Base Year Value ()

x.x %

x.x %

CAGR ()

x.x %

x.x %

Forecast Year Value ()

x.x %

x.x %

Historical Data Period

Largest Region

Forecast Period

Mercado de integración de sistemas de combate por plataforma (grandes buques de combate, buques de combate medianos, helicópteros, buques de combate pequeños, submarinos, aviones de combate, vehículos blindados/artillería, helicópteros de combate), aplicación (naval, aerotransportada y terrestre) y por región Tendencias globales y pronóstico de 2022 a 2029

Instant access to hundreds of data points and trends

- Market estimates from 2014-2029

- Competitive analysis, industry segmentation, financial benchmarks

- Incorporates SWOT, Porter's Five Forces and risk management frameworks

- PDF report or online database with Word, Excel and PowerPoint export options

- 100% money back guarantee

Descripción general del mercado de integración de sistemas de combate

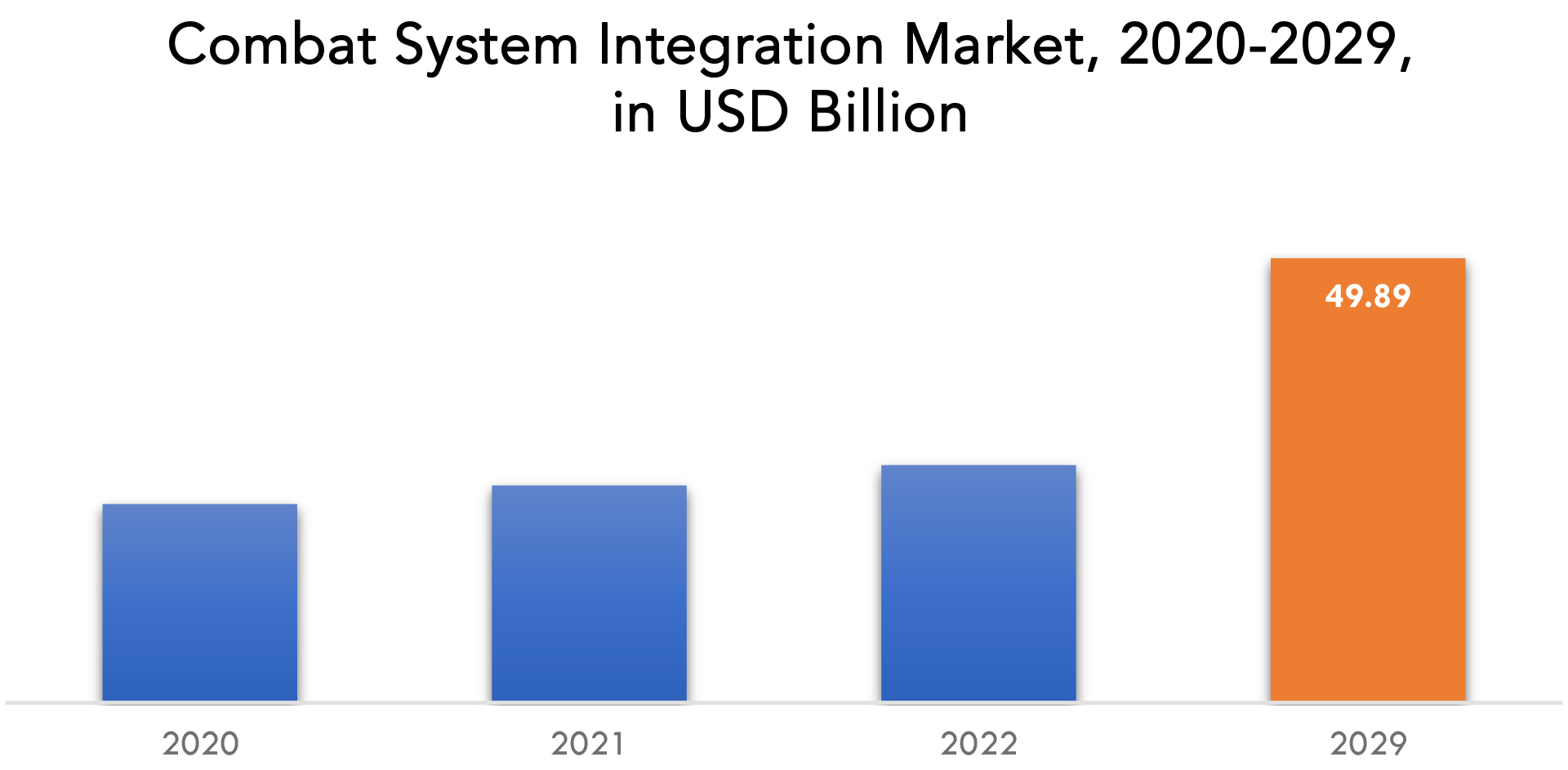

Se proyecta que el mercado global de integración de sistemas de combate alcance los USD 49,89 mil millones para 2029 desde los USD 22,30 mil millones en 2020, con una CAGR del 10,69 % entre 2022 y 2029.

La integración de sistemas de combate (CSI) es el proceso de integrar varios sistemas y subsistemas de combate en un único sistema capaz de coordinar y controlar todos los aspectos de una operación de combate. El objetivo de la CSI es proporcionar un sistema de combate unificado e integrado que sea capaz de ofrecer la capacidad de combate requerida.

El proceso de integración implica el diseño y desarrollo de interfaces entre diferentes sistemas, la integración de varios sistemas, la prueba del sistema integrado y la validación de su rendimiento. El proceso se puede dividir en varias fases, entre las que se incluyen el diseño del sistema, la integración del sistema, la prueba del sistema y la validación del sistema.

| ATRIBUTO | DETALLES |

| Periodo de estudio | 2020-2029 |

| Año base | 2021 |

| Año estimado | 2022 |

| Año pronosticado | 2022-2029 |

| Periodo histórico | 2018-2020 |

| Unidad | Valor (miles de millones de USD) |

| Segmentación | Por tipo de plataforma, por aplicación, por región. |

| Por tipo de plataforma |

|

| Por aplicación |

|

| Por región |

|

La fase de diseño del sistema implica la definición de los requisitos del sistema y el desarrollo de la arquitectura del mismo. La fase de integración del sistema implica la integración de los subsistemas individuales en un único sistema. La fase de prueba del sistema implica la prueba del sistema integrado para garantizar que cumple con los requisitos. La fase de validación del sistema implica la evaluación del rendimiento del sistema en un entorno de combate simulado o real.

El mercado está impulsado por la creciente demanda de sistemas de combate avanzados que puedan abordar las amenazas en constante evolución a las que se enfrentan las fuerzas militares de todo el mundo. La necesidad de sistemas integrados que puedan funcionar sin problemas y proporcionar conocimiento de la situación en tiempo real es cada vez más importante en la guerra moderna. Como resultado, los gobiernos y las organizaciones de defensa están invirtiendo mucho en CSI para mejorar sus capacidades de combate.

El mercado de la integración de sistemas de combate (CSI) también está impulsado por avances tecnológicos en áreas como la inteligencia artificial, el aprendizaje automático y la ciberseguridad. Estas tecnologías se están integrando en los sistemas de combate para mejorar su eficacia y resiliencia frente a las amenazas cibernéticas.

El mercado es muy competitivo y varios contratistas de defensa de gran tamaño dominan la industria. Estas empresas tienen una importante experiencia y conocimientos en el diseño y desarrollo de sistemas y subsistemas de combate avanzados y suelen trabajar en estrecha colaboración con agencias gubernamentales y fuerzas militares.

En general, se espera que el mercado de CSI siga creciendo en los próximos años, impulsado por la creciente demanda de sistemas de combate avanzados que puedan proporcionar capacidades de combate superiores en escenarios de guerra modernos. Se espera que el mercado esté impulsado por la inversión continua en el desarrollo de tecnología, así como por un enfoque en la interoperabilidad y la integración entre diferentes sistemas y subsistemas.

Además, la creciente demanda de sistemas de combate naval, incluidos los sistemas de radar , los sistemas de sonar y los sistemas de guerra electrónica, también está impulsando el crecimiento del mercado de CSI. Los sistemas de combate naval son fundamentales para garantizar la seguridad marítima y proteger los activos navales, y su integración en un único sistema de combate puede mejorar su eficacia.

La creciente demanda de modernización y actualización de los sistemas de combate existentes es una de las principales oportunidades. Muchas organizaciones de defensa buscan actualizar sus sistemas heredados para mejorar sus capacidades de combate y su resiliencia frente a las amenazas modernas. Esto crea oportunidades significativas para que las empresas de integración de sistemas de combate (CSI) brinden sus servicios y soluciones.

[título id="attachment_18504" align="aligncenter" width="1920"]

Frequently Asked Questions

• What is the worth of global combat system integration market?

The global combat system integration market is projected to reach USD 49.89 billion by 2029 from USD 22.30 billion in 2020, at a CAGR of 10.69 % from 2022 to 2029.

• What are the key factors driving in the combat system integration market, globally?

Rise in the interconnected warfare systems, focus on defense budgets by various countries, and continuous upgradation in the existing combat systems.

• What is the CAGR of combat system integration market?

The global combat system integration market registered a CAGR of 10.69 % from 2022 to 2029.

• Which are the top companies to hold the market share in combat system integration market?

Key players profiled in the report include ICI Services Corporation, Lockheed Martin Corporation, Leonardo-Finmeccanica, Raytheon Company, Thales Group, Elbit Systems Ltd, DCS Corporation, Qinetiq Group, Saab AB and BAE Systems, Raytheon Company.

• Which is the largest regional market for combat system integration market?

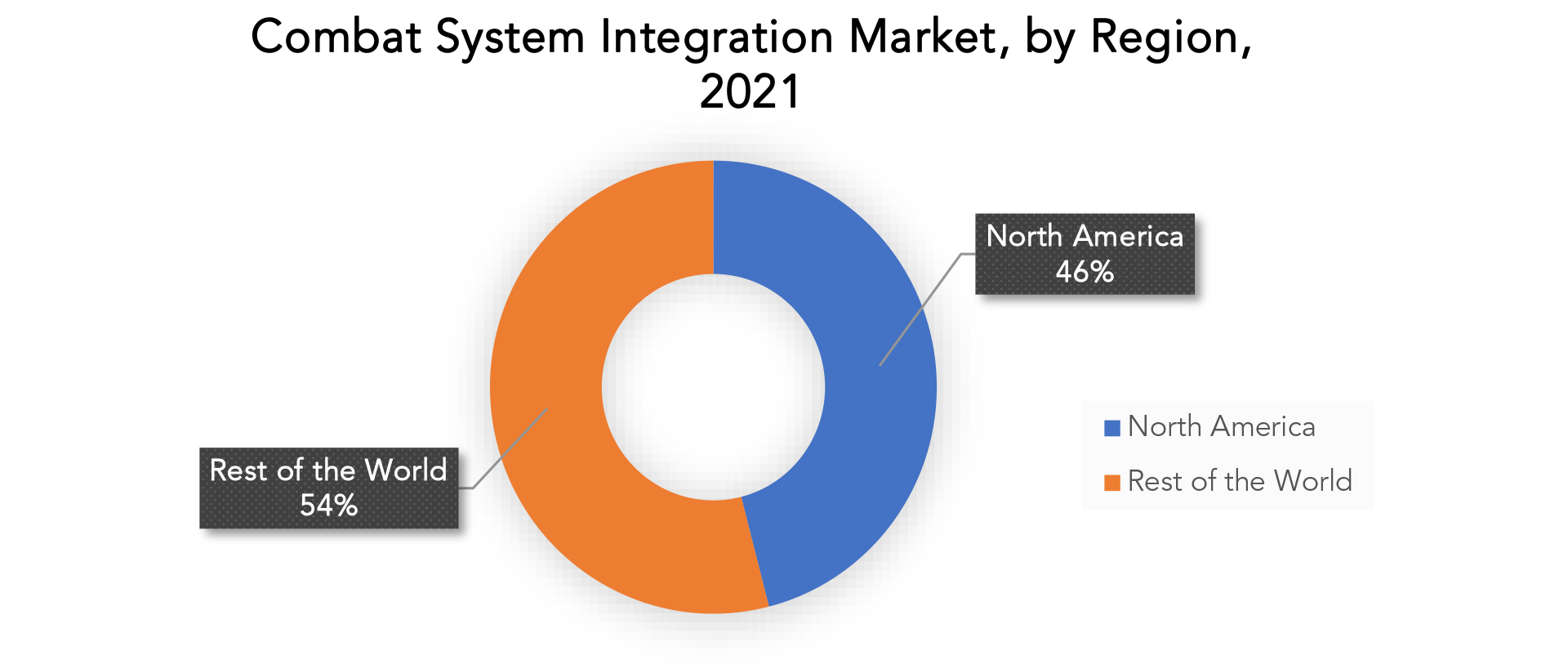

North America is a significant market for combat system integration, with the United States being the region's largest market. The presence of major defence contractors and significant defence spending by the US government drive the region. The growing emphasis on network-centric warfare and the integration of multiple platforms into a single network is also driving demand for combat system integration solutions.

Combat System Integration Market Segment Analysis

The global combat system integration market is segmented by platform application and region.

Based on the platform, global combat system integration market is categorized into large combat ships, medium combat ships, helicopters, small combat ships, submarines, fighter aircraft armored vehicles/artillery and Combat Helicopters. The submarines segment is also expected to witness significant growth in the coming years, driven by the increasing use of advanced submarines by navies around the world. Submarines require advanced combat systems that can operate seamlessly in the underwater environment, and companies that specialize in CSI are expected to play a key role in developing and integrating these systems.

The large combat ships segment also is expected to dominate the Combat System Integration market during the forecast period. This is due to the increasing demand for advanced combat systems for large naval vessels, such as aircraft carriers, destroyers, and frigates, which require sophisticated CSI capabilities.

The other segments, including medium combat ships, small combat ships, helicopters, fighter aircraft, and armored vehicles/artillery, are also expected to witness growth in the coming years, driven by the increasing demand for advanced combat systems across various platforms. However, the extent of their growth may vary based on several factors, including the specific requirements of defense organizations and the evolving threat landscape.

Based on application, the global combat system integration market is categorized into naval, airborne, and land-based. The naval application segment is expected to dominate the Combat System Integration market during the forecast period. This is due to the increasing demand for advanced combat systems for naval platforms, including large combat ships, submarines, and small combat vessels, which require sophisticated CSI capabilities to operate effectively and protect naval assets.

Moreover, the airborne application segment is also expected to witness significant growth in the coming years, driven by the increasing use of unmanned aerial vehicles (UAVs) and manned aircraft for surveillance, reconnaissance, and combat missions. These platforms require advanced CSI capabilities to operate effectively and provide real-time situational awareness to operators. The land-based application segment, which includes armored vehicles and artillery systems, is also expected to witness growth in the coming years, driven by the increasing demand for advanced combat systems for ground forces. These systems can enhance the situational awareness and firepower of ground forces, improving their effectiveness in modern warfare.

[caption id="attachment_18509" align="aligncenter" width="1920"]

Combat System Integration Market Players

The global combat system integration market key players include ICI Services Corporation, Lockheed Martin Corporation, Leonardo-Finmeccanica, Raytheon Company, Thales Group, Elbit Systems Ltd, DCS Corporation, Qinetiq Group, Saab AB and BAE Systems, Raytheon Company. Recent News- Feb. 13, 2023: The Lockheed Martin VISTA X-62A, a one-of-a-kind training aircraft, was recently flown for more than 17 hours by an artificial intelligence agent, marking the first time AI was used on a tactical aircraft. VISTA, which stands for Variable In-flight Simulation Test Aircraft, is revolutionizing air power at the United States Air Force Test Pilot School (USAF TPS) at Edwards Air Force Base in California.

- 02 November 2022: Leonardo is attending the Indo Defense Expo & Forum 2022, Southeast Asia's largest defence and security event. the company would present multi-domain technologies designed to meet the needs of governments and armed forces, as well as strengthen its position as a trusted partner of the Indonesian government and defence industry.

- 28 Feb 2023: BAE Systems, Inc. has been awarded a $219 million (GBP181 million) contract to outfit five Mk 45 Maritime Indirect Fire Systems for the Royal Navy's Type 26 frigates (MIFS). The 5-inch, 62-caliber Mk 45 Mod 4A naval gun system is combined with a fully automated Ammunition Handling System (AHS).

Who Should Buy? Or Key stakeholders

- Regional agencies and research organizations

- Investment research firm

- Original Equipment Manufacturers (OEMs)

- Component Suppliers

- Militaries

- Integration Service Providers

- Research institutes

Combat System Integration Market Regional Analysis

The combat system integration market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).- North America: includes the US, Canada, Mexico

- Asia Pacific: includes China, Japan, South Korea, India, Australia, ASEAN and Rest of APAC

- Europe: includes UK, Germany, France, Italy, Spain, Russia, and Rest of Europe

- South America: includes Brazil, Argentina and Rest of South America

- Middle East & Africa: includes Turkey, UAE, Saudi Arabia, South Africa, and Rest of MEA

North America and Europe are major markets for combat system integration, driven by the presence of major defense contractors and significant defense spending. North America is a major market for combat system integration, with the United States being the largest market in the region. The region is driven by the presence of major defense contractors and significant defense spending by the US government. The demand for combat system integration solutions is also driven by the increasing focus on network-centric warfare and the integration of multiple platforms into a single network.

Asia Pacific is a rapidly growing market for combat system integration, driven by increasing defense spending in countries such as China and India. The region is also characterized by a growing demand for advanced military platforms and the need to modernize existing platforms.

Europe is another significant market for combat system integration, driven by the presence of major defense contractors such as Airbus, BAE Systems, and Thales Group. The region is also characterized by significant defense spending, particularly in countries such as the UK, France, and Germany. The market is driven by the need to modernize existing military platforms and the increasing emphasis on network-centric warfare.

[caption id="attachment_18515" align="aligncenter" width="1920"]

Key Market Segments: Combat System Integration Market

Combat System Integration Market by Platform Type, 2020-2029, (USD Billion)- Large Combat Ships

- Medium Combat Ships

- Small Combat Ships

- Submarines

- Fighter Aircraft

- Helicopters

- Armored Vehicles

- Combat Helicopters

- Naval

- Airborne

- Land-Based

- North America

- Europe

- Asia Pacific

- South America

- Middle East And Africa

Exactitude Consultancy Services Key Objectives

- Increasing sales and market share

- Developing new technology

- Improving profitability

- Entering new markets

- Enhancing brand reputation

Key Question Answered

- What is the expected growth rate of the combat system integration market over the next 7 years?

- Who are the major players in the combat system integration market and what is their market share?

- What are the end-user industries driving demand for market and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-Pacific, Middle East, and Africa?

- How is the economic environment affecting the combat system integration market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the combat system integration market?

- What is the current and forecasted size and growth rate of the global combat system integration market?

- What are the key drivers of growth in the combat system integration market?

- What are the distribution channels and supply chain dynamics in the combat system integration market?

- What are the technological advancements and innovations in the combat system integration market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the combat system integration market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the combat system integration market?

- What are the service offerings and specifications of leading players in the market?

- INTRODUCCIÓN

- DEFINICIÓN DE MERCADO

- SEGMENTACIÓN DEL MERCADO

- CRONOGRAMAS DE INVESTIGACIÓN

- SUPUESTOS Y LIMITACIONES

- METODOLOGÍA DE LA INVESTIGACIÓN

- MINERÍA DE DATOS

- INVESTIGACIÓN SECUNDARIA

- INVESTIGACIÓN PRIMARIA

- ASESORAMIENTO DE EXPERTOS EN LA MATERIA

- CONTROLES DE CALIDAD

- REVISIÓN FINAL

- TRIANGULACIÓN DE DATOS

- ENFOQUE DE ABAJO HACIA ARRIBA

- ENFOQUE DE ARRIBA HACIA ABAJO

- FLUJO DE INVESTIGACIÓN

- FUENTES DE DATOS

- MINERÍA DE DATOS

- RESUMEN EJECUTIVO

- PANORAMA DEL MERCADO

- PERSPECTIVAS DEL MERCADO DE INTEGRACIÓN DE SISTEMAS DE COMBATE GLOBAL

- IMPULSORES DEL MERCADO

- RESTRICCIONES DEL MERCADO

- OPORTUNIDADES DE MERCADO

- IMPACTO DEL COVID-19 EN EL MERCADO DE INTEGRACIÓN DE SISTEMAS DE COMBATE

- MODELO DE LAS CINCO FUERZAS DE PORTER

- AMENAZA DE NUEVOS INGRESANTES

- AMENAZA DE SUSTITUTOS

- PODER DE NEGOCIACIÓN DE LOS PROVEEDORES

- PODER DE NEGOCIACIÓN DE LOS CLIENTES

- GRADO DE COMPETENCIA

- ANÁLISIS DE LA CADENA DE VALOR DE LA INDUSTRIA

- PERSPECTIVAS DEL MERCADO DE INTEGRACIÓN DE SISTEMAS DE COMBATE GLOBAL

- MERCADO GLOBAL DE INTEGRACIÓN DE SISTEMAS DE COMBATE POR TIPO DE PLATAFORMA, 2020-2029 (MIL MILLONES DE USD)

- GRANDES BUQUES DE COMBATE

- BUQUES DE COMBATE MEDIANOS

- PEQUEÑOS BUQUES DE COMBATE

- SUBMARINOS

- Aviones de combate

- HELICÓPTEROS

- VEHÍCULOS BLINDADOS

- HELICÓPTEROS DE COMBATE

- MERCADO GLOBAL DE INTEGRACIÓN DE SISTEMAS DE COMBATE POR APLICACIÓN, 2020-2029 (MIL MILLONES DE USD)

- NAVAL

- AEROTRANSPORTADO

- BASADO EN TIERRA

- MERCADO GLOBAL DE INTEGRACIÓN DE SISTEMAS DE COMBATE POR REGIÓN, 2020-2029 (MIL MILLONES DE USD)

- AMÉRICA DEL NORTE

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- AMÉRICA DEL NORTE

- COMPANY PROFILES* (BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCT OFFERED, RECENT DEVELOPMENTS)

8.1. ICI SERVICES CORPORATION

8.2. LOCKHEED MARTIN CORPORATION

8.3. LEONARDO-FINMECCANICA

8.4. RAYTHEON COMPANY

8.5. THALES GROUP

8.6. ELBIT SYSTEMS LTD

8.7. DCS CORPORATION

8.8. QINETIQ GROUP

8.9. SAAB AB

8.10. BAE SYSTEMS *THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 2 GLOBAL COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 3 GLOBAL COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 4 NORTH AMERICA COMBAT SYSTEM INTEGRATION MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 5 NORTH AMERICA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 6 NORTH AMERICA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 7 US COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 8 US COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 9 US COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 10 CANADA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 11 CANADA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 12 CANADA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 13 MEXICO COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 14 MEXICO COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 15 MEXICO COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 16 SOUTH AMERICA COMBAT SYSTEM INTEGRATION MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 17 SOUTH AMERICA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 18 SOUTH AMERICA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 19 BRAZIL COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 20 BRAZIL COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 21 BRAZIL COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 22 ARGENTINA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 23 ARGENTINA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 24 ARGENTINA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 25 COLOMBIA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 26 COLOMBIA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 27 COLOMBIA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 28 REST OF SOUTH AMERICA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 29 REST OF SOUTH AMERICA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 30 REST OF SOUTH AMERICA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 31 ASIA-PACIFIC COMBAT SYSTEM INTEGRATION MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 32 ASIA-PACIFIC COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 33 ASIA-PACIFIC COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 34 INDIA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 35 INDIA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 36 INDIA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 37 CHINA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 38 CHINA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 39 CHINA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 40 JAPAN COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 41 JAPAN COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 42 JAPAN COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 43 SOUTH KOREA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 44 SOUTH KOREA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 45 SOUTH KOREA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 46 AUSTRALIA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 47 AUSTRALIA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 48 AUSTRALIA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 49 SOUTH-EAST ASIA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 50 SOUTH-EAST ASIA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 51 SOUTH-EAST ASIA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 52 REST OF ASIA PACIFIC COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 53 REST OF ASIA PACIFIC COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 54 REST OF ASIA PACIFIC COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 55 EUROPE COMBAT SYSTEM INTEGRATION MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 56 EUROPE COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 57 EUROPE COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 58 GERMANY COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 59 GERMANY COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 60 GERMANY COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 61 UK COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 62 UK COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 63 UK COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 64 FRANCE COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 65 FRANCE COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 66 FRANCE COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 67 ITALY COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 68 ITALY COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 69 ITALY COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 70 SPAIN COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 71 SPAIN COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 72 SPAIN COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 73 RUSSIA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 74 RUSSIA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 75 RUSSIA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 76 REST OF EUROPE COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 77 REST OF EUROPE COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 78 REST OF EUROPE COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 79 MIDDLE EAST AND AFRICA COMBAT SYSTEM INTEGRATION MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 80 MIDDLE EAST AND AFRICA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 81 MIDDLE EAST AND AFRICA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 82 UAE COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 83 UAE COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 84 UAE COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 85 SAUDI ARABIA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 86 SAUDI ARABIA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 87 SAUDI ARABIA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 88 SOUTH AFRICA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 89 SOUTH AFRICA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 90 SOUTH AFRICA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

TABLE 91 REST OF MIDDLE EAST AND AFRICA COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

TABLE 92 REST OF MIDDLE EAST AND AFRICA COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 93 REST OF MIDDLE EAST AND AFRICA COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2020-2029

FIGURE 9 GLOBAL COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2020- 2029

FIGURE 10 GLOBAL COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2020-2029

FIGURE 11 PORTER’S FIVE FORCES MODEL

FIGURE 12 GLOBAL COMBAT SYSTEM INTEGRATION MARKET BY PLATFORM TYPE (USD BILLION) 2021

FIGURE 13 GLOBAL COMBAT SYSTEM INTEGRATION MARKET BY APPLICATION (USD BILLION) 2021

FIGURE 14 GLOBAL COMBAT SYSTEM INTEGRATION MARKET BY REGION (USD BILLION) 2021

FIGURE 15 NORTH AMERICA COMBAT SYSTEM INTEGRATION MARKET SNAPSHOT

FIGURE 16 EUROPE COMBAT SYSTEM INTEGRATION MARKET SNAPSHOT

FIGURE 17 SOUTH AMERICA COMBAT SYSTEM INTEGRATION MARKET SNAPSHOT

FIGURE 18 ASIA PACIFIC COMBAT SYSTEM INTEGRATION MARKET SNAPSHOT

FIGURE 19 MIDDLE EAST ASIA AND AFRICA COMBAT SYSTEM INTEGRATION MARKET SNAPSHOT

FIGURE 20 MARKET SHARE ANALYSIS

FIGURE 21 ICI SERVICES CORPORATION: COMPANY SNAPSHOT

FIGURE 22 LOCKHEED MARTIN CORPORATION: COMPANY SNAPSHOT

FIGURE 23 LEONARDO-FINMECCANICA: COMPANY SNAPSHOT

FIGURE 24 RAYTHEON COMPANY: COMPANY SNAPSHOT

FIGURE 25 THALES GROUP: COMPANY SNAPSHOT

FIGURE 26 ELBIT SYSTEMS LTD: COMPANY SNAPSHOT

FIGURE 27 DCS CORPORATION: COMPANY SNAPSHOT

FIGURE 28 QINETIQ GROUP: COMPANY SNAPSHOT

FIGURE 29 SAAB AB: COMPANY SNAPSHOT

FIGURE 30 BAE SYSTEMS: COMPANY SNAPSHOT

DOWNLOAD FREE SAMPLE REPORT

License Type

SPEAK WITH OUR ANALYST

Want to know more about the report or any specific requirement?

WANT TO CUSTOMIZE THE REPORT?

Our Clients Speak

We asked them to research ‘ Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te

Yosuke Mitsui

Senior Associate Construction Equipment Sales & Marketing

We asked them to research ‘Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te