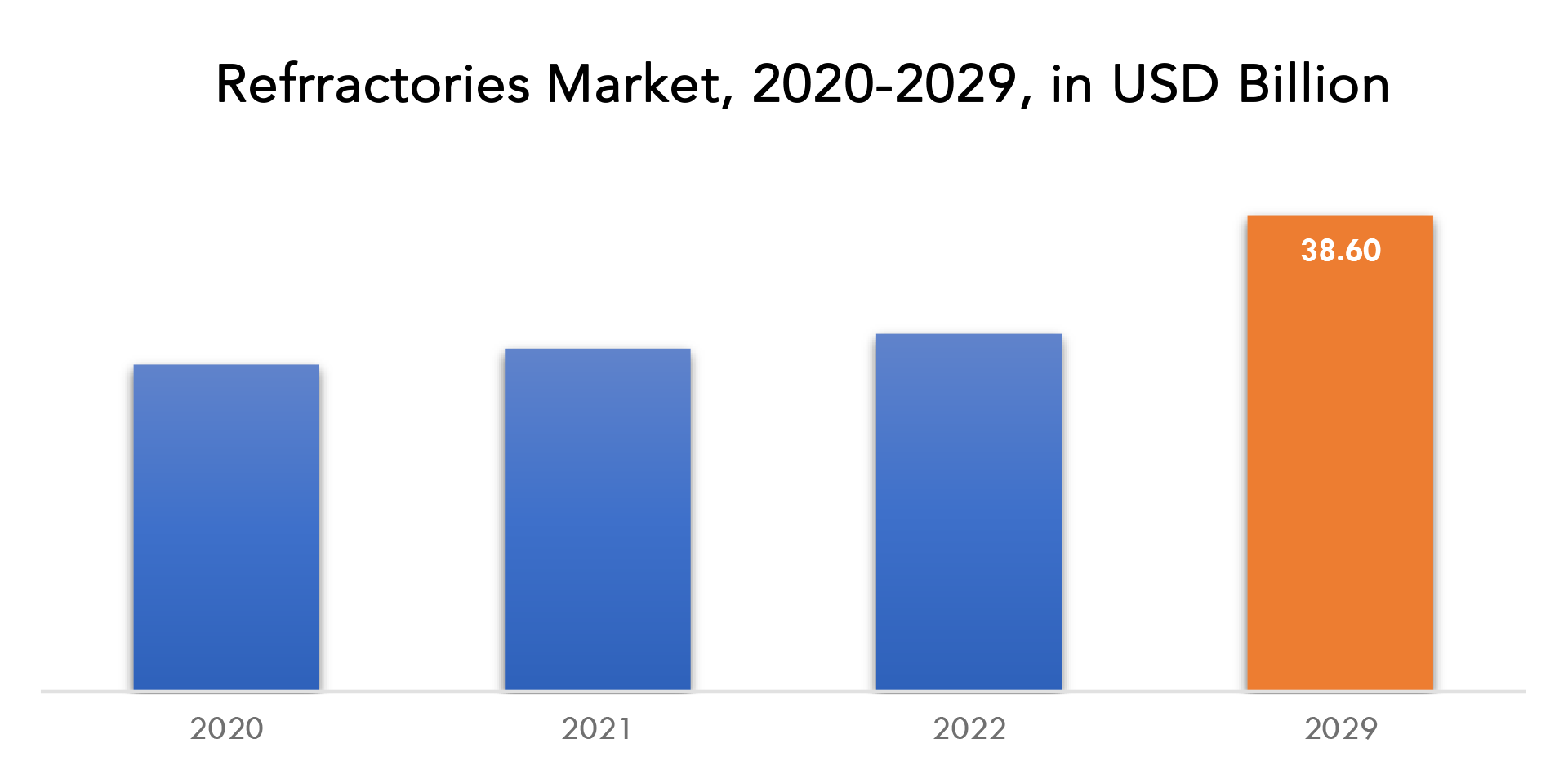

The Refractories market is expected to grow at 4.2% CAGR from 2020 to 2029. It is expected to reach above USD 38.6 billion by 2029 from USD 26.5 billion in 2020.

Refractories are ceramic materials created to endure the extreme heat (over 1,000°F; 538°C) present in contemporary production. They are utilized to line the hot surfaces present in many industrial processes since they are more heat-resistant than metals. Refractories can endure physical wear and corrosion brought on by chemical agents in addition to being resistant to thermal stress and other physical phenomena brought on by heat. They are therefore necessary for the production of petrochemical goods and the refinement of gasoline.

Preformed forms or unformed compositions, which are frequently referred to as specialized or monolithic refractories, are the two main categories into which refractory products typically fall. Then there are refractory ceramic fibers, which insulate at considerably greater temperatures but resemble household insulation. The most conventional form of refractories, which traditionally has made up the majority of refractory manufacturing, are bricks and forms.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2029 |

| Base year | 2021 |

| Estimated year | 2022 |

| Forecasted year | 2022-2029 |

| Historical period | 2018-2020 |

| Unit | Value (USD BILLION) (Kilotons) |

| Segmentation | By Form, By Alkalinity, By End-User, By Region |

| By Form |

|

| By Alkalinity |

|

| By End-User |

|

| By Region |

|

Refractories exist in a variety of forms and dimensions. They can be made in interlocking forms and wedges, pressed or molded for usage in floors and walls, or bent to fit the inside of boilers and ladles. While some refractory components are large and may weigh several tones, others, in the form of precast or fusion-cast blocks, are huge and have intricate geometrics.

Steel, iron, and glass have gained traction as a result of the recent revival of the automobile industry, especially with the rise of electric vehicles. The body structure of a vehicle is composed of 60% steel-based products, according to a report released jointly by the Global Steel Association and the International Organization of Motor Vehicle Manufacturers. Comparatively, glass makes up more than 6% of the car’s total weight. Due to the material’s importance in the production of these materials, demand for them from the steel and glass industries has increased. Thus, the expansion of the automotive sector is anticipated to fuel the growth of the global refractories market.

As one of the world’s economies with the greatest rate of expansion, China requires ongoing road and rail infrastructure construction. The development of the Chinese car sector has also been aided by this. The construction of homes and businesses has expanded as a result of the accelerated infrastructure development in these developing nations, which is anticipated to raise demand for refractories in the cement and iron & steel sectors. The need for refractories will be driven by rising construction activity in emerging nations, which is also anticipated to stimulate the glass industry.

Refractory grogs are the discarded refractory materials that are further recycled to create secondary raw resources. Refractories come in two different quality ranges: high quality and low quality. The number of recycled refractories that can be used in other processes depends on the quality of the original refractory; only 0–30% of the recycled refractories made from low-quality refractories may be utilized in other processes. Due to rising freight and raw material costs as well as environmental concerns forcing businesses to search for more environmentally friendly alternatives for refractory applications, the necessity for recycling refractory goods has grown.

Mining, baking, and curing refractory materials are only a few of the carbon-intensive processes used in the creation of these goods. Significant volumes of CO2 and other pollutants, like carbon monoxide and volatile organic compounds, are generated during the production process. The release of these gases into the atmosphere is strictly regulated by environmental regulatory organizations since they are known to act as greenhouse gases. Moreover, a sizable amount of energy is required throughout the production process, which further increases the carbon intensity. Refractory material producers are being pressured to reduce their carbon intensity, which reduces their profit margins, as environmental, health, and safety concerns are becoming more and more prominent. These restrictions restrict the market’s potential for expansion since of the market’s current fierce rivalry.

The COVID-19 epidemic has had a significant negative impact on the global market for refractories. Refractories were less in demand during that time as a result of government measures like lockdowns, factory closures, and social isolation. In many areas of the regional market, as well as in international exports and imports, the COVID-19 outbreak has imposed restrictions such as lockdown and travel prohibitions inside the nation and within states, which has caused delays in logistics and deliveries.

Refractories Market Segment Analysis

The refractories market is segmented based on form, alkalinity, end-use and region, global trends and forecast.

Based on form, the market is divided into shaped and unshaped categories based on form. Due to the substantial demand for these items from the metal and non-metal sectors, the shaped category holds the largest market share. Bricks are needed to create the insulation layer inside ovens and kilns, and they must be replaced on a regular basis to maintain the customer-specified insulation ratings. The bigger market share of the shaped sector is mostly due to this aspect. However, due to increased need to produce linings inside reactors, where positioning of shaped refractories is limited by space constraints, the unshaped category is anticipated to acquire market share throughout the projection period.

Based on alkalinity, the market is divided into acidic & neutral and basic categories based on alkalinity. Dolomite, magnesia-chrome, and magnesia site are resistant to the chemical attack of bases used in the production of products like ferrous metals and cement. The demand is anticipated to increase greatly throughout the forecast period since the demand for these materials is growing rapidly. On the other hand, since to the presence of acids during the manufacturing process, silica, zirconia, and aluminosilicate resist corrosion. The iron and steel industry, which uses acids to process minerals to produce pure metallic goods, is the biggest consumer of acidic refractory products. In these procedures, neutral refractory materials like carbon and alumina are preferred.

Based on end use, the market is divided into iron & steel, non-ferrous metals, glass, cement, and other end-use industries. Due to the fact that practically all furnaces, reactors, and vessels used in the production of steel employ iron and steel, this industry dominates the global market. Also, the iron and steel sector consume a lot of energy since the refractory lining is periodically replaced, every 30 minutes to two days, in the various steps of the steel producing process.

Refractories Market Players

The Refractories market key players IMERYS, POSCO Chemica, RHI MAGNESTHIA, Kaefer, INTOCAST Group, Beijing Lier high Temperature Materials Co. Ltd, Magnzit Group, Saint-Gobain, Refratechnik, Plibrico Company.

News:

- 24-10-2022: IMERYS announced the start of the EMILI project in the presence of government officials, elected representatives and local authorities.

- 28-02-2023: From energy usage to emissions and natural resources, the construction industry has a huge impact on the environment. Today, this impact translates to revisions in building regulations, leveraging of technological advances and new materials, and greater adoption of sustainable construction methods. This sustainability is what we strive for.

Who Should Buy? Or Key stakeholders

- Refractories Suppliers

- Manufacturing

- Construction

- Auto sector

- Investors

- Others

Refractories Market Regional Analysis

The Refractories market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).

- North America: includes the US, Canada, Mexico

- Asia Pacific: includes China, Japan, South Korea, India, Australia, ASEAN and Rest of APAC

- Europe: includes UK, Germany, France, Italy, Spain, Russia, and Rest of Europe

- South America: includes Brazil, Argentina and Rest of South America

- Middle East & Africa: includes Turkey, UAE, Saudi Arabia, South Africa, and Rest of MEA

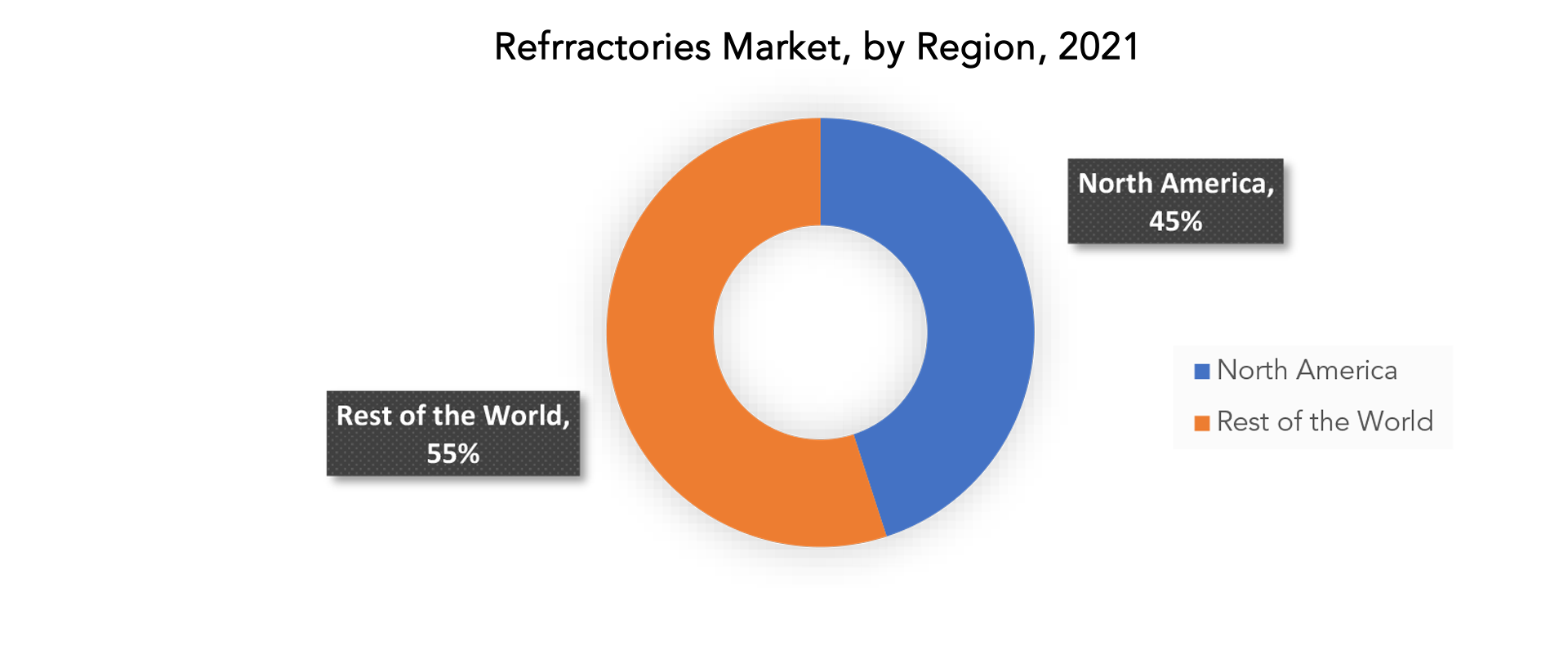

Asia Pacific holds 45% of the market share overall. Due to the existence of numerous end-use industries in the region, Asia Pacific is anticipated to hold the highest share of the global market. The Global Steel Association estimates that China alone produces about 50% of the world’s steel, with Asia Pacific accounting for more than 70% of that total. The dominance of the Asia Pacific region in the global economy is largely due to this aspect. The region’s advantage is further strengthened by the region’s significant non-ferrous metal and cement sectors.

Due to rising demand from the region’s end-use industries, particularly the glass and iron & steel sectors, the market in North America will expand. The market in Europe will develop relatively slowly, but is anticipated to be revived by the region’s car manufacturers’ rising demand for steel and glass. Since 15% of the world’s steel production is produced in Europe, the expansion of this market in that continent will be mirrored by the expansion of the steel industry there.

Key Market Segments

Refractories Market By Form, 2020-2029, (USD Billion) (Kilotons)

- Shaped Refrctories

- Unshaped Refractories

Refractories Market By Alkalinity, 2020-2029, (USD Billion) (Kilotons)

- Acidic & Neutral

- Basic

Refractories Market By End-User, 2020-2029, (USD Billion) (Kilotons)

- Iron & Steel

- Power Generation

- Non-Ferrous Metals

- Cement

- Glass

Refractories Market By Region, 2020-2029, (USD Billion) (Kilotons)

- North America

- Asia Pacific

- Europe

- South America

- Middle East And Africa

Important Countries In All Regions Are Covered.

Exactitude Consultancy Services Key Objectives

- Increasing sales and market share

- Developing new technology

- Improving profitability

- Entering new markets

- Enhancing brand reputation

Key Question Answered

- What is the expected growth rate of the refractories market over the next 7 years?

- Who are the major players in the refractories market and what is their market share?

- What are the end-user industries driving demand for market and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-Pacific, Middle East, And Africa?

- How is the economic environment affecting the refractories market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the refractories market?

- What is the current and forecasted size and growth rate of the global refractories market?

- What are the key drivers of growth in the refractories market?

- Who are the major players in the market and what is their market share?

- What are the distribution channels and supply chain dynamics in the refractories market?

- What are the technological advancements and innovations in the refractories market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the refractories market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the refractories market?

- What are the service offerings and specifications of leading players in the market?

- What is the pricing trend of refractories in the market and what is the impact of raw material prices on the price trend?

Table of Content

- INTRODUCTION

- MARKET DEFINITION

- MARKET SEGMENTATION

- RESEARCH TIMELINES

- ASSUMPTIONS AND LIMITATIONS

- RESEARCH METHODOLOGY

- DATA MINING

- SECONDARY RESEARCH

- PRIMARY RESEARCH

- SUBJECT-MATTER EXPERTS’ ADVICE

- QUALITY CHECKS

- FINAL REVIEW

- DATA TRIANGULATION

- BOTTOM-UP APPROACH

- TOP-DOWN APPROACH

- RESEARCH FLOW

- DATA SOURCES

- DATA MINING

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- GLOBAL REFRACTORIES OUTLOOK

- MARKET DRIVERS

- MARKET RESTRAINTS

- MARKET OPPORTUNITIES

- IMPACT OF COVID-19 ON REFRACTORIES MARKET

- PORTER’S FIVE FORCES MODEL

- THREAT FROM NEW ENTRANTS

- THREAT FROM SUBSTITUTES

- BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER OF CUSTOMERS

- DEGREE OF COMPETITION

- INDUSTRY VALUE CHAIN ANALYSIS

- GLOBAL REFRACTORIES OUTLOOK

- GLOBAL REFRACTORIES MARKET BY FORM (USD BILLION) (KILOTONS) 2020-2029

- SHAPED REFRACTORIES

- UNSHAPED REFRACTORIES

- GLOBAL REFRACTORIES MARKET BY ALKALINITY (USD BILLION) (KILOTONS) 2020-2029

- ACIDIC & NEUTRAL

- BASIC

- GLOBAL REFRACTORIES MARKET BY END USE (USD BILLION) (KILOTONS) 2020-2029

- IRON & STEEL

- POWER GENERATION

- NON-FERROUS METALS

- CEMENT

- GLASS

- GLOBAL REFRACTORIES MARKET BY REGION (USD BILLION) (KILOTONS) 2020-2029

- NORTH AMERICA

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

- COMPANY PROFILES* (BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCTS OFFERED, RECENT DEVELOPMENTS)

- IMERYS

- POSCO CHEMICA

- RHI MAGNESTHIA

- KAEFER

- INTOCAST GROUP

- BEIJING LIER HIGH TEMPERATURE ALKALINITY

- MAGNZIT GROUP

- AINT-GOBIN

- REFRATECHNIK

- PLIBRICO COMPANY *THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 2 GLOBAL REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 3 GLOBAL REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 4 GLOBAL REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 5 GLOBAL REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 6 GLOBAL REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 7 GLOBAL REFRACTORIES MARKET BY REGION (USD BILLION) 2020-2029

TABLE 8 GLOBAL REFRACTORIES MARKET BY REGION (KILOTONS) 2020-2029

TABLE 9 NORTH AMERICA REFRACTORIES MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 10 NORTH AMERICA REFRACTORIES MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 11 US REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 12 US REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 13 US REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 14 US REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 15 US REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 16 US REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 17 CANADA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 18 CANADA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 19 CANADA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 20 CANADA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 21 CANADA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 22 CANADA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 23 MEXICO REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 24 MEXICO REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 25 MEXICO REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 26 MEXICO REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 27 MEXICO REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 28 MEXICO REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 29 SOUTH AMERICA REFRACTORIES MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 30 SOUTH AMERICA REFRACTORIES MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 31 BRAZIL REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 32 BRAZIL REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 33 BRAZIL REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 34 BRAZIL REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 35 BRAZIL REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 36 BRAZIL REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 37 ARGENTINA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 38 ARGENTINA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 39 ARGENTINA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 40 ARGENTINA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 41 ARGENTINA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 42 ARGENTINA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 43 COLOMBIA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 44 COLOMBIA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 45 COLOMBIA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 46 COLOMBIA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 47 COLOMBIA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 48 COLOMBIA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 49 REST OF SOUTH AMERICA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 50 REST OF SOUTH AMERICA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 51 REST OF SOUTH AMERICA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 52 REST OF SOUTH AMERICA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 53 REST OF SOUTH AMERICA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 54 REST OF SOUTH AMERICA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 55 ASIA-PACIFIC REFRACTORIES MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 56 ASIA-PACIFIC REFRACTORIES MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 57 INDIA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 58 INDIA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 59 INDIA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 60 INDIA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 61 INDIA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 62 INDIA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 63 CHINA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 64 CHINA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 65 CHINA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 66 CHINA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 67 CHINA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 68 CHINA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 69 JAPAN REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 70 JAPAN REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 71 JAPAN REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 72 JAPAN REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 73 JAPAN REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 74 JAPAN REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 75 SOUTH KOREA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 76 SOUTH KOREA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 77 SOUTH KOREA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 78 SOUTH KOREA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 79 SOUTH KOREA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 80 SOUTH KOREA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 81 AUSTRALIA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 82 AUSTRALIA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 83 AUSTRALIA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 84 AUSTRALIA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 85 AUSTRALIA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 86 AUSTRALIA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 87 SOUTH-EAST ASIA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 88 SOUTH-EAST ASIA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 89 SOUTH-EAST ASIA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 90 SOUTH-EAST ASIA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 91 SOUTH-EAST ASIA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 92 SOUTH-EAST ASIA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 93 REST OF ASIA PACIFIC REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 94 REST OF ASIA PACIFIC REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 95 REST OF ASIA PACIFIC REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 96 REST OF ASIA PACIFIC REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 97 REST OF ASIA PACIFIC REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 98 REST OF ASIA PACIFIC REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 99 EUROPE REFRACTORIES MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 100 EUROPE REFRACTORIES MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 101 GERMANY REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 102 GERMANY REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 103 GERMANY REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 104 GERMANY REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 105 GERMANY REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 106 GERMANY REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 107 UK REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 108 UK REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 109 UK REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 110 UK REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 111 UK REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 112 UK REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 113 FRANCE REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 114 FRANCE REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 115 FRANCE REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 116 FRANCE REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 117 FRANCE REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 118 FRANCE REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 119 ITALY REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 120 ITALY REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 121 ITALY REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 122 ITALY REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 123 ITALY REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 124 ITALY REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 125 SPAIN REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 126 SPAIN REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 127 SPAIN REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 128 SPAIN REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 129 SPAIN REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 130 SPAIN REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 131 RUSSIA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 132 RUSSIA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 133 RUSSIA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 134 RUSSIA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 135 RUSSIA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 136 RUSSIA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 137 REST OF EUROPE REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 138 REST OF EUROPE REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 139 REST OF EUROPE REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 140 REST OF EUROPE REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 141 REST OF EUROPE REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 142 REST OF EUROPE REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 143 MIDDLE EAST AND AFRICA REFRACTORIES MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 144 MIDDLE EAST AND AFRICA REFRACTORIES MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 145 UAE REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 146 UAE REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 147 UAE REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 148 UAE REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 149 UAE REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 150 UAE REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 151 SAUDI ARABIA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 152 SAUDI ARABIA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 153 SAUDI ARABIA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 154 SAUDI ARABIA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 155 SAUDI ARABIA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 156 SAUDI ARABIA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 157 SOUTH AFRICA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 158 SOUTH AFRICA REFRACTORIES MARKET BY FORM (KILOTONS) 2020-2029

TABLE 159 SOUTH AFRICA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 160 SOUTH AFRICA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 161 SOUTH AFRICA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 162 SOUTH AFRICA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 163 REST OF MIDDLE EAST AND AFRICA REFRACTORIES MARKET BY FORM (USD BILLION) 2020-2029

TABLE 164 REST OF MIDDLE EAST AND AFRICA REFRACTORIES MARKET BY FORM (KILOTONS) 2020- 2029

TABLE 165 REST OF MIDDLE EAST AND AFRICA REFRACTORIES MARKET BY ALKALINITY (USD BILLION) 2020-2029

TABLE 166 REST OF MIDDLE EAST AND AFRICA REFRACTORIES MARKET BY ALKALINITY (KILOTONS) 2020-2029

TABLE 167 REST OF MIDDLE EAST AND AFRICA REFRACTORIES MARKET BY END USER (USD BILLION) 2020-2029

TABLE 168 REST OF MIDDLE EAST AND AFRICA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

TABLE 169 REST OF MIDDLE EAST AND AFRICA REFRACTORIES MARKET BY END USER (KILOTONS) 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL REFRACTORIES BY FORM, USD BILLION, 2020-2029

FIGURE 9 GLOBAL REFRACTORIES BY END USER, USD BILLION, 2020-2029

FIGURE 10 GLOBAL REFRACTORIES BY ALKALINITY, USD BILLION, 2020-2029

FIGURE 11 GLOBAL REFRACTORIES BY REGION, USD BILLION, 2020-2029

FIGURE 12 GLOBAL REFRACTORIES BY FORM, USD BILLION, 2021

FIGURE 13 GLOBAL REFRACTORIESBY END USER, USD BILLION, 2021

FIGURE 14 GLOBAL REFRACTORIESBY ALKALINITY, USD BILLION, 2021

FIGURE 15 GLOBAL REFRACTORIESBY REGION, USD BILLION, 2021

FIGURE 16 PORTER’S FIVE FORCES MODEL

FIGURE 17 MARKET SHARE ANALYSIS

FIGURE 18 IMERYS: COMPANY SNAPSHOT

FIGURE 19 POSCO CHEMICA: COMPANY SNAPSHOT

FIGURE 20 RHI MAGNESTHIA: COMPANY SNAPSHOT

FIGURE 21 KAEFER: COMPANY SNAPSHOT

FIGURE 22 INTOCAST GROUP: COMPANY SNAPSHOT

FIGURE 23 BEIJING LIER HIGH TEMPERATURE ALKALINITY CO.LTD: COMPANY SNAPSHOT

FIGURE 24 MAGNZIT: COMPANY SNAPSHOT

FIGURE 25 SAINT-GOBIN: COMPANY SNAPSHOT

FIGURE 26 REFRATECHNIK: COMPANY SNAPSHOT

FAQ

The refractories market is expected to grow at 4.2% CAGR from 2020 to 2029. It is expected to reach above USD 38.6 billion by 2029 from USD 26.5 billion in 2020.

Asia Pacific held more than 45 % of the Refractories market revenue share in 2021 and will witness expansion in the forecast period.

Steel, iron, and glass have gained traction as a result of the recent revival of the automobile industry, especially with the rise of electric vehicles. The body structure of a vehicle is composed of 60% steel-based products, according to a report released jointly by the Global Steel Association and the International Organization of Motor Vehicle Manufacturers. Comparatively, glass makes up more than 6% of the car’s total weight. Due to the material’s importance in the production of these materials, demand for them from the steel and glass industries has increased. Thus, the expansion of the automotive sector is anticipated to fuel the growth of the global refractories market.

Based on Form, the market is divided into shaped and unshaped categories based on form. Due to the substantial demand for these items from the metal and non-metal sectors, the shaped category holds the largest market share. Bricks are needed to create the insulation layer inside ovens and kilns, and they must be replaced on a regular basis to maintain the customer-specified insulation ratings. The bigger market share of the shaped sector is mostly due to this aspect. However, due to increased need to produce linings inside reactors, where positioning of shaped refractories is limited by space constraints, the unshaped category is anticipated to acquire market share throughout the projection period.

Asia Pacific holds 45% of the market share overall. Due to the existence of numerous end-use industries in the region, Asia Pacific is anticipated to hold the highest share of the global market. The Global Steel Association estimates that China alone produces about 50% of the world’s steel, with Asia Pacific accounting for more than 70% of that total. The dominance of the Asia Pacific region in the global economy is largely due to this aspect. The region’s advantage is further strengthened by the region’s significant non-ferrous metal and cement sectors.

In-Depth Database

Our Report’s database covers almost all topics of all regions over the Globe.

Recognised Publishing Sources

Tie ups with top publishers around the globe.

Customer Support

Complete pre and post sales

support.

Safe & Secure

Complete secure payment

process.