INTERESTED IN THIS RESEARCH?

Contact our analysts for inquiries, samples, and expert insights.

Report Outlook

| Market Size | CAGR | Dominating Region |

|---|---|---|

| USD 12.99 Billion by 2030 | 5.30% | North America |

| By Process | By Light Source | By Application |

|---|---|---|

|

|

|

SCOPE OF THE REPORT

Photolithography Market Overview

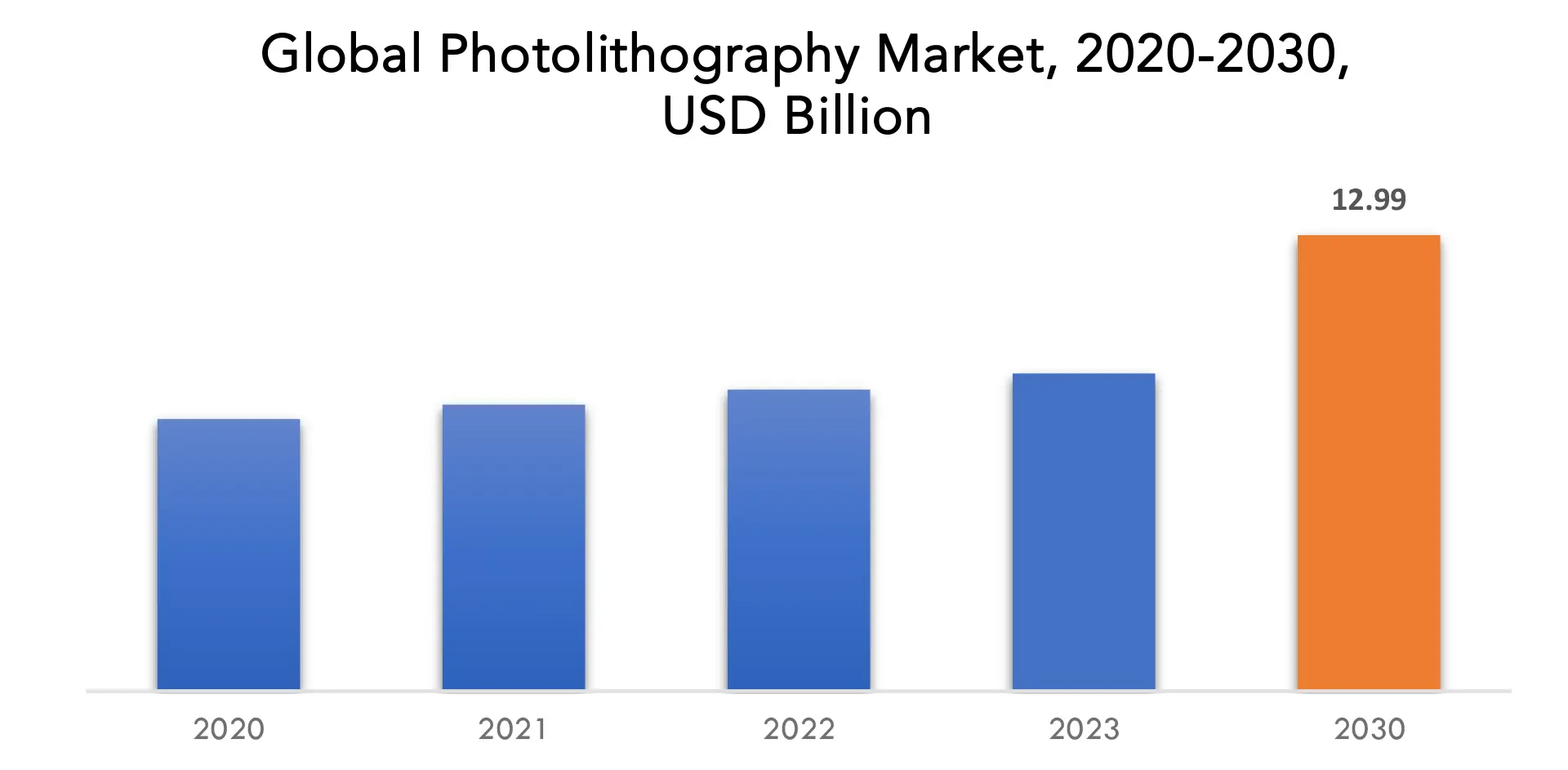

The global photolithography market is anticipated to grow from USD 9.05 Billion in 2023 to USD 12.99 Billion by 2030, at a CAGR of 5.30 % during the forecast period.

A microfabrication technique called photolithography uses light to make patterns on a substrate. Chips, sometimes referred to as integrated circuits (ICs), are typically produced using this technique. Integrated circuits (ICs) and other microelectronic devices are made using the fundamental semiconductor manufacturing technique of photolithography. Transistors, interconnects, and other crucial parts of contemporary electronic devices may be formed by following a sequence of exact processes to produce complicated patterns on a silicon wafer.

A clean silicon wafer covered in a light-sensitive substance called photoresist serves as the starting point of the process. UV light is shined through a photomask that is put over the wafer and includes the required circuit layout. Transparent areas of the mask allow the UV light to flow through, exposing the underlying photoresist. Depending on the kind of photoresist utilised, chemical reactions take place in the exposed regions, increasing or decreasing the soluble amount of the resist. Precision and repeatability in photolithography are essential for developing semiconductor technology and making it possible for current microchips’ ever-shrinking features and enhanced functionality.

Advanced photolithography methods are now more necessary than ever because of the enduring desire for smaller, more powerful, and energy-efficient electronic products. A key factor influencing market expansion is the need for more advanced photolithographic equipment capable of creating complicated and miniaturized patterns due to the shrinking feature sizes on semiconductor devices. The market is expanding due to the photolithography industry’s ongoing technological improvements. Manufacturing of semiconductors may now be done with finer details and more accuracy due to developments like extreme ultraviolet (EUV) lithography, which meets the needs of cutting-edge gadgets.

The need for photolithography has also risen as a result of the spread of upcoming technologies like 5G, AI, and the Internet of Things (IoT). These technologies rely on semiconductor components, whose manufacturing calls for more complex photolithography techniques. Additionally, the industry is expanding and its clientele is becoming more diverse thanks to the growing use of photolithography methods in non-semiconductor applications including MEMS (Micro-Electro-Mechanical Systems), LED production, and sophisticated packaging.

A newer photolithography process called EUV lithography makes it possible to produce transistors that are both smaller and more intricate. For the creation of cutting-edge semiconductor technologies like AI, ML, and 5G, EUV lithography is crucial.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2030 |

| Base year | 2022 |

| Estimated year | 2023 |

| Forecasted year | 2023-2030 |

| Historical period | 2019-2021 |

| Unit | Value (USD Billion) |

| Segmentation | By Service, Light Source, Application and Region |

| By Process |

|

| By Light Source |

|

| By Application |

|

|

By Region

|

|

Photolithography Market Segmentation Analysis

The global Photolithography market is divided into three segments, process, light source, application and region. By process the market is divided into product engineering, process engineering, support, maintenance, and operations. By light source the market is classified into small and medium-sized enterprises, large enterprises. By application the market is classified into automotive & transportation, industrial manufacturing, healthcare & life sciences, it & telecom, aerospace & defense, banking, financial services, and insurance, energy & utilities, others.

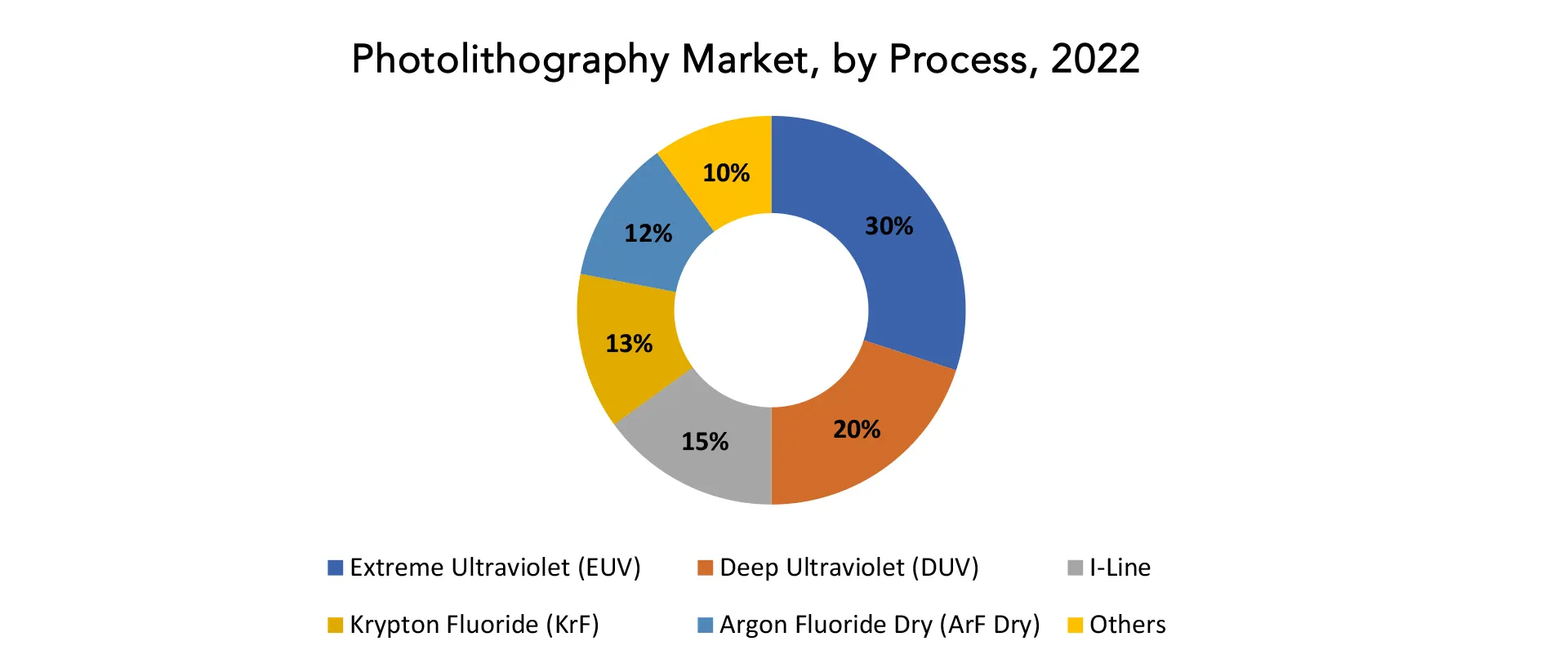

Based on process product engineering segment dominating in the Photolithography market. Extreme ultraviolet (EUV) lithography has become a dominating technique in the photolithography industry, due to its distinct benefits and capabilities in semiconductor production. Since it uses light with extremely short wavelengths (13.5 nanometers or less), EUV lithography offers a major improvement over conventional optical lithography methods. This allows for the manufacture of smaller and more complex semiconductor components.

The capacity of EUV to produce finer feature sizes is one of the main factors contributing to its supremacy. EUV lithography offers the accuracy required to make sub-10nm features, which is crucial for cutting-edge CPUs and memory circuits as semiconductor manufacturers attempt to fit more transistors onto a single chip. Electronic gadgets’ processing speed and memory capacity grow as a result of the finer feature size. Additionally, EUV lithography offers increased scalability and cost-effectiveness. Traditional lithography methods needed several intricate masking and layering procedures in order to generate the necessary designs, which raised production costs and lengthened the manufacturing process. With the use of EUV lithography, many of these difficult stages are not necessary, which lowers manufacturing costs and increases total productivity.

The semiconductor industry’s constant push to boost processing power while lowering the physical size of devices is precisely in line with EUV lithography’s capacity to make smaller, denser patterns.

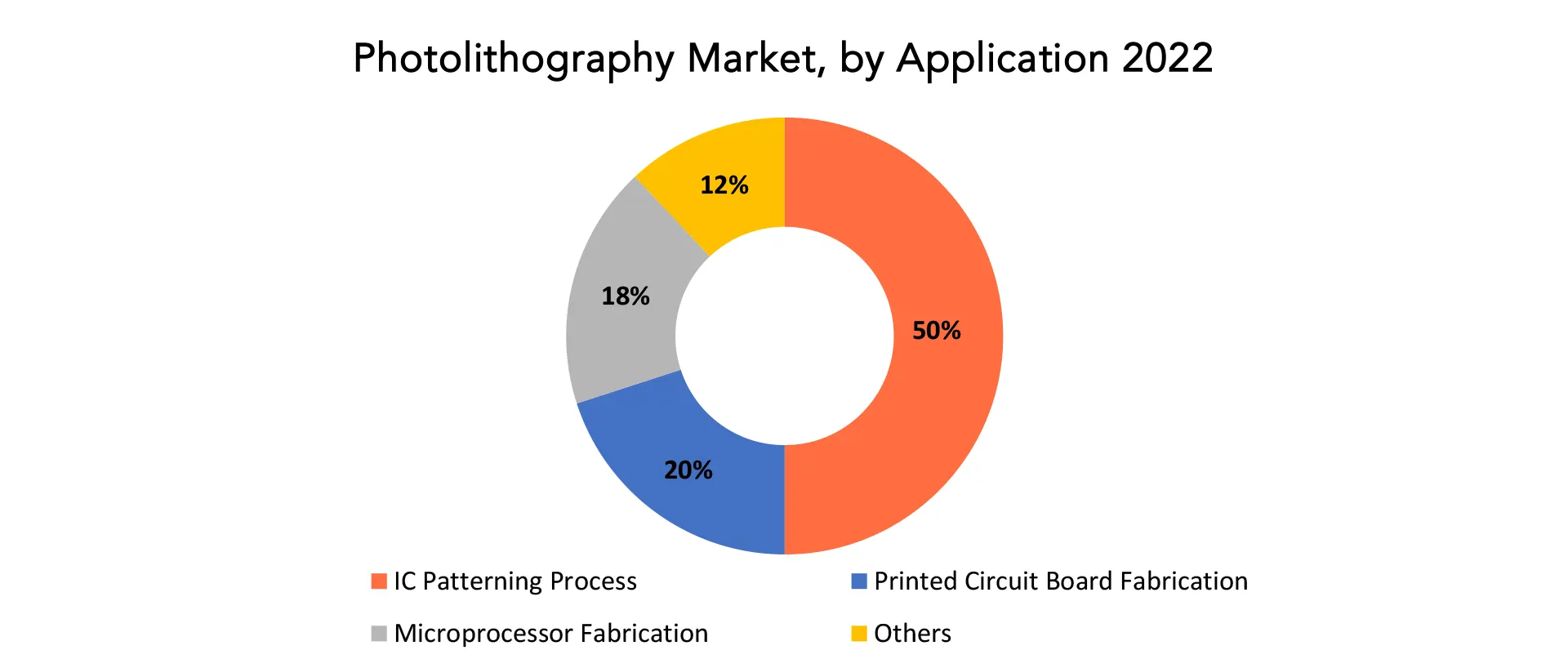

Based on application IC patterning process segment dominating in the photolithography market. Transistors and other electronic components are made using semiconductor wafers that have patterns etched into them during the IC patterning process. A crucial phase in the IC patterning process is photolithography.

The crucial part that semiconductor fabrication plays in IC patterning is one of the main factors contributing to its supremacy. Integrated circuits are the brains and heart of modern electronic devices, such as smartphones, laptops, automotive systems, and Internet of Things (IoT) gadgets. New photolithography techniques that can create patterns that are more intricate and compact have been developed in response to the ongoing need for chips that are smaller, faster, and more energy-efficient. IC patterning, which has developed into the cornerstone of the semiconductor industry, makes it possible to fabricate cutting-edge microprocessors, memory chips, and other essential components.

Additionally, emerging technologies like artificial intelligence, 5G communications, and driverless vehicles also heavily rely on IC patterning. It is not just used in conventional computers and consumer electronics. These applications necessitate specialised semiconductor devices with sub-10nm feature sizes and intricate, multi-layered designs, among other requirements. Advanced photolithography and other IC patterning methods have risen to meet these difficulties, further solidifying their market dominance.

With more transistors and other components on each chip, ICs are growing more complicated. This is increasing the need for photolithography tools that can be used to print increasingly intricate designs with smaller details on semiconductor wafers. Advanced integrated circuits (ICs), including 5G and AI processors, are in high demand. This is driving the demand for photolithography equipment that can be used to produce these advanced ICs.

Photolithography Market Dynamics

Driver

Growing demand for advanced semiconductor technologies driving photolithography market.

The photolithography industry is expanding rapidly, owing mostly to an increasing need for improved semiconductor technologies. This increase of need can be attributable to a number of significant variables. To begin, the persistent desire of smaller and more powerful electronic devices, including smartphones, tablets, IoT devices, and high-performance computer systems, is driving semiconductor makers to create chips with ever-lower feature sizes and greater transistor densities. As a key semiconductor production method, photolithography plays a critical role in attaining these goals through facilitating the exact patterning of nanoscale structures on semiconductor wafers.

In addition, the introduction of cutting-edge semiconductor nodes such as 7nm, 5nm, and even lower nodes demands the use of sophisticated photolithography methods like as extreme ultraviolet (EUV) lithography. With its capacity to create smaller features while reducing process complexity, EUV lithography has become more important in reaching the requisite levels of performance, power efficiency, and functionality in current semiconductor devices.

Furthermore, the increasing need for semiconductor components goes beyond consumer electronics and into essential industries such as automotive, healthcare, telecommunications, and data centres. Autonomous cars, 5G networks, AI-driven healthcare solutions, and cloud computing all rely on advanced semiconductor technology. This broadening of semiconductor applications increases the demand of innovative photolithography equipment and procedures.

Restraint

High operational and maintenance costs of photolithography devices can be a major challenge for the photolithography market during the forecast period.

The intricacy of photolithography equipment, especially at advanced nodes like those below 10nm, needs sophisticated and costly components. Precision engineering and high-quality materials are required for the development and production of cutting-edge photomasks, lenses, optical systems, and stage mechanisms, which raises initial equipment prices. These complex components are necessary for current semiconductor devices to have nanoscale feature sizes.

In addition, keeping photolithography equipment running at top performance levels necessitates continuing investment. Fine-tuned optical system alignment, regular calibration, and tight cleaning standards necessitate expert personnel and specialised instruments. Regular maintenance processes, such as cleaning and replacing components, can be time-consuming and expensive, resulting in downtime in semiconductor production plants.

Also, the shift to sophisticated lithography methods like as extreme ultraviolet (EUV) lithography presents additional obstacles. While EUV lithography equipment has advantages in terms of accuracy and decreased process complexity, it is notorious for its high installation and maintenance costs. The development of EUV sources, optics, and masks necessitates the use of cutting-edge technology and materials, which contributes to increased operating and maintenance costs.

Opportunities

Adoption of extreme ultraviolet (EUV) lithography creates new avenues for photolithography market.

EUV lithography is a next-generation photolithography method that allows for the production of smaller, more sophisticated transistors. EUV lithography is required for the manufacture of modern semiconductor technologies such as AI, machine learning, and 5G. Light having a wavelength of 13.5 nanometers is utilised in EUV lithography, and this is substantially shorter than the wavelength of light utilised by typical photolithography methods. Due to the shorter wavelength, EUV lithography is able to make smaller and more intricate patterns on semiconductor wafers.

EUV lithography enables the development of more sophisticated semiconductor technologies, fueling consumer interest in photolithography equipment. In addition, since EUV lithography is a complicated technique, photolithography equipment providers that provide EUV lithography solutions are seeing new prospects. Also, as EUV lithography is a critical technique for the development of next-generation semiconductors, photolithography equipment providers now have new chances to engage with semiconductor businesses on the creation of innovative EUV lithography technologies and solutions.

EUV lithography significantly streamlines the semiconductor production process by eliminating the requirement for sophisticated multiple patterning techniques that were previously used to overcome optical lithography restrictions. EUV lithography simplifies the manufacturing process by combining many mask layers into a single exposure phase, resulting in higher yields, lower production costs, and quicker time-to-market for semiconductor devices.

Photolithography Market Trends

- Extreme ultraviolet (EUV) lithography gained popularity. Semiconductor manufacturers have increasingly utilised EUV technology for advanced node semiconductor production, enabling for smaller and more efficient devices.

- High-performance electronic devices, photolithography techniques were being modified for advanced packaging applications such as fan-out wafer-level packaging (FOWLP) and through-silicon via (TSV) to meet the need for small.

- Artificial intelligence (AI) and machine learning were being incorporated into photolithography operations to improve yield and efficiency through optimisation, predictive maintenance, and defect identification.

- EUV lithography is a next-generation photolithography method that allows for the production of smaller, more sophisticated transistors. EUV lithography is required for the manufacture of modern semiconductor technologies such as AI, machine learning, and 5G.

- Cloud-based photolithography technologies are rapidly being used by semiconductor businesses. Cloud-based systems have several advantages, including scalability, cost effectiveness, and ease of use.

- Nanoimprint lithography, a low-cost, high-resolution technology, was being evaluated for use in niche applications such as photonics, microfluidics, and nano-electromechanical systems (NEMS).

- In response to environmental concerns, sustainable lithography technologies that cut chemical usage and energy consumption were gaining traction.

- Artificial intelligence (AI) and machine learning were being incorporated into photolithography operations to improve yield and efficiency through optimisation, predictive maintenance, and defect identification.

Competitive Landscape

The competitive landscape of the photolithography market was dynamic, with several prominent companies competing to provide innovative and advanced Photolithography solutions.

- ASML Holdings, N.V

- Nikon Corporation

- Canon, Inc.

- JEOL Ltd

- NuFlare Technology

- Ultratech, Inc.

- Rudolph Technologies, Inc.

- SUSS Mictotec, A.G

- Nil Technology

- EV Group

- Carl Zeiss AG

- Samsung Electronics

- Tokyo Electron Limited

- Applied Materials

- Veeco Instruments Inc.

- Vistec Electron Beam GMBH

- Shanghai Microelectronics equipment group

- Taiwan Semiconductor Manufacturing Company Ltd

- Advanced Micro Devices

- Broadcom Limited

Recent Developments:

September 25, 2023: Samsung Electronics announced a new collaboration with AMD to advance 5G virtualized RAN (vRAN) for network transformation. This collaboration represents Samsung’s ongoing commitment to enriching vRAN and Open RAN ecosystems to help operators build and modernize mobile networks with unmatched flexibility and optimized performance.

JUNE 28, 2023: Imec, a leading research and innovation hub in nanoelectronics and digital technologies, and ASML Holding N.V. (ASML), a leading supplier to the semiconductor industry, announced that they intend to intensify their collaboration in the next phase of developing a state-of-the-art high-numerical aperture (High-NA) extreme ultraviolet (EUV) lithography pilot line at Imec.

Regional Analysis

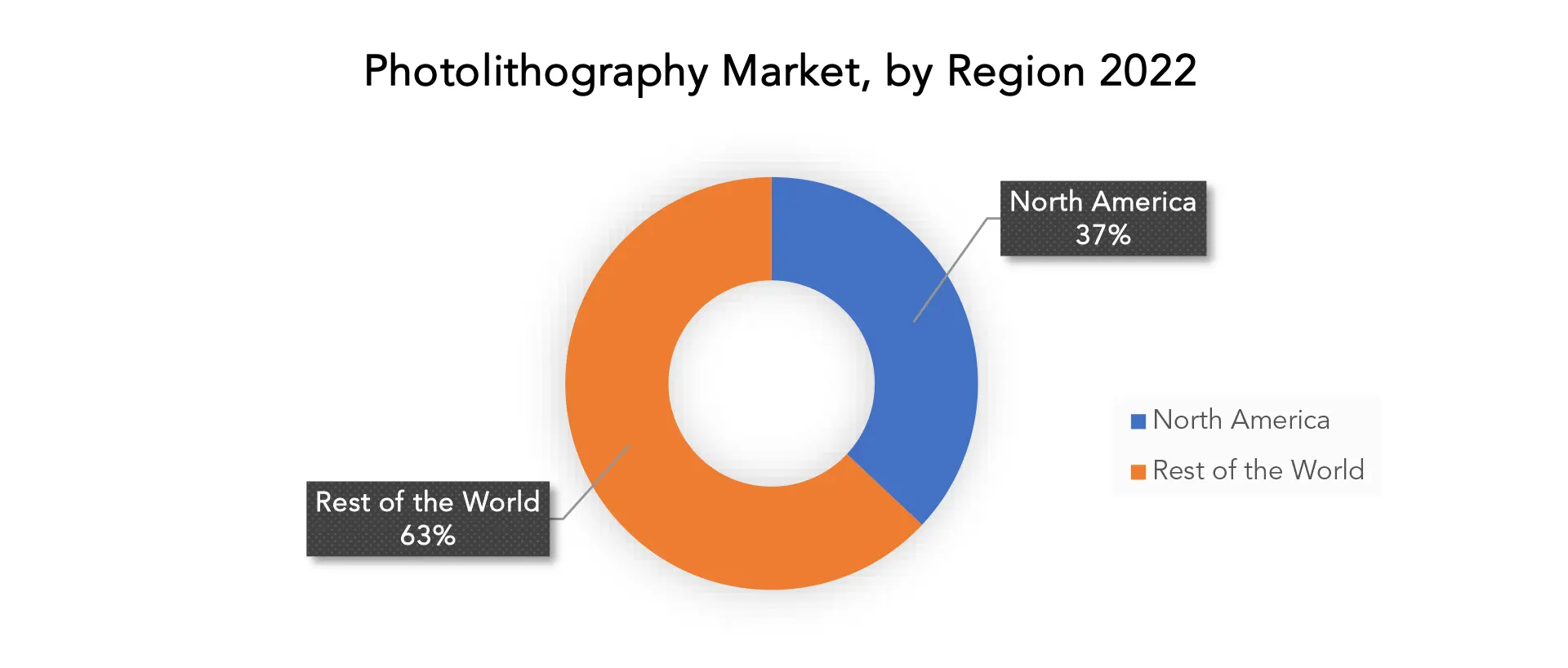

North America accounted for the largest market in the photolithography market. North America accounted for the 37 % market share of the global market value. The region has a strong and developed ecosystem for the production of semiconductors and electronics. Numerous industry leaders in semiconductors, cutting-edge IT firms, and prestigious research institutions call it home. As they work to innovate and create smaller, more potent, and energy-efficient microchips and electronic components, these organisations continuously feed the need for improved photolithography solutions. North America has benefited from significant investments in R&D, notably in semiconductor technology. This investment supports the development of next-generation lithography technologies and guarantees that the field remains at the forefront of industry technical breakthroughs. Furthermore, the presence of major semiconductor equipment manufacturers and suppliers in North America helps to market growth.

Furthermore, the region’s strong emphasis on innovation and technical leadership, in addition to an increased need for consumer electronics, automotive electronics, and telecommunications equipment, fuels the demand for accurate and sophisticated photolithography methods. As customers rely more on smartphones, tablets, IoT devices, and other high-tech gadgets, North American semiconductor makers are being forced to invest in cutting-edge lithography technology in order to fulfil the rising need for smaller, more powerful, and environmentally friendly processors.

North America’s dedication to meeting national security and defence objectives drives the photolithography business forward. Semiconductor technology is critical in military applications, and investments in defense-related electronics in the region contribute considerably to demand for sophisticated photolithography devices.

Target Audience for Photolithography Market

- Semiconductor Manufacturers

- Microelectronics Companies

- Integrated Circuit (IC) Manufacturers

- Research Institutions

- Equipment Suppliers and Manufacturers

- Technology Developers and Innovators in Lithography

- Semiconductor Foundries

- Electronics Manufacturing Services (EMS) Providers

- Semiconductor Equipment Distributors

- Government and Regulatory Bodies

- Quality Control and Testing Laboratories

- Original Equipment Manufacturers (OEMs) of Electronics Products

- Industrial and Consumer Electronics Manufacturers

Segments Covered in the Photolithography Market Report

Photolithography Market by Process

- Extreme Ultraviolet (EUV)

- Deep Ultraviolet (DUV)

- I-Line

- Krypton Fluoride (KrF)

- Argon Fluoride Dry (ArF Dry)

- Others

Photolithography Market by Light Source

- Mercury Lamps

- Fluorine Lasers

- Excimer Lasers

- Laser-Produced Plasma

Photolithography Market by Application

- IC Patterning Process

- Printed Circuit Board Fabrication

- Microprocessor Fabrication

- Others

Photolithography Market by Region

- North America

- Europe

- Asia Pacific

- South America

- Middle East and Africa

Key Question Answered

- What is the expected growth rate of the photolithography market over the next 7 years?

- Who are the major players in the Photolithography market and what is their market share?

- What are the end-user industries driving market demand and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-Pacific, the middle east, and Africa?

- How is the economic environment affecting the Photolithography market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the Photolithography market?

- What is the current and forecasted size and growth rate of the global Photolithography market?

- What are the key drivers of growth in the Photolithography market?

- Who are the major players in the market and what is their market share?

- What are the distribution channels and supply chain dynamics in the Photolithography market?

- What are the technological advancements and innovations in the Photolithography market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the Photolithography market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the Photolithography market?

- What are the product offerings and specifications of leading players in the market?

Table of Content

- INTRODUCTION

- MARKET DEFINITION

- MARKET SEGMENTATION

- RESEARCH TIMELINES

- ASSUMPTIONS AND LIMITATIONS

- RESEARCH METHODOLOGY

- DATA MINING

- SECONDARY RESEARCH

- PRIMARY RESEARCH

- SUBJECT-MATTER EXPERTS’ ADVICE

- QUALITY CHECKS

- FINAL REVIEW

- DATA TRIANGULATION

- BOTTOM-UP APPROACH

- TOP-DOWN APPROACH

- RESEARCH FLOW

- DATA SOURCES

- DATA MINING

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- GLOBAL PHOTOLITHOGRAPHY MARKET OUTLOOK

- MARKET DRIVERS

- MARKET RESTRAINTS

- MARKET OPPORTUNITIES

- IMPACT OF COVID-19 ON PHOTOLITHOGRAPHY MARKET

- PORTER’S FIVE FORCES MODEL

- THREAT FROM NEW ENTRANTS

- THREAT FROM SUBSTITUTES

- BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER OF CUSTOMERS

- DEGREE OF COMPETITION

- INDUSTRY VALUE CHAIN ANALYSIS

- GLOBAL PHOTOLITHOGRAPHY MARKET OUTLOOK

- GLOBAL PHOTOLITHOGRAPHY MARKET BY PROCESS, 2020-2030, (USD BILLION)

- EXTREME ULTRAVIOLET (EUV)

- DEEP ULTRAVIOLET (DUV)

- I-LINE

- KRYPTON FLUORIDE (KRF)

- ARGON FLUORIDE DRY (ARF DRY)

- OTHERS

- GLOBAL PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE, 2020-2030, (USD BILLION)

- MERCURY LAMPS

- FLUORINE LASERS

- EXCIMER LASERS

- LASER-PRODUCED PLASMA

- GLOBAL PHOTOLITHOGRAPHY MARKET BY APPLICATION, 2020-2030, (USD BILLION)

- IC PATTERNING PROCESS

- PRINTED CIRCUIT BOARD FABRICATION

- MICROPROCESSOR FABRICATION

- OTHERS

- GLOBAL PHOTOLITHOGRAPHY MARKET BY REGION, 2020-2030, (USD BILLION)

- NORTH AMERICA

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

- COMPANY PROFILES*

(BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCTS OFFERED, RECENT DEVELOPMENTS)

- ASML HOLDINGS, N.V

- NIKON CORPORATION

- CANON, INC

- JEOL LTD

- NUFLARE TECHNOLOGY

- ULTRATECH, INC

- RUDOLPH TECHNOLOGIES, INC

- SUSS MICTOTEC, A.G

- NIL TECHNOLOGY

- EV GROUP

- CARL ZEISS AG

- SAMSUNG ELECTRONICS

- TOKYO ELECTRON LIMITED

- APPLIED MATERIALS

- VEECO INSTRUMENTS INC

- VISTEC ELECTRON BEAM GMBH

- SHANGHAI MICROELECTRONICS EQUIPMENT GROUP

- TAIWAN SEMICONDUCTOR MANUFACTURING COMPANY LTD

- ADVANCED MICRO DEVICES

- BROADCOM LIMITED

*THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 2 GLOBAL PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 3 GLOBAL PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 4 GLOBAL PHOTOLITHOGRAPHY MARKET BY REGION (USD BILLION) 2020-2030

TABLE 5 NORTH AMERICA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 6 NORTH AMERICA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 7 NORTH AMERICA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 8 NORTH AMERICA PHOTOLITHOGRAPHY MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 9 US PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 10 US PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 11 US PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 12 CANADA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 13 CANADA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 14 CANADA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 15 MEXICO PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 16 MEXICO PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 17 MEXICO PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 18 SOUTH AMERICA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 19 SOUTH AMERICA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 20 SOUTH AMERICA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 21 SOUTH AMERICA PHOTOLITHOGRAPHY MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 22 BRAZIL PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 23 BRAZIL PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 24 BRAZIL PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 25 ARGENTINA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 26 ARGENTINA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 27 ARGENTINA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 28 COLOMBIA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 29 COLOMBIA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 30 COLOMBIA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 31 REST OF SOUTH AMERICA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 32 REST OF SOUTH AMERICA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 33 REST OF SOUTH AMERICA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 34 ASIA-PACIFIC PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 35 ASIA-PACIFIC PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 36 ASIA-PACIFIC PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 37 ASIA-PACIFIC PHOTOLITHOGRAPHY MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 38 INDIA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 39 INDIA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 40 INDIA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 41 CHINA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 42 CHINA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 43 CHINA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 44 JAPAN PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 45 JAPAN PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 46 JAPAN PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 47 SOUTH KOREA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 48 SOUTH KOREA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 49 SOUTH KOREA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 50 AUSTRALIA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 51 AUSTRALIA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 52 AUSTRALIA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 53 SOUTH-EAST ASIA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 54 SOUTH-EAST ASIA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 55 SOUTH-EAST ASIA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 56 REST OF ASIA PACIFIC PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 57 REST OF ASIA PACIFIC PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 58 REST OF ASIA PACIFIC PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 59 EUROPE PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 60 EUROPE PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 61 EUROPE PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 62 EUROPE PHOTOLITHOGRAPHY MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 63 GERMANY PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 64 GERMANY PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 65 GERMANY PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 66 UK PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 67 UK PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 68 UK PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 69 FRANCE PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 70 FRANCE PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 71 FRANCE PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 72 ITALY PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 73 ITALY PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 74 ITALY PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 75 SPAIN PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 76 SPAIN PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 77 SPAIN PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 78 RUSSIA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 79 RUSSIA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 80 RUSSIA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 81 REST OF EUROPE PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 82 REST OF EUROPE PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 83 REST OF EUROPE PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 84 MIDDLE EAST AND AFRICA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 85 MIDDLE EAST AND AFRICA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 86 MIDDLE EAST AND AFRICA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 87 MIDDLE EAST AND AFRICA PHOTOLITHOGRAPHY MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 88 UAE PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 89 UAE PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 90 UAE PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 91 SAUDI ARABIA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 92 SAUDI ARABIA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 93 SAUDI ARABIA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 94 SOUTH AFRICA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 95 SOUTH AFRICA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 96 SOUTH AFRICA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

TABLE 97 REST OF MIDDLE EAST AND AFRICA PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

TABLE 98 REST OF MIDDLE EAST AND AFRICA PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

TABLE 99 REST OF MIDDLE EAST AND AFRICA PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2020-2030

FIGURE 9 GLOBAL PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2020-2030

FIGURE 10 GLOBAL PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2020-2030

FIGURE 11 GLOBAL PHOTOLITHOGRAPHY MARKET BY REGION (USD BILLION) 2020-2030

FIGURE 12 PORTER’S FIVE FORCES MODEL

FIGURE 13 GLOBAL PHOTOLITHOGRAPHY MARKET BY PROCESS (USD BILLION) 2022

FIGURE 14 GLOBAL PHOTOLITHOGRAPHY MARKET BY LIGHT SOURCE (USD BILLION) 2022

FIGURE 15 GLOBAL PHOTOLITHOGRAPHY MARKET BY APPLICATION (USD BILLION) 2022

FIGURE 16 GLOBAL PHOTOLITHOGRAPHY MARKET BY REGION (USD BILLION) 2022

FIGURE 17 MARKET SHARE ANALYSIS

FIGURE 18 ASML HOLDINGS, N.V: COMPANY SNAPSHOT

FIGURE 19 NIKON CORPORATION: COMPANY SNAPSHOT

FIGURE 20 CANON, INC: COMPANY SNAPSHOT

FIGURE 21 JEOL LTD: COMPANY SNAPSHOT

FIGURE 22 NUFLARE TECHNOLOGY: COMPANY SNAPSHOT

FIGURE 23 ULTRATECH, INC: COMPANY SNAPSHOT

FIGURE 24 RUDOLPH TECHNOLOGIES, INC: COMPANY SNAPSHOT

FIGURE 25 SUSS MICTOTEC, A.G: COMPANY SNAPSHOT

FIGURE 26 NIL TECHNOLOGY: COMPANY SNAPSHOT

FIGURE 27 EV GROUP: COMPANY SNAPSHOT

FIGURE 28 CARL ZEISS AG: COMPANY SNAPSHOT

FIGURE 29 SAMSUNG ELECTRONICS: COMPANY SNAPSHOT

FIGURE 30 TOKYO ELECTRON LIMITED: COMPANY SNAPSHOT

FIGURE 31 APPLIED MATERIALS: COMPANY SNAPSHOT

FIGURE 32 VEECO INSTRUMENTS INC: COMPANY SNAPSHOT

FIGURE 33 VISTEC ELECTRON BEAM GMBH: COMPANY SNAPSHOT

FIGURE 34 SHANGHAI MICROELECTRONICS EQUIPMENT GROUP: COMPANY SNAPSHOT

FIGURE 35 TAIWAN SEMICONDUCTOR MANUFACTURING COMPANY LTD: COMPANY SNAPSHOT

FIGURE 36 ADVANCED MICRO DEVICES: COMPANY SNAPSHOT

FIGURE 37 BROADCOM LIMITED: COMPANY SNAPSHOT

FAQ

The global photolithography market is expected to grow from USD 9.05 Billion in 2023 to USD 12.99 Billion by 2030, at a CAGR of 5.30 % during the forecast period.

North America accounted for the largest market in the photolithography market. North America accounted for 37 % market share of the global market value.

ASML Holdings, N.V, Nikon Corporation, Canon, Inc., JEOL Ltd, NuFlare Technology, Ultratech, Inc., Rudolph Technologies, Inc., SUSS Mictotec, A.G, Nil Technology, EV Group, Carl Zeiss AG, Samsung Electronics, Tokyo Electron Limited, Applied Materials, Veeco Instruments Inc., Vistec Electron Beam GMBH, Shanghai Microelectronics equipment group, Taiwan Semiconductor Manufacturing Company Ltd, Advanced Micro Devices, Broadcom Limited

The photolithography market includes the increasing demand for advanced semiconductor manufacturing technologies to support the development of smaller and more powerful electronic devices, as well as the adoption of extreme ultraviolet (EUV) lithography for improved precision and efficiency in semiconductor production.

In-Depth Database

Our Report’s database covers almost all topics of all regions over the Globe.

Recognised Publishing Sources

Tie ups with top publishers around the globe.

Customer Support

Complete pre and post sales

support.

Safe & Secure

Complete secure payment

process.