Base Year Value ()

x.x %

x.x %

CAGR ()

x.x %

x.x %

Forecast Year Value ()

x.x %

x.x %

Historical Data Period

Largest Region

Forecast Period

Mercado de poliolefinas por tipo (polietileno (PE), polipropileno (PP), elastómero de poliolefina (POE), poliestireno, etileno acetato de vinilo (EVA), poliolefina termoplástica (TPO)), aplicación (película y lámina, moldeo por inyección, moldeo por soplado, extrusión de perfiles, otros) y por región Tendencias globales y pronóstico de 2022 a 2029

Instant access to hundreds of data points and trends

- Market estimates from 2014-2029

- Competitive analysis, industry segmentation, financial benchmarks

- Incorporates SWOT, Porter's Five Forces and risk management frameworks

- PDF report or online database with Word, Excel and PowerPoint export options

- 100% money back guarantee

Descripción general del mercado de poliolefinas

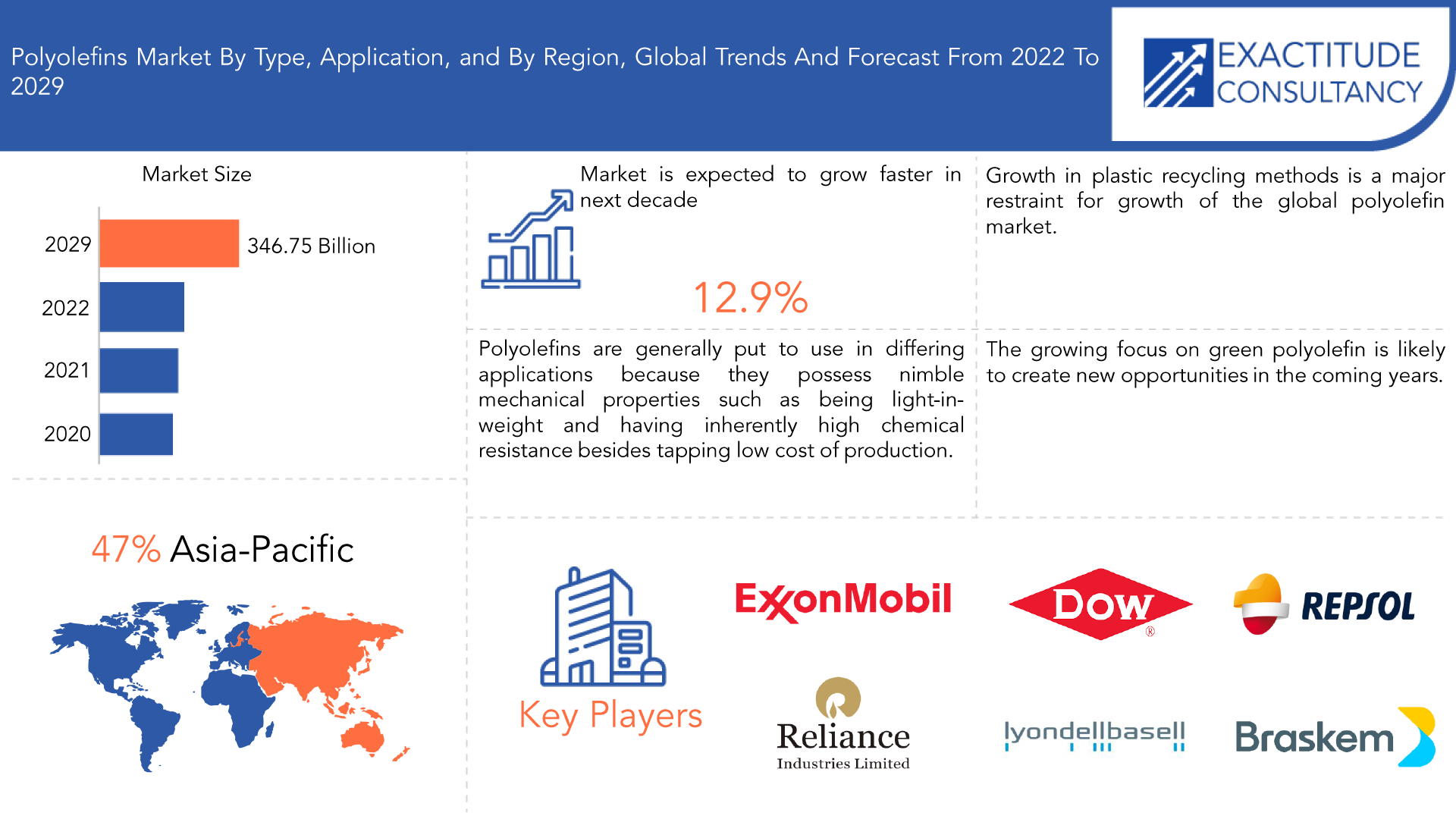

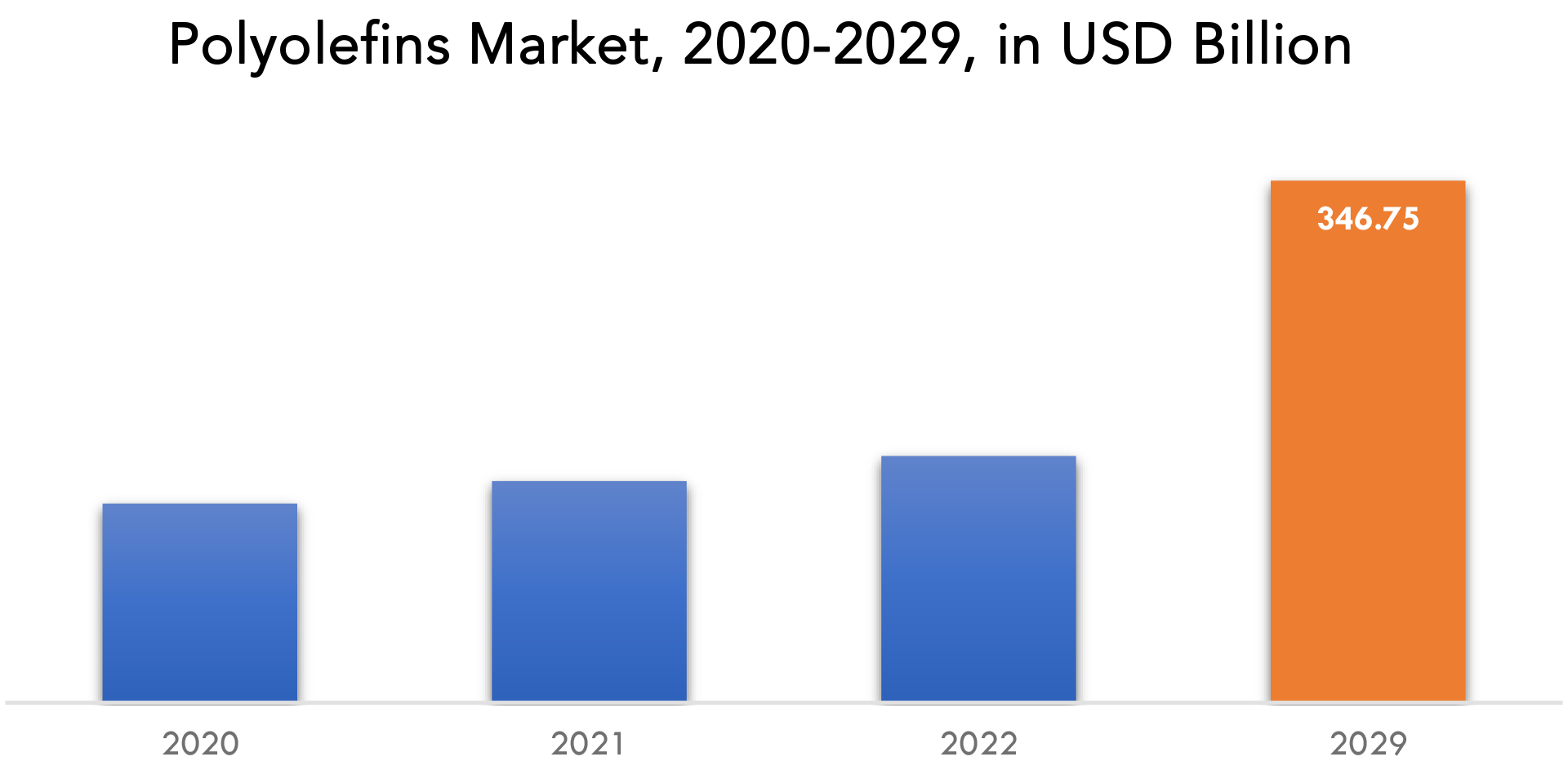

Se proyecta que el mercado mundial de poliolefinas alcance los 346,75 mil millones de dólares en 2029, desde los 132,30 mil millones de dólares en 2020, con una CAGR del 12,9 % entre 2022 y 2029.

La poliolefina es cualquier resina sintética que se obtiene mediante la polimerización de olefinas. Las olefinas son hidrocarburos con átomos de carbono unidos entre sí por un doble enlace. La mayoría de ellas se derivan del gas natural o de componentes de petróleo de bajo peso molecular, y sus componentes más conocidos son el etileno y el propileno. Estos dos compuestos son olefinas inferiores, que tienen solo un par de átomos de carbono en sus moléculas. El buteno y el metilpentano son ejemplos de olefinas superiores, que tienen dos o más átomos de carbono por molécula. Los polímeros se fabrican a partir de estas olefinas, de las cuales las más importantes son el polietileno y el polipropileno .

La gran variedad de aplicaciones para las que se pueden utilizar estos plásticos adaptables y las enormes cantidades en las que se producen superan con creces a las de otros polímeros olefínicos, por lo que a menudo se utiliza la palabra "poliolefina" para referirse exclusivamente a ellos. Los filmes retráctiles, los embalajes, los materiales de fabricación, las fibras para uso en ropa y otros tejidos, la tecnología de espuma rígida, las cuerdas de las raquetas de tenis, las botellas y los contenedores están hechos de poliolefinas. También se utilizan en tubos termorretráctiles para proteger cables y nuevos componentes electrónicos, así como en aplicaciones médicas.

| ATRIBUTO | DETALLES |

| Periodo de estudio | 2020-2029 |

| Año base | 2021 |

| Año estimado | 2022 |

| Año pronosticado | 2022-2029 |

| Periodo histórico | 2018-2020 |

| Unidad | Valor (miles de millones de USD) Volumen (kilotones) |

| Segmentación | Por tipo, por aplicación, por región. |

| Por tipo |

|

| Por aplicación |

|

| Por región |

|

La creciente demanda de poliolefinas en las industrias automotriz, eléctrica y electrónica, de alimentos y bebidas y de bienes de consumo está impulsando el mercado hacia adelante. La alta rigidez, la buena resistencia a la humedad y a los productos químicos son algunas de las propiedades que hacen que las poliolefinas sean adecuadas para aplicaciones industriales, principalmente para el envasado de repuestos automotrices y eléctricos. Mientras que en la industria automotriz, los fabricantes se están enfocando en aumentar la eficiencia del vehículo al reducir el peso del mismo. Las poliolefinas son preferidas debido a sus propiedades de peso ligero, fácil procesamiento, sellado y rigidez.

La necesidad de más materiales de envasado para alimentos y bebidas está impulsando el uso del polietileno en el sector de alimentos y bebidas. Por sus cualidades de resistencia a las tensiones físicas, durabilidad, flexibilidad en el envasado y facilidad de moldeo de los productos, también se utiliza en moda, deportes y juguetes. Las regulaciones gubernamentales y los desastres ambientales afectan a los plásticos fabricados con poliolefinas. Ahora suponen una grave amenaza para el ecosistema. La descomposición requiere mucho tiempo. Además, se acumula en los cuerpos de agua, dañando tanto el medio ambiente humano como el acuático.

La industria de la construcción es otro gran consumidor de poliolefinas, principalmente en forma de tuberías, cables y materiales de aislamiento. Se espera que el crecimiento de la industria de la construcción, en particular en las economías emergentes, impulse la demanda de poliolefinas en los próximos años. La industria automotriz también es un consumidor importante de poliolefinas, principalmente en forma de piezas interiores y exteriores. La demanda de vehículos livianos y de bajo consumo de combustible está impulsando el uso de poliolefinas en la industria automotriz.

Además, los gobiernos de numerosos países han aprobado leyes específicas para controlar el uso del plástico en sus países, lo que impide la expansión del mercado mundial de poliolefinas. El potencial de crecimiento del mercado está aumentando como resultado de los avances en la tecnología y el desarrollo de productos en numerosos sectores. El desarrollo del mercado mundial de poliolefinas se acelerará aún más pronto gracias a la expansión de los plásticos biodegradables y de origen biológico.

[título id="attachment_18907" align="aligncenter" width="1920"]

Frequently Asked Questions

• What is the worth of global polyolefins market?

The global polyolefins market is projected to reach USD 346.75 billion by 2029 from USD 132.30 billion in 2020, at a CAGR of 12.9 % from 2022 to 2029.

• What are the factor driving the growth of polyolefins market?

The driving factors of the polyolefin market are growing demand from automotive industry for making lightweight vehicles and increasing demand for films and sheets from the agriculture sector.

• What is the CAGR of polyolefins market?

The global polyolefins market registered a CAGR of 12.9 % from 2022 to 2029

• Which are the top companies to hold the market share in polyolefins market?

Key players profiled in the report include ExxonMobil Corporation, SABIC, Dow, Repsol, Ineos Group AG, Reliance Industries, LyondellBasell Industries N.V., Sinopec Group, Ducor Petrochemical, BASF SE, Borealis AG, Arkema S.A., Braskem S.A, Abu Dhabi Polymers Company Ltd. (Borouge), Sasol Ltd, Tosoh Corporation, Polyone Corporation, and others

• Which is the largest regional market for Polyolefins market?

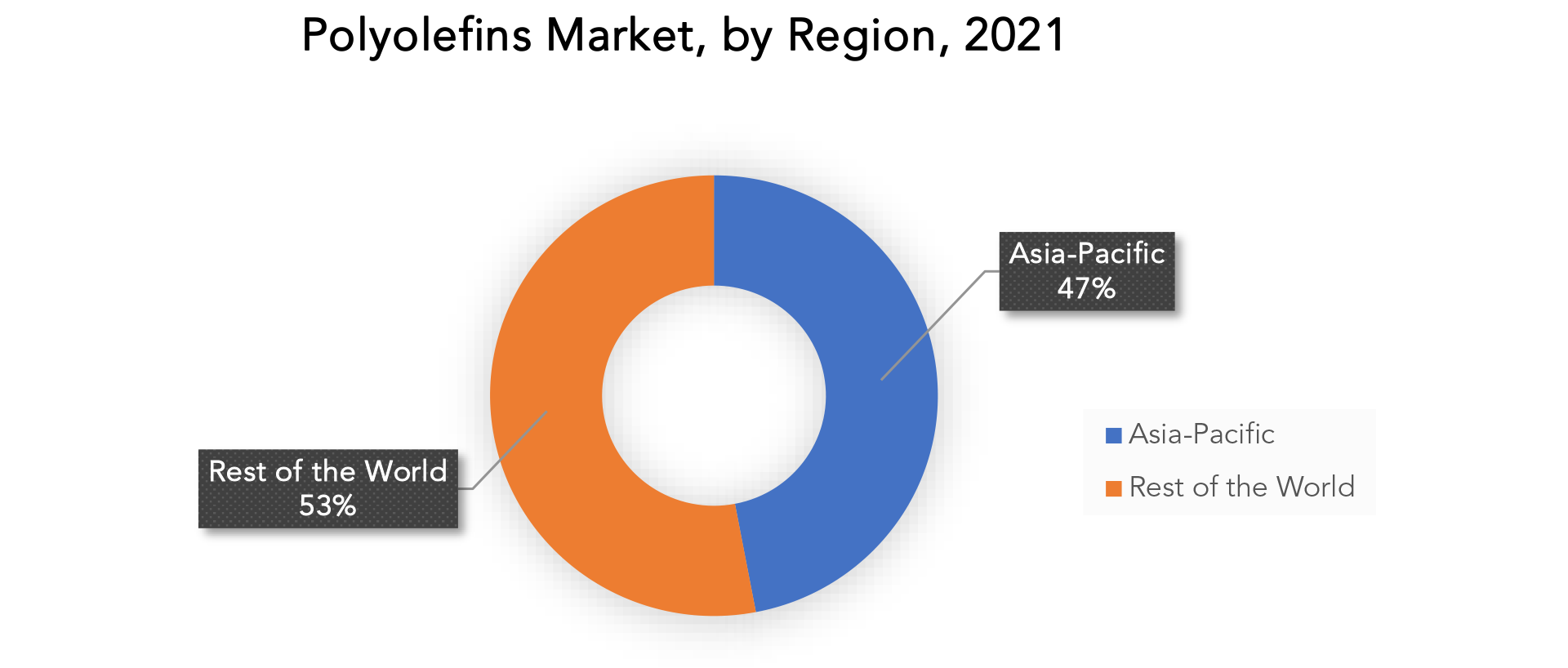

Asia Pacific dominated the polyolefin market, accounting for 47% of total revenue in 2021. Asia Pacific is the largest and fastest-growing polyolefin market. The rapid industrialization of economies such as China, India, and Indonesia is increasing polyolefin consumption in the region.

Polyolefins Market Segment Analysis

The global polyolefins market is segmented by type, application, and region.Based on type, the polyolefins market is classified into polyethylene (PE), polypropylene (PP), polyolefin elastomer (POE), polystyrene, ethylene vinyl acetate (EVA), thermoplastics polyolefin (TPO) the polyethylene sector dominates the market with a CAGR of 12.3%, it is anticipated to achieve an expected value of USD 333.303 billion by 2029. Due to the rapid growth of the food industry in developing countries like China and India and the development of the renewable energy sector, polyethylene is getting significant traction on the global market. This is attributable to the widespread use of polyethylene in food containers.

The polypropylene market is the fastest growing. It is expected to be worth USD 225.3 billion by 2030, with a CAGR of 14%. The growing demand for syringes, medical vials, and specimen bottles is driving up demand for polypropylene. The polystyrene market is the third largest. It is expected to be worth USD 9.625 billion by 2029, with a CAGR of 11.3%. High adoption in insulation applications and increased adoption in automotive applications are important parameters for the growth of the polystyrene market.

Based on application, the market is segmented into film & sheet, injection molding, blow molding, profile extrusion, others. The film and sheet segment dominated the market. It is expected to reach USD 198.175 billion by 2029, at a CAGR of 13%. The primary driver of market expansion is an increase in demand for biaxially oriented polyolefin films. However, one factor impeding demand for polyolefin films and sheets is the implementation of stringent regulations prohibiting the use of non-biodegradable plastics.

Injection molding is the fastest-growing segment. Fast manufacturing, high efficiency in terms of the number of parts manufactured per hour, low labor costs, design flexibility, high-output production, enhanced strength of plastic products, and product consistency are some of the factors driving demand for polyolefin in injection molding. Labor costs have decreased as automation in the injection molding process has increased. The third-largest market is for profile extrusion. It is expected to be worth USD 92.50 million by 2029, with a CAGR of 11.3%.

[caption id="attachment_18916" align="aligncenter" width="1920"]

Polyolefins Market Players

The global polyolefins market key players include ExxonMobil Corporation, SABIC, Dow, Repsol, Ineos Group AG, Reliance Industries, LyondellBasell Industries N.V., Sinopec Group, Ducor Petrochemical, BASF SE, Borealis AG, Arkema S.A., Braskem S.A, Abu Dhabi Polymers Company Ltd. (Borouge), Sasol Ltd, Tosoh Corporation, Polyone Corporation, and others 23 Aug 2022: SABIC, a global leader in the chemicals industry, announced that its SABIC SK Nexlene Company (SSNC) joint venture in South Korea with SK Geo Centric (formerly SK Global Chemicals) will expand the capacity of their Ulsan plant to produce advanced material solutions based on NEXLENE technology. Korea Nexlene Company (KNC) operates the plant, which supports the production of SABIC's diverse portfolio of COHERETM metallocene polyolefin plastomers (POP), SUPEERTM metallocene linear low density polyethylenes (mLLDPE), and FORTIFYTM polyolefin elastomers (POE). November 02, 2022: LyondellBasell announced that Stavian Quang Yen Petrochemical, Ltd. (Stavian) has chosen its leading polypropylene (PP) technology for a new world scale production facility.Who Should Buy? Or Key stakeholders

- Regional agencies and research organizations

- Investment research firm

- Manufacturers of Polyolefins

- Traders, distributors, and suppliers of Polyolefins

- Organizations, forums, and alliances related to Polyolefins distribution

- Government and regional agencies and research organizations

- Research institutes

- Automotive Industry

Polyolefins Market Regional Analysis

The polyolefins market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).

- North America: includes the US, Canada, Mexico

- Asia Pacific: includes China, Japan, South Korea, India, Australia, ASEAN, and Rest of APAC

- Europe: includes UK, Germany, France, Italy, Spain, Russia, and Rest of Europe

- South America: includes Brazil, Argentina, and Rest of South America

- Middle East & Africa: includes Turkey, UAE, Saudi Arabia, South Africa, and Rest of MEA

The Asia-Pacific region dominated the market. It is expected to reach USD 47.165 billion by 2029, with a CAGR of 12.9%. This is attributed to countries such as China, India, and Japan, which have established and developed consumer bases in the electronics manufacturing and construction sectors. The outbreak of COVID-19 in China severely hampered the polyolefins market, as China is a major consumer of polyolefins. This is attributed to industries such as packaging, toy manufacturing, construction, and automotive.

Europe is the world's second-largest continent. It is expected to be worth USD 7580 million by 2030, with a CAGR of 7%. Germany, France, the United Kingdom, Italy, Spain, and the rest of Europe are all examined. As of the expansion of the packaging and automotive industries, Germany is one of the most significant users of polyolefins. The COVID-19 pandemic has caused lockdowns in several European countries, resulting in panic purchases of consumer goods such as food, health, and hygiene products. This fueled demand for polyolefins in the packaging industry.

North America is the third most populous continent. It is expected to be worth USD 8085 million by 2030, with a CAGR of 12%. Plastic is primarily used in the packaging, construction, automotive, and electrical and electronics industries in North America, which serves as the market's primary driving force. Furthermore, as the COVID-19 pandemic spread, the demand for packaging increased due to the increased penetration of e-commerce frameworks.

[caption id="attachment_18918" align="aligncenter" width="1920"]

Key Market Segments: Polyolefins Market

Polyolefins Market By Type, 2020-2029, (Usd Billion) (Kilotons)- Polyethylene (Pe)

- Polypropylene (Pp)

- Polyolefin Elastomer (Poe)

- Ethylene Vinyl Acetate (Eva)

- Thermoplastics Polyolefin (Tpo)

- Polystyrene

- Film & Sheet

- Injection Molding

- Blow Molding

- Profile Extrusion

- Others

- North America

- Europe

- Asia Pacific

- South America

- Middle East And Africa

Exactitude Consultancy Services Key Objectives

- Increasing sales and market share

- Developing new technology

- Improving profitability

- Entering new markets

- Enhancing brand reputation

Key Question Answered

- What is the expected growth rate of the polyolefins market over the next 7 years?

- Who are the major players in the polyolefins market and what is their market share?

- What are the end-user industries driving demand for market and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-Pacific, Middle East, and Africa?

- How is the economic environment affecting the polyolefins market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the polyolefins market?

- What is the current and forecasted size and growth rate of the global polyolefins market?

- What are the key drivers of growth in the polyolefins market?

- What are the distribution channels and supply chain dynamics in the polyolefins market?

- What are the technological advancements and innovations in the polyolefins market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the polyolefins market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the polyolefins market?

- What are the product offerings and specifications of leading players in the market?

- What is the pricing trend of polyolefins in the market and what is the impact of raw material prices on the price trend?

- INTRODUCCIÓN

- DEFINICIÓN DE MERCADO

- SEGMENTACIÓN DEL MERCADO

- CRONOGRAMAS DE INVESTIGACIÓN

- SUPUESTOS Y LIMITACIONES

- METODOLOGÍA DE LA INVESTIGACIÓN

- MINERÍA DE DATOS

- INVESTIGACIÓN SECUNDARIA

- INVESTIGACIÓN PRIMARIA

- ASESORAMIENTO DE EXPERTOS EN LA MATERIA

- CONTROLES DE CALIDAD

- REVISIÓN FINAL

- TRIANGULACIÓN DE DATOS

- ENFOQUE DE ABAJO HACIA ARRIBA

- ENFOQUE DE ARRIBA HACIA ABAJO

- FLUJO DE INVESTIGACIÓN

- FUENTES DE DATOS

- MINERÍA DE DATOS

- RESUMEN EJECUTIVO

- PANORAMA DEL MERCADO

- PERSPECTIVAS DEL MERCADO MUNDIAL DE POLIOLEFINAS

- IMPULSORES DEL MERCADO

- RESTRICCIONES DEL MERCADO

- OPORTUNIDADES DE MERCADO

- IMPACTO DEL COVID-19 EN EL MERCADO DE POLIOLEFINAS

- MODELO DE LAS CINCO FUERZAS DE PORTER

- AMENAZA DE NUEVOS INGRESANTES

- AMENAZA DE SUSTITUTOS

- PODER DE NEGOCIACIÓN DE LOS PROVEEDORES

- PODER DE NEGOCIACIÓN DE LOS CLIENTES

- GRADO DE COMPETENCIA

- ANÁLISIS DE LA CADENA DE VALOR DE LA INDUSTRIA

- PERSPECTIVAS DEL MERCADO MUNDIAL DE POLIOLEFINAS

- GLOBAL POLYOLEFINS MARKET BY TYPE, 2020-2029, (USD BILLION) (KILOTONS)

- POLYETHYLENE (PE)

- POLYPROPYLENE (PP)

- POLYOLEFIN ELASTOMER (POE)

- ETHYLENE VINYL ACETATE (EVA)

- THERMOPLASTICS POLYOLEFIN (TPO)

- POLYSTYRENE

- GLOBAL POLYOLEFINS MARKET BY APPLICATION, 2020-2029, (USD BILLION) (KILOTONS)

- FILM & SHEET

- INJECTION MOLDING

- BLOW MOLDING

- PROFILE EXTRUSION

- OTHERS

- GLOBAL POLYOLEFINS MARKET BY REGION, 2020-2029, (USD BILLION) (KILOTONS)

- NORTH AMERICA

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

- COMPANY PROFILES* (BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCT OFFERED, RECENT DEVELOPMENTS)

8.1. EXXONMOBIL CORPORATION

8.2. SABIC

8.3. DOW

8.4. REPSOL

8.5. INEOS GROUP AG

8.6. RELIANCE INDUSTRIES

8.7. LYONDELLBASELL INDUSTRIES N.V.

8.8. SINOPEC GROUP

8.9. DUCOR PETROCHEMICAL

8.10. BASF SE

8.11. BOREALIS AG

8.12. ARKEMA S.A.

8.13. BRASKEM S.A

8.14. ABU DHABI POLYMERS COMPANY LTD. (BOROUGE)

8.15. SASOL LTD

8.16. TOSOH CORPORATION

8.17.POLYONE CORPORATION.*THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 2 GLOBAL POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 3 GLOBAL POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 4 GLOBAL POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 5 GLOBAL POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 6 GLOBAL POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 7 NORTH AMERICA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 8 NORTH AMERICA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 9 NORTH AMERICA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 10 NORTH AMERICA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 11 NORTH AMERICA POLYOLEFINS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 12 NORTH AMERICA POLYOLEFINS MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 13 US POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 14 US POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 15 US POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 16 US POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 17 US POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 18 US POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 19 CANADA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 20 CANADA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 21 CANADA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 22 CANADA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 23 CANADA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 24 CANADA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 25 MEXICO POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 26 MEXICO POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 27 MEXICO POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 28 MEXICO POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 29 MEXICO POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 30 MEXICO POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 31 SOUTH AMERICA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 32 SOUTH AMERICA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 33 SOUTH AMERICA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 34 SOUTH AMERICA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 35 SOUTH AMERICA POLYOLEFINS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 36 SOUTH AMERICA POLYOLEFINS MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 37 BRAZIL POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 38 BRAZIL POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 39 BRAZIL POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 40 BRAZIL POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 41 BRAZIL POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 42 BRAZIL POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 43 ARGENTINA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 44 ARGENTINA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 45 ARGENTINA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 46 ARGENTINA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 47 ARGENTINA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 48 ARGENTINA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 49 COLOMBIA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 50 COLOMBIA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 51 COLOMBIA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 52 COLOMBIA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 53 COLOMBIA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 54 COLOMBIA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 55 REST OF SOUTH AMERICA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 56 REST OF SOUTH AMERICA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 57 REST OF SOUTH AMERICA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 58 REST OF SOUTH AMERICA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 59 REST OF SOUTH AMERICA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 60 REST OF SOUTH AMERICA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 61 ASIA-PACIFIC POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 62 ASIA-PACIFIC POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 63 ASIA-PACIFIC POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 64 ASIA-PACIFIC POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 65 ASIA-PACIFIC POLYOLEFINS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 66 ASIA-PACIFIC POLYOLEFINS MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 67 INDIA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 68 INDIA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 69 INDIA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 70 INDIA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 71 INDIA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 72 INDIA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 73 CHINA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 74 CHINA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 75 CHINA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 76 CHINA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 77 CHINA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 78 CHINA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 79 JAPAN POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 80 JAPAN POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 81 JAPAN POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 82 JAPAN POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 83 JAPAN POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 84 JAPAN POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 85 SOUTH KOREA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 86 SOUTH KOREA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 87 SOUTH KOREA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 88 SOUTH KOREA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 89 SOUTH KOREA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 90 SOUTH KOREA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 91 AUSTRALIA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 92 AUSTRALIA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 93 AUSTRALIA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 94 AUSTRALIA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 95 AUSTRALIA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 96 AUSTRALIA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 97 SOUTH-EAST ASIA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 98 SOUTH-EAST ASIA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 99 SOUTH-EAST ASIA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 100 SOUTH-EAST ASIA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 101 SOUTH-EAST ASIA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 102 SOUTH-EAST ASIA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 103 REST OF ASIA PACIFIC POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 104 REST OF ASIA PACIFIC POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 105 REST OF ASIA PACIFIC POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 106 REST OF ASIA PACIFIC POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 107 REST OF ASIA PACIFIC POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 108 REST OF ASIA PACIFIC POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 109 EUROPE POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 110 EUROPE POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 111 EUROPE POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 112 EUROPE POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 113 EUROPE POLYOLEFINS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 114 EUROPE POLYOLEFINS MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 115 GERMANY POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 116 GERMANY POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 117 GERMANY POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 118 GERMANY POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 119 GERMANY POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 120 GERMANY POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 121 UK POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 122 UK POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 123 UK POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 124 UK POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 125 UK POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 126 UK POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 127 FRANCE POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 128 FRANCE POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 129 FRANCE POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 130 FRANCE POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 131 FRANCE POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 132 FRANCE POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 133 ITALY POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 134 ITALY POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 135 ITALY POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 136 ITALY POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 137 ITALY POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 138 ITALY POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 139 SPAIN POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 140 SPAIN POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 141 SPAIN POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 142 SPAIN POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 143 SPAIN POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 144 SPAIN POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 145 RUSSIA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 146 RUSSIA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 147 RUSSIA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 148 RUSSIA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 149 RUSSIA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 150 RUSSIA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 151 REST OF EUROPE POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 152 REST OF EUROPE POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 153 REST OF EUROPE POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 154 REST OF EUROPE POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 155 REST OF EUROPE POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 156 REST OF EUROPE POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 157 MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 158 MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 159 MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 160 MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 161 MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 162 MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 163 UAE POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 164 UAE POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 165 UAE POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 166 UAE POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 167 UAE POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 168 UAE POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 169 SAUDI ARABIA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 170 SAUDI ARABIA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 171 SAUDI ARABIA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 172 SAUDI ARABIA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 173 SAUDI ARABIA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 174 SAUDI ARABIA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 175 SOUTH AFRICA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 176 SOUTH AFRICA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 177 SOUTH AFRICA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 178 SOUTH AFRICA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 179 SOUTH AFRICA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 180 SOUTH AFRICA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

TABLE 181 REST OF MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 182 REST OF MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY TYPE (KILOTONS) 2020-2029

TABLE 183 REST OF MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 184 REST OF MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY APPLICATION (KILOTONS) 2020-2029

TABLE 185 REST OF MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 186 REST OF MIDDLE EAST AND AFRICA POLYOLEFINS MARKET BY REGION (KILOTONS) 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL POLYOLEFINS MARKET BY TYPE (USD BILLION) 2020-2029

FIGURE 9 GLOBAL POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2020-2029

FIGURE 10 GLOBAL POLYOLEFINS MARKET BY REGION (USD BILLION) 2020-2029

FIGURE 11 PORTER’S FIVE FORCES MODEL

FIGURE 12 GLOBAL POLYOLEFINS MARKET BY TYPE (USD BILLION) 2021

FIGURE 13 GLOBAL POLYOLEFINS MARKET BY APPLICATION (USD BILLION) 2021

FIGURE 14 GLOBAL POLYOLEFINS MARKET BY REGION (USD BILLION) 2021

FIGURE 15 NORTH AMERICA POLYOLEFINS MARKETSNAPSHOT

FIGURE 16 EUROPE POLYOLEFINS MARKETSNAPSHOT

FIGURE 17 SOUTH AMERICA POLYOLEFINS MARKETSNAPSHOT

FIGURE 18 ASIA PACIFICPOLYOLEFINS MARKETSNAPSHOT

FIGURE 19 MIDDLE EAST ASIA AND AFRICA POLYOLEFINS MARKETSNAPSHOT

FIGURE 20 MARKET SHARE ANALYSIS

FIGURE 21 EXXONMOBIL CORPORATION: COMPANY SNAPSHOT

FIGURE 22 SABIC: COMPANY SNAPSHOT

FIGURE 23 DOW: COMPANY SNAPSHOT

FIGURE 24 REPSOL: COMPANY SNAPSHOT

FIGURE 25 INEOS GROUP AG: COMPANY SNAPSHOT

FIGURE 26 RELIANCE INDUSTRIES: COMPANY SNAPSHOT

FIGURE 27 LYONDELLBASELL INDUSTRIES N.V.: COMPANY SNAPSHOT

FIGURE 28 SINOPEC GROUP: COMPANY SNAPSHOT

FIGURE 29 DUCOR PETROCHEMICAL: COMPANY SNAPSHOT

FIGURE 30 BASF SE: COMPANY SNAPSHOT

FIGURE 31 BOREALIS AG: COMPANY SNAPSHOT

FIGURE 32 ARKEMA S.A.: COMPANY SNAPSHOT

FIGURE 33 BRASKEM S.A: COMPANY SNAPSHOT

FIGURE 34 ABU DHABI POLYMERS COMPANY LTD. (BOROUGE): COMPANY SNAPSHOT

FIGURE 35 SASOL LTD: COMPANY SNAPSHOT

FIGURE 36 TOSOH CORPORATION: COMPANY SNAPSHOT

FIGURE 37 POLYONE CORPORATION: COMPANY SNAPSHOT

DOWNLOAD FREE SAMPLE REPORT

License Type

SPEAK WITH OUR ANALYST

Want to know more about the report or any specific requirement?

WANT TO CUSTOMIZE THE REPORT?

Our Clients Speak

We asked them to research ‘ Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te

Yosuke Mitsui

Senior Associate Construction Equipment Sales & Marketing

We asked them to research ‘Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te