INTERESTED IN THIS RESEARCH?

Contact our analysts for inquiries, samples, and expert insights.

REPORT OUTLOOK

| Market Size | CAGR | Dominating Region |

|---|---|---|

| USD 4.16 Trillion by 2030 | 3.32 % | North America |

| by Input Suppliers | by Production | by Processing & Distribution |

|---|---|---|

|

|

|

SCOPE OF THE REPORT

Agribusiness Market Overview

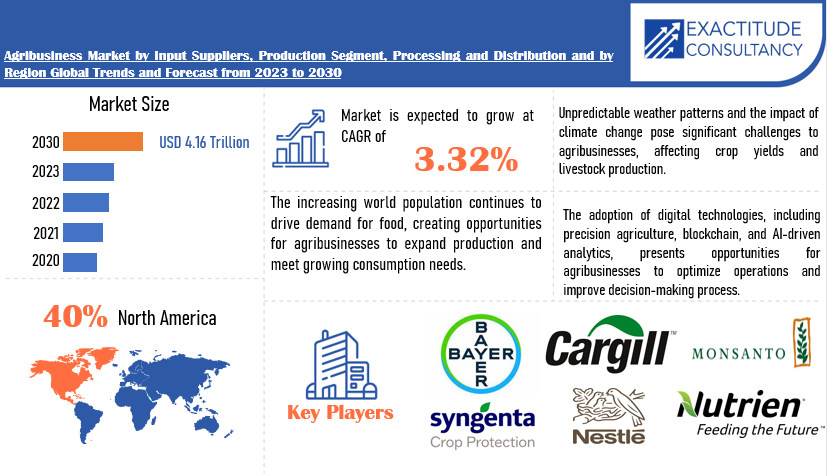

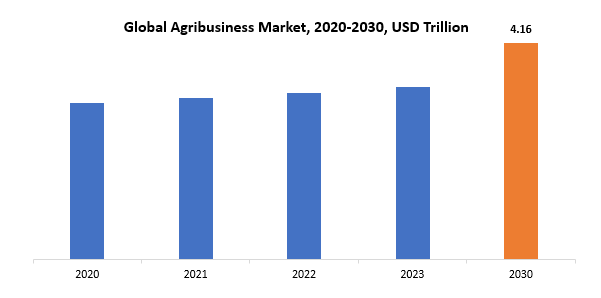

The global agribusiness market is anticipated to grow from USD 3.31 Trillion in 2023 to USD 4.16 Trillion by 2030, at a CAGR of 3.32 % during the forecast period.

Agribusiness constitutes a comprehensive and interconnected industry that integrates agricultural production, processing, distribution, and marketing activities. It encompasses a diverse range of tasks associated with the production and commercialization of agricultural goods and services. Going beyond traditional farming methods, agribusiness involves multiple stakeholders, including farmers, processors, distributors, retailers, and consumers. Utilizing modern technologies, management techniques, and business strategies, this sector aims to optimize efficiency, productivity, and sustainability across the entire agricultural value chain. Agribusiness covers various domains such as crop cultivation, livestock farming, agrochemicals, food processing, and distribution. Globally, the agribusiness industry is pivotal in addressing the growing demand for food, feed, fiber, and bioenergy, making substantial contributions to economic development, rural livelihoods, and global food security.

The growing global population acts as a primary driver, increasing the demand for food and agricultural products. This necessitates advancements in agricultural practices, technologies, and supply chain management to meet the rising consumption needs. Secondly, the adoption of modern technologies and precision agriculture plays a crucial role in enhancing productivity and efficiency throughout the agribusiness sector. Technologies such as drones, IoT devices, and data analytics enable farmers and agribusinesses to make informed decisions, optimize resource use, and improve overall yields.

Moreover, the increasing focus on sustainability and environmentally friendly practices is a significant driver. Consumers and regulatory bodies are increasingly demanding sustainable and ethical production methods, leading agribusinesses to adopt practices that reduce environmental impact and promote resource conservation. Additionally, the rise of e-commerce and digital platforms in agribusiness facilitates streamlined communication, efficient transactions, and improved market access for both farmers and consumers.

Furthermore, the globalization of food markets and the expansion of international trade contribute to the growth of the agribusiness market. Agribusinesses are exploring new markets and opportunities globally, driving innovation and competitiveness. The awareness and demand for organic and natural products also drive agribusiness practices towards more sustainable and health-conscious approaches.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2030 |

| Base year | 2022 |

| Estimated year | 2023 |

| Forecasted year | 2023-2030 |

| Historical period | 2019-2021 |

| Unit | Value (USD Trillion) |

| Segmentation | By Input Suppliers, Production Segment, Processing & Distribution and Region |

| By Input Suppliers |

|

| By Production Segment |

|

| By Processing & Distribution |

|

|

By Region

|

|

Agribusiness Market Segmentation Analysis

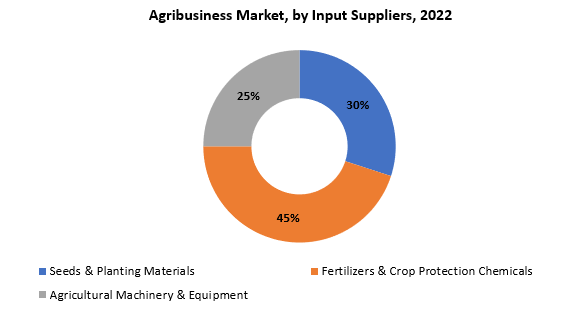

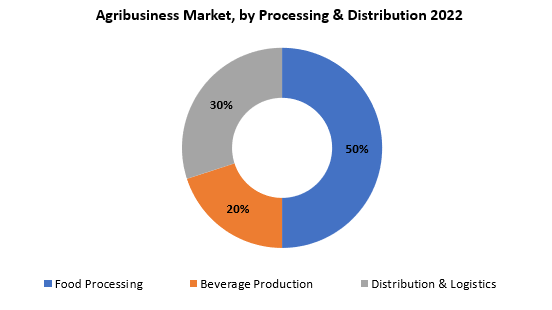

The global Agribusiness market is divided into three segments, technology, product type, application and region. By product type the market is divided Seeds & Planting Materials, Fertilizers & Crop Protection Chemicals, Agricultural Machinery & Equipment. By Production Segment the market is classified into Crop Production, Livestock Production, Aquaculture. By Processing & Distribution the market is classified into Food Processing, Beverage Production, Distribution & Logistics.

Based on input suppliers, fertilizers & crop protection chemicals segment dominating in the agribusiness market. Fertilizers, encompassing various nutrients essential for plant growth, are critical for enhancing soil fertility and optimizing crop yields. They provide plants with the necessary elements like nitrogen, phosphorus, and potassium, contributing to robust and healthy crop development. Crop protection chemicals, including pesticides and herbicides, are equally vital in safeguarding crops from pests, diseases, and weeds, ensuring a successful harvest.

The dominance of the fertilizers and crop protection chemicals segment reflects the industry’s dependence on efficient and productive agricultural practices. Farmers rely on these inputs to address soil nutrient deficiencies and protect their crops from potential threats, thereby maximizing their output. The continuous advancement in agricultural technology has led to the development of specialized fertilizers and innovative crop protection solutions that enhance precision farming and minimize environmental impact.

Moreover, the segment’s dominance underscores the global emphasis on increasing agricultural productivity to meet the rising demand for food. As the world population grows, the need to produce more food efficiently and sustainably becomes imperative, making the role of input suppliers, particularly in fertilizers and crop protection, crucial for addressing global food security challenges.

Based on processing & distribution, food processing segment dominating in the agribusiness market. Food processing plays a central role in transforming raw agricultural products into consumable goods, adding value to the supply chain and meeting the diverse demands of consumers. This segment encompasses a myriad of activities such as sorting, cleaning, packaging, and preserving agricultural produce.

The dominance of the food processing segment is indicative of the growing importance of processed food in modern diets and the evolving preferences of consumers for convenience, variety, and longer shelf life. Food processing not only extends the lifespan of perishable products but also allows for the creation of diverse and innovative food products. Furthermore, it enables the development of value-added items, such as ready-to-eat meals, snacks, and packaged goods, contributing to the overall economic value of the agribusiness sector. The global food processing industry plays a crucial role in reducing food wastage by optimizing the use of raw materials and ensuring the efficient utilization of agricultural outputs. Moreover, it facilitates the distribution of food products across various geographical locations, contributing to the globalization of food markets.

Agribusiness Market Dynamics

Driver

Innovations in agricultural technology, such as precision farming, genetic engineering, and IoT applications, enhance productivity and efficiency in agribusiness operations.

Precision farming, a key component of this technological revolution, involves the use of advanced systems such as GPS-guided tractors and drones to optimize various aspects of crop management. This precision allows farmers to precisely apply resources like fertilizers and pesticides, reducing waste, minimizing environmental impact, and enhancing overall crop yields. Genetic engineering, another groundbreaking innovation, enables the development of genetically modified (GM) crops with desirable traits, such as resistance to pests, diseases, or adverse environmental conditions. These genetically enhanced crops often exhibit improved yields, resilience, and nutritional profiles, addressing challenges related to food security and sustainability.

Internet of Things (IoT) applications have further amplified the efficiency of agribusiness operations. IoT devices, such as soil sensors, weather stations, and automated machinery, facilitate real-time data collection and analysis. Farmers can monitor soil conditions, weather patterns, and crop health remotely, enabling informed decision-making and timely interventions. This connectivity not only streamlines operations but also empowers farmers to respond promptly to changing environmental factors, thereby optimizing resource utilization. The integration of these technologies creates a comprehensive and interconnected system that enhances every stage of agribusiness. From precise planting and monitoring to data-driven decision-making, these innovations contribute to sustainable practices, cost-effectiveness, and resilience in the face of unpredictable environmental challenges.

Restraint

Unpredictable weather patterns and the impact of climate change pose significant challenges to agribusinesses, affecting crop yields and livestock production.

Changes in temperature, precipitation, and extreme weather events disrupt traditional growing seasons and agricultural calendars, leading to increased uncertainty for farmers. Shifts in precipitation patterns, including irregular rainfall and prolonged droughts, can result in water scarcity, negatively influencing crop growth and stressing livestock. Rising temperatures and altered climate conditions also create favorable environments for the proliferation of pests, diseases, and invasive species, posing additional threats to agricultural productivity. Changes in temperature regimes can disturb the delicate balance of ecosystems, affecting the natural cycles of pollinators and beneficial organisms essential for crop health.

Extreme weather events, such as floods, hurricanes, and wildfires, further exacerbate the challenges faced by agribusinesses. These events can lead to soil erosion, crop damage, and the destruction of infrastructure, disrupting the entire agricultural supply chain. Livestock, too, face increased vulnerability to heat stress and diseases under changing climatic conditions, impacting their overall well-being and productivity.

The cumulative effect of these climate-related challenges is a heightened risk of yield variability, decreased crop quality, and increased production costs for agribusinesses. Farmers are compelled to adopt adaptive strategies, including the selection of climate-resilient crop varieties, water-efficient irrigation practices, and the implementation of precision agriculture technologies to mitigate the impacts of climate change.

Opportunities

The adoption of digital technologies, including precision agriculture, blockchain, and AI-driven analytics, presents opportunities for agribusinesses market.

Precision agriculture stands at the forefront of this digital revolution, leveraging technologies such as GPS, sensors, and automated machinery to optimize various aspects of farming practices. Farmers can precisely monitor and manage field variability, enabling targeted application of resources like fertilizers and pesticides. This not only improves resource efficiency but also minimizes environmental impact and enhances overall crop yields.

lockchain technology has introduced a new era of transparency and traceability in the agribusiness sector. By creating secure and immutable ledgers, blockchain enables the tracking of agricultural products throughout the supply chain. This has profound implications for food safety, allowing consumers to access real-time information about the origin, production, and distribution of the products they consume. Additionally, blockchain enhances trust and collaboration among supply chain stakeholders, reducing fraud, mitigating risks, and facilitating more efficient transactions.

Artificial Intelligence (AI)-driven analytics represents another key opportunity for agribusinesses. AI algorithms can analyze vast amounts of data, including weather patterns, soil conditions, and historical crop performance, providing actionable insights for decision-making. AI-powered systems can predict crop diseases, optimize irrigation schedules, and recommend personalized strategies for crop management.

Agribusiness Market Trends

-

The adoption of digital technologies, including IoT devices, drones, and data analytics, continues to rise. Precision agriculture allows farmers to make data-driven decisions, optimize resource use, and improve overall farm efficiency.

-

The use of blockchain in agribusiness for supply chain transparency and traceability has gained momentum. Blockchain helps in tracking the journey of agricultural products from farm to fork, ensuring authenticity and improving food safety.

-

There is a growing emphasis on sustainable and regenerative agricultural practices. Agribusinesses are increasingly adopting eco-friendly approaches to farming, which includes organic farming, agroecology, and conservation practices.

-

The increasing demand for alternative protein sources, including plant-based and lab-grown meat, is influencing the agribusiness landscape. Companies are diversifying their product offerings to meet the rising demand for alternative protein options.

-

The integration of smart technologies such as robotics, autonomous vehicles, and sensor networks is enhancing automation in farming operations. This trend contributes to increased efficiency and reduced labor requirements.

-

The use of data analytics and artificial intelligence for crop monitoring, disease prediction, and yield optimization is becoming more prevalent. These technologies help farmers make informed decisions for better crop management.

Competitive Landscape

The competitive landscape of the agribusiness market was dynamic, with several prominent companies competing to provide innovative and advanced agribusiness solutions.

- Bayer CropScience, LLC

- Cargill, Inc.

- The Monsanto Company

- Syngenta Crop Protection

- Nestlé S.A.

- Wilmer International Limited

- Associated British Foods PLC

- Brasil Agro

- Bunge Limited

- Cairo Poultry Company

- CHS, Inc.

- LT Foods, Ltd.

- Nutrien

- Deere & Company

- BASF SE

- CNH Industrial N. V.

- The Archer-Daniels-Midland Company

- ABP Food Group

- COFCO Corporation

- Unilever plc

Recent Developments:

-

March 30, 2023: Cargill and food tech leader ENOUGH, which produces fermented protein sustainably, are expanding their current partnership to further innovate nutritious and sustainable alternative meat and dairy solutions consumers crave.

-

October 24, 2023: – Silal1 and Bayer2, a global leader in life sciences with a strong focus on healthcare and nutrition, have joined forces in a pioneering collaboration set to strengthen the agricultural landscape in the United Arab Emirates (UAE), addressing climate change as a pivotal concern.

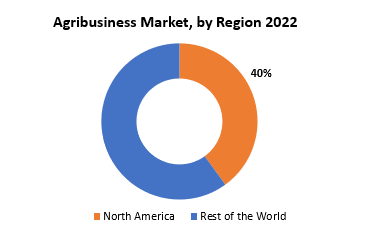

Regional Analysis

North America accounted for the largest market in the agribusiness market. North America accounted for 40 % market share of the global market value. North America has consistently held a dominant position in the global agribusiness market, reflecting the region’s robust and diverse agricultural sector, technological advancements, and sophisticated supply chain infrastructure. The United States, Canada, and Mexico collectively contribute to the region’s prominence in agribusiness. The vast and varied geography of North America supports a wide range of agricultural activities, including crop cultivation, livestock farming, and agro-processing.

In the United States, large-scale commercial farming operations leverage advanced technologies such as precision agriculture, genetically modified crops, and automated machinery. This technological sophistication enhances productivity, efficiency, and the overall competitiveness of the agricultural sector. The U.S. is a major producer of key crops such as corn, soybeans, and wheat, and it has a well-established livestock industry.

Canada, with its extensive arable land and favorable climate conditions in certain regions, is a major contributor to the agribusiness market. The country is known for its production of canola, barley, and various fruits, as well as its significant livestock sector, including cattle and poultry. Mexico plays a crucial role in North America’s agribusiness landscape, combining traditional agricultural practices with modern approaches. The country is a leading exporter of fruits and vegetables, such as tomatoes, avocados, and berries, to North American and international markets.

In Europe, agribusiness is deeply intertwined with the continent’s rich history of agriculture and diverse climates. The European Union (EU) member states collectively contribute to the region’s strong position in the global agribusiness market. The Common Agricultural Policy (CAP) of the EU plays a crucial role in shaping agricultural practices, ensuring food security, and supporting rural development. European agriculture encompasses a wide range of activities, from large-scale commercial farming in countries like France and Germany to specialized and high-value agriculture in the Netherlands. The region is known for producing a variety of crops, including wheat, barley, grapes, and olive oil.

The Asia-Pacific region is characterized by its diverse agricultural systems, ranging from traditional subsistence farming to highly mechanized commercial agriculture. Countries like China, India, Japan, and Australia contribute significantly to the agribusiness market in this region. China, as a major global agricultural producer, plays a pivotal role in the Asia-Pacific market. The region is known for the cultivation of staple crops such as rice, wheat, and soybeans, which form the dietary foundation for a large portion of the population. In addition to traditional farming methods, there is a growing emphasis on modernization and technology adoption in countries like Japan and Australia, leading to increased efficiency and productivity.

Target Audience for Agribusiness Market

- Farmers and Agricultural Producers

- Agribusiness Companies

- Investors and Financial Institutions

- Government Agencies

- Technology Providers

- Research and Development Institutions

- Supply Chain and Logistics Providers

- Trade Associations and Industry Groups

- AgTech Startups

- Insurance Companies

- Educational Institutions

Segments Covered in the Agribusiness Market Report

Agribusiness Market by Input Suppliers

- Seeds & Planting Materials

- Fertilizers & Crop Protection Chemicals

- Agricultural Machinery & Equipment

Agribusiness Market by Production Segment

- Crop Production

- Livestock Production

- Aquaculture

Agribusiness Market by Processing & Distribution

- Food Processing

- Beverage Production

- Distribution & Logistics

Agribusiness Market by Region

- North America

- Europe

- Asia Pacific

- South America

- Middle East and Africa

Key Question Answered

- What is the expected growth rate of the agribusiness market over the next 7 years?

- Who are the major players in the Agribusiness market and what is their market share?

- What are the end-user industries driving market demand and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-Pacific, the middle east, and Africa?

- How is the economic environment affecting the Agribusiness market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the Agribusiness market?

- What is the current and forecasted size and growth rate of the global Agribusiness market?

- What are the key drivers of growth in the Agribusiness market?

- Who are the major players in the market and what is their market share?

- What are the distribution channels and supply chain dynamics in the Agribusiness market?

- What are the technological advancements and innovations in the Agribusiness market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the agribusiness market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the Agribusiness market?

- What are the service offerings and specifications of leading players in the market?

Table of Content

- INTRODUCTION

- MARKET DEFINITION

- MARKET SEGMENTATION

- RESEARCH TIMELINES

- ASSUMPTIONS AND LIMITATIONS

- RESEARCH METHODOLOGY

- DATA MINING

- SECONDARY RESEARCH

- PRIMARY RESEARCH

- SUBJECT-MATTER EXPERTS’ ADVICE

- QUALITY CHECKS

- FINAL REVIEW

- DATA TRIANGULATION

- BOTTOM-UP APPROACH

- TOP-DOWN APPROACH

- RESEARCH FLOW

- DATA SOURCES

- DATA MINING

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- GLOBAL AGRIBUSINESS MARKET OUTLOOK

- MARKET DRIVERS

- MARKET RESTRAINTS

- MARKET OPPORTUNITIES

- IMPACT OF COVID-19 ON AGRIBUSINESS MARKET

- PORTER’S FIVE FORCES MODEL

- THREAT FROM NEW ENTRANTS

- THREAT FROM SUBSTITUTES

- BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER OF CUSTOMERS

- DEGREE OF COMPETITION

- PROCESSING & DISTRIBUTION VALUE CHAIN ANALYSIS

- GLOBAL AGRIBUSINESS MARKET OUTLOOK

- GLOBAL AGRIBUSINESS MARKET BY INPUT SUPPLIERS, 2020-2030, (USD TRILLION)

- SEEDS & PLANTING MATERIALS

- FERTILIZERS & CROP PROTECTION CHEMICALS

- AGRICULTURAL MACHINERY & EQUIPMENT

- GLOBAL AGRIBUSINESS MARKET BY PRODUCTION SEGMENT, 2020-2030, (USD TRILLION)

- CROP PRODUCTION

- LIVESTOCK PRODUCTION

- AQUACULTURE

- GLOBAL AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION, 2020-2030, (USD TRILLION)

- FOOD PROCESSING

- BEVERAGE PRODUCTION

- DISTRIBUTION & LOGISTICS

- GLOBAL AGRIBUSINESS MARKET BY REGION, 2020-2030, (USD TRILLION)

- NORTH AMERICA

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

- COMPANY PROFILES*

(BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCTS OFFERED, RECENT DEVELOPMENTS)

- BAYER CROPSCIENCE, LLC

- CARGILL, INC.

- THE MONSANTO COMPANY

- SYNGENTA CROP PROTECTION

- NESTLÉ S.A.

- WILMER INTERNATIONAL LIMITED

- ASSOCIATED BRITISH FOODS PLC

- BRASIL AGRO

- BUNGE LIMITED

- CAIRO POULTRY COMPANY

- CHS, INC.

- LT FOODS, LTD.

- NUTRIEN

- DEERE & COMPANY

- BASF SE

- CNH INDUSTRIAL N. V.

- THE ARCHER-DANIELS-MIDLAND COMPANY

- ABP FOOD GROUP

- COFCO CORPORATION

- UNILEVER PLC *THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 2 GLOBAL AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 3 GLOBAL AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 4 GLOBAL AGRIBUSINESS MARKET BY REGION (USD TRILLION) 2020-2030

TABLE 5 NORTH AMERICA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 6 NORTH AMERICA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 7 NORTH AMERICA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 8 NORTH AMERICA AGRIBUSINESS MARKET BY COUNTRY (USD TRILLION) 2020-2030

TABLE 9 US AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 10 US AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 11 US AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 12 CANADA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 13 CANADA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 14 CANADA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 15 MEXICO AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 16 MEXICO AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 17 MEXICO AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 18 SOUTH AMERICA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 19 SOUTH AMERICA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 20 SOUTH AMERICA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 21 SOUTH AMERICA AGRIBUSINESS MARKET BY COUNTRY (USD TRILLION) 2020-2030

TABLE 22 BRAZIL AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 23 BRAZIL AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 24 BRAZIL AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 25 ARGENTINA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 26 ARGENTINA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 27 ARGENTINA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 28 COLOMBIA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 29 COLOMBIA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 30 COLOMBIA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 31 REST OF SOUTH AMERICA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 32 REST OF SOUTH AMERICA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 33 REST OF SOUTH AMERICA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 34 ASIA-PACIFIC AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 35 ASIA-PACIFIC AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 36 ASIA-PACIFIC AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 37 ASIA-PACIFIC AGRIBUSINESS MARKET BY COUNTRY (USD TRILLION) 2020-2030

TABLE 38 INDIA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 39 INDIA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 40 INDIA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 41 CHINA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 42 CHINA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 43 CHINA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 44 JAPAN AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 45 JAPAN AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 46 JAPAN AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 47 SOUTH KOREA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 48 SOUTH KOREA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 49 SOUTH KOREA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 50 AUSTRALIA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 51 AUSTRALIA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 52 AUSTRALIA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 53 SOUTH-EAST ASIA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 54 SOUTH-EAST ASIA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 55 SOUTH-EAST ASIA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 56 REST OF ASIA PACIFIC AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 57 REST OF ASIA PACIFIC AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 58 REST OF ASIA PACIFIC AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 59 EUROPE AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 60 EUROPE AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 61 EUROPE AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 62 EUROPE AGRIBUSINESS MARKET BY COUNTRY (USD TRILLION) 2020-2030

TABLE 63 GERMANY AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 64 GERMANY AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 65 GERMANY AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 66 UK AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 67 UK AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 68 UK AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 69 FRANCE AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 70 FRANCE AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 71 FRANCE AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 72 ITALY AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 73 ITALY AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 74 ITALY AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 75 SPAIN AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 76 SPAIN AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 77 SPAIN AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 78 RUSSIA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 79 RUSSIA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 80 RUSSIA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 81 REST OF EUROPE AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 82 REST OF EUROPE AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 83 REST OF EUROPE AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 84 MIDDLE EAST AND AFRICA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 85 MIDDLE EAST AND AFRICA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 86 MIDDLE EAST AND AFRICA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 87 MIDDLE EAST AND AFRICA AGRIBUSINESS MARKET BY COUNTRY (USD TRILLION) 2020-2030

TABLE 88 UAE AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 89 UAE AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 90 UAE AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 91 SAUDI ARABIA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 92 SAUDI ARABIA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 93 SAUDI ARABIA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 94 SOUTH AFRICA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 95 SOUTH AFRICA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 96 SOUTH AFRICA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

TABLE 97 REST OF MIDDLE EAST AND AFRICA AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

TABLE 98 REST OF MIDDLE EAST AND AFRICA AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

TABLE 99 REST OF MIDDLE EAST AND AFRICA AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2020-2030

FIGURE 9 GLOBAL AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2020-2030

FIGURE 10 GLOBAL AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2020-2030

FIGURE 11 GLOBAL AGRIBUSINESS MARKET BY REGION (USD TRILLION) 2020-2030

FIGURE 12 PORTER’S FIVE FORCES MODEL

FIGURE 13 GLOBAL AGRIBUSINESS MARKET BY INPUT SUPPLIERS (USD TRILLION) 2022

FIGURE 14 GLOBAL AGRIBUSINESS MARKET BY PRODUCTION SEGMENT (USD TRILLION) 2022

FIGURE 15 GLOBAL AGRIBUSINESS MARKET BY PROCESSING & DISTRIBUTION (USD TRILLION) 2022

FIGURE 16 GLOBAL AGRIBUSINESS MARKET BY REGION (USD TRILLION) 2021

FIGURE 17 MARKET SHARE ANALYSIS

FIGURE 18 BAYER CROPSCIENCE, LLC: COMPANY SNAPSHOT

FIGURE 19 CARGILL, INC.: COMPANY SNAPSHOT

FIGURE 20 THE MONSANTO COMPANY: COMPANY SNAPSHOT

FIGURE 21 SYNGENTA CROP PROTECTION: COMPANY SNAPSHOT

FIGURE 22 NESTLÉ S.A.: COMPANY SNAPSHOT

FIGURE 23 WILMER INTERNATIONAL LIMITED: COMPANY SNAPSHOT

FIGURE 24 ASSOCIATED BRITISH FOODS PLC: COMPANY SNAPSHOT

FIGURE 25 BRASIL AGRO: COMPANY SNAPSHOT

FIGURE 26 BUNGE LIMITED: COMPANY SNAPSHOT

FIGURE 27 CAIRO POULTRY COMPANY: COMPANY SNAPSHOT

FIGURE 28 CHS, INC.: COMPANY SNAPSHOT

FIGURE 29 LT FOODS, LTD.: COMPANY SNAPSHOT

FIGURE 30 NUTRIEN: COMPANY SNAPSHOT

FIGURE 31 DEERE & COMPANY: COMPANY SNAPSHOT

FIGURE 32 BASF SE: COMPANY SNAPSHOT

FIGURE 33 CNH INDUSTRIAL N. V.: COMPANY SNAPSHOT

FIGURE 34 THE ARCHER-DANIELS-MIDLAND COMPANY: COMPANY SNAPSHOT

FIGURE 35 ABP FOOD GROUP: COMPANY SNAPSHOT

FIGURE 36 COFCO CORPORATION: COMPANY SNAPSHOT

FIGURE 37 UNILEVER PLC: COMPANY SNAPSHOT

FAQ

The global agribusiness market is anticipated to grow from USD 3.31 Trillion in 2023 to USD 4.16 Trillion by 2030, at a CAGR of 3.32 % during the forecast period.

North America accounted for the largest market in the agribusiness market. North America accounted for 40 % market share of the global market value.

Bayer CropScience, LLC, Cargill, Inc., The Monsanto Company, Syngenta Crop Protection, Nestlé S.A., Wilmer International Limited, Associated British Foods PLC, Brasil Agro, Bunge Limited, Cairo Poultry Company, CHS, Inc., LT Foods, Ltd., Nutrien, Deere & Company, BASF SE, CNH Industrial N. V., The Archer-Daniels-Midland Company, ABP Food Group, COFCO Corporation, Unilever plc.

Key trends in the agribusiness market include a growing emphasis on sustainable and eco-friendly activewear, the integration of technology for enhanced performance, and the rise of athleisure, where activewear seamlessly transitions into casual wear. Additionally, personalized and inclusive sizing options are becoming more prevalent as brands strive to cater to a diverse range of body types and preferences, reflecting a shift towards inclusivity and body positivity in the industry.

In-Depth Database

Our Report’s database covers almost all topics of all regions over the Globe.

Recognised Publishing Sources

Tie ups with top publishers around the globe.

Customer Support

Complete pre and post sales

support.

Safe & Secure

Complete secure payment

process.