Base Year Value ()

x.x %

x.x %

CAGR ()

x.x %

x.x %

Forecast Year Value ()

x.x %

x.x %

Historical Data Period

Largest Region

Forecast Period

Mercado de materiales para neumáticos por tipo (elastómeros, cargas de refuerzo, plastificantes, productos químicos, refuerzos metálicos y refuerzos textiles), aplicación (vehículos comerciales ligeros [LCV], turismos [PC] y vehículos comerciales pesados [HCV]), por región (Norteamérica, Europa, Asia Pacífico, Sudamérica, Oriente Medio y África), tendencias globales y pronóstico de 2022 a 2029

Instant access to hundreds of data points and trends

- Market estimates from 2014-2029

- Competitive analysis, industry segmentation, financial benchmarks

- Incorporates SWOT, Porter's Five Forces and risk management frameworks

- PDF report or online database with Word, Excel and PowerPoint export options

- 100% money back guarantee

Descripción general del mercado de materiales para neumáticos

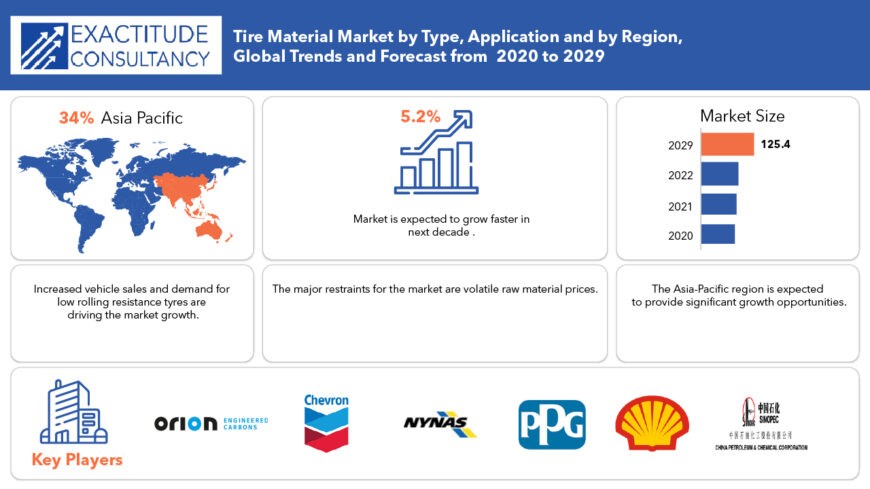

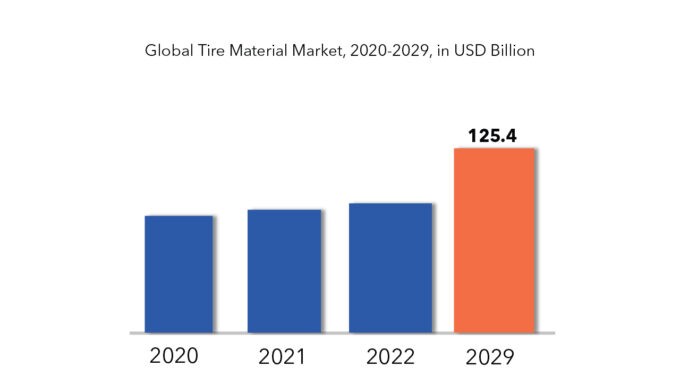

Se estima que el tamaño del mercado mundial de materiales para neumáticos estará valorado en USD 79,46 mil millones en 2020 y se proyecta que alcance los USD 125,40 mil millones para 2029, registrando una CAGR del 5,2%.

El neumático, esencial para adaptarse a una huella adaptada al peso del vehículo, constituye un elemento fundamental de la ingeniería automotriz. Compuestos predominantemente por caucho sintético , caucho natural, textiles, cables de acero, negro de carbono y otros compuestos químicos, los neumáticos, comúnmente inflados neumáticamente, sirven como amortiguadores elásticos que mitigan los impactos que se producen al atravesar terrenos irregulares. En particular, el caucho de butadieno y el caucho de estireno-butadieno son polímeros de caucho artificial primarios que forman parte integral de los procesos de fabricación de neumáticos.

A la par de las crecientes preocupaciones por la sostenibilidad medioambiental, existe una creciente demanda de neumáticos de bajo consumo de combustible destinados a reducir las emisiones de CO2. Los neumáticos de bajo consumo de combustible no sólo ofrecen beneficios medioambientales al reducir tanto las emisiones de CO2 como la contaminación atmosférica, sino que también manifiestan potencial para disminuir las emisiones de CO2 hasta en un 4%, como lo corrobora la Agencia de Protección Ambiental de Estados Unidos.

[título id="attachment_4096" align="aligncenter" width="870"]

El impulso del mercado mundial de materiales para neumáticos depende en gran medida del aumento de la producción de neumáticos y de la creciente necesidad de sustituirlos en las economías emergentes. A medida que el sector automovilístico pone cada vez más énfasis en la contención y la tracción en el diseño de los vehículos, la atención se ha desplazado hacia materiales como el negro de carbono, el alambre y el caucho sintético. Las rigurosas pruebas de materiales en la industria automotriz han impulsado simultáneamente la demanda de materiales para neumáticos, fomentando la expansión dentro del sector de materiales para neumáticos. Además, los gobiernos de todo el mundo han realizado importantes inversiones en tecnología de ingeniería automotriz, lo que ha catalizado aún más el crecimiento del mercado.

Dado el papel fundamental que desempeña la industria automotriz en la conformación del PIB de una nación, las inversiones gubernamentales en este sector resuenan en el mercado de materiales para neumáticos. Sin embargo, las fluctuaciones persistentes en los precios de las materias primas y la gestión deficiente de la oferta y la demanda plantean limitaciones a la expansión de la industria. No obstante, la creciente demanda de materiales neumáticos ecológicos y los esfuerzos de colaboración de los fabricantes de materiales neumáticos y otros actores del mercado en materia de avances tecnológicos presentan grandes oportunidades de mercado, elevando al mismo tiempo la calidad de los productos y las ofertas de mercado.

[título id="attachment_4099" align="aligncenter" width="680"]

Tire Material Market Segment Analysis

In terms of volume, the elastomer category accounts for the biggest share of the tire materials business, compared to other materials. Natural and synthetic rubber are examples of elastomers. The rise in car sales worldwide as a result of population growth and the necessity for mobility raises the demand for tyres, which is expected to rise significantly throughout the forecast period.

The passenger car sector is expected to grow at the fastest rate in the tire materials market. The reduction in loan rates through banking services, as well as different government programs and incentives to develop company units, could boost car sales globally.

Tire Material Market Players

Market players focus on growth strategies, such as new product launches, collaborations, partnerships, operational expansion, mergers & acquisitions, and awareness campaigns. Companies operating the target market can focus on partnerships and collaborations, in order to develop advanced products which in turn create lucrative growth opportunities. Few of the important market players include Orion Engineered Carbons, Royal Dutch Shell, China Petroleum & Chemical Corporation, Chevron Corporation, Nynas AB, Petro China Company Limited, Exxon Mobil Corporation, SIBUR INTERNATIONAL, American Zinc Recycling LLC, PPG Industries and Ralson Goodluck Carbon.

Companies are mainly in the developing and they are competing closely with each other. Innovation is one of the most important and key strategy as it has to be for any market. However, companies in the market have also opted and successfully driven inorganic growth strategies like mergers & acquisition and so on.

- In December 2021, the Goodyear Tire & Rubber Company, an American multinational tire manufacturing company, announced entering into a collaboration agreement with a next generation chemical and energy company, Monolith for development of carbon black from methane for tires.

- In September 2017, Thai Carbon Black Public Company Limited commenced its operation to produce carbon black in a greenfield facility in Jining, China. The plant is being constructed in two phases. Currently, the company has installed a production capacity of 120,000 ton per year in phase 1 and is expected to increase the production capacity to 240,000 tons. This expansion will enable the company to serve its customers in China.

Who Should Buy? Or Key Stakeholders

- Tire material Companies

- Research Organizations

- Investors

- Regulatory Authorities

- Others

Tire Material Market Regional Analysis

The Tire material market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).

- North America: includes US, Canada and Mexico

- Asia Pacific: includes China, Japan, South Korea, India, Australia, ASEAN and Rest of APAC

- Europe: includes UK, Germany, France, Italy, Spain, Russia, and Rest of Europe

- South America: includes Brazil, Argentina and Rest of South America

- Middle East & Africa: includes Turkey, UAE, Saudi Arabia, South Africa, and Rest of MEA

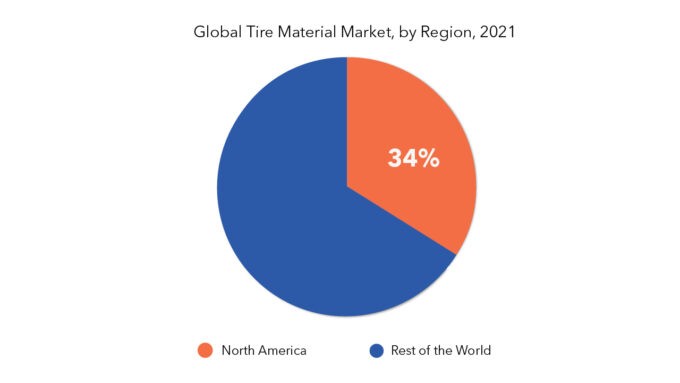

The major share is expected to be occupied by Asia Pacific for global tire material market during the forecast period. In terms of value and volume, the tire materials industry in Asia Pacific is expected to develop at the fastest CAGR over the forecast period. The key nations contributing to the expansion of the global tire materials business in this area are China and India. Major worldwide automakers have invested in Asia-Pacific because of the simple availability of raw resources, political and economic stability, well-developed infrastructure, and inexpensive, skilled labor. As a result, all of these factors are expected to boost the Asia-Pacific tire materials business.

Key Takeaways

- The global tire material market is recording a CAGR of 5.2%

- In terms of volume, the elastomer category accounts for the biggest share of the tire materials business.

- The passenger car sector is expected to grow at the fastest rate in the tire materials market.

- The major share is expected to be occupied by Asia Pacific for global tire material market.

- The tire material market is experiencing steady growth driven by increasing demand for fuel-efficient and high-performance tires, along with advancements in sustainable materials.

Key Market Segments: Tire Material Market

Tire Material Market by Type, 2020-2029, (USD Million) (Kilotons)- Elastomers

- Reinforcing Fillers

- Plasticizers

- Chemicals

- Metal Reinforcements

- Textile Reinforcements

- Light-Weight Commercial Vehicles [LCVs]

- Passenger Cars [Pcs]

- Heavyweight Commercial Vehicles [HCVs]

- North America

- Europe

- Asia Pacific

- South America

- Middle East And Africa

Key Question Answered

- What is the current market size of this high growth market?

- What is the overall growth rate?

- What are the key growth areas, applications, end uses and types?

- Key reasons for growth

- Challenges for growth

- Who are the important market players in this market?

- What are the key strategies of these players?

- What technological developments are happening in this area?

- Introducción

- Definición de mercado

- Segmentación del mercado

- Cronología de la investigación

- Supuestos y limitaciones

- Metodología de la investigación

- Minería de datos

- Investigación secundaria

- Investigación primaria

- Asesoramiento de expertos en la materia

- Controles de calidad

- Revisión final

- Triangulación de datos

- Enfoque de abajo hacia arriba

- Enfoque de arriba hacia abajo

- Flujo de investigación

- Fuentes de datos

- Minería de datos

- Resumen ejecutivo

- Descripción general del mercado

- Perspectivas del mercado mundial de materiales para neumáticos

- Factores impulsores del mercado

- Restricciones del mercado

- Oportunidades de mercado

- Impacto de la COVID-19 en el mercado mundial de materiales para neumáticos

- Perspectivas del mercado mundial de materiales para neumáticos

- Mercado mundial de materiales para neumáticos por tipo (millones de USD) (kilotones)

- Elastómeros

- Rellenos de refuerzo

- Plastificantes

- Productos químicos

- Refuerzos Metálicos

- Refuerzos textiles

- Mercado mundial de materiales para neumáticos por aplicación (millones de USD) (kilotones)

- Vehículos comerciales ligeros [LCV]

- Automóviles de pasajeros [Pzs]

- Vehículos comerciales pesados [HCVS]

- Mercado mundial de materiales para neumáticos por región (millones de USD) (kilotones)

- Introducción

- Asia-Pacífico

- Porcelana

- India

- Japón

- Corea del Sur

- Australia

- Sudeste asiático

- Resto de Asia-Pacífico

- América del norte

- Estados Unidos

- Canadá

- México

- Europa

- Alemania

- Reino Unido

- Francia

- Italia

- España

- Rusia

- Resto de Europa

- Sudamerica

- Brasil

- Argentina

- Colombia

- Resto de Sudamérica

- Oriente Medio y África

- Emiratos Árabes Unidos

- Arabia Saudita

- Sudáfrica

- Resto de Oriente Medio y África

- Perfiles de empresas* (descripción general de la empresa, descripción general de la empresa, tipos ofrecidos, desarrollos recientes)

- Carbones de ingeniería Orion

- Concha real holandesa

- Corporación China de Petróleo y Productos Químicos

- Corporación Chevron

- Nynas AB

- Compañía Petro China Limitada

- Corporación Exxon Mobil

- SIBUR INTERNACIONAL

- Reciclaje de Zinc Americano LLC

- Industrias PPG

*El listado de empresas es orientativo

LISTA DE TABLAS

TABLE 1 GLOBAL TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 2 GLOBAL TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 3 GLOBAL TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 4 GLOBAL TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 5 GLOBAL TIRE MATERIAL MARKET BY REGION (USD MILLIONS), 2020-2029

TABLE 6 GLOBAL TIRE MATERIAL MARKET BY REGION (KILOTONS), 2020-2029

TABLE 7 NORTH AMERICA TIRE MATERIAL MARKET BY COUNTRY (USD MILLIONS), 2020-2029

TABLE 8 NORTH AMERICA TIRE MATERIAL MARKET BY COUNTRY (KILOTONS), 2020-2029

TABLE 9 US TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 10 US TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 11 US TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 12 US TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 13 CANADA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 14 CANADA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 15 CANADA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 16 CANADA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 17 MEXICO TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 18 MEXICO TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 19 MEXICO TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 20 MEXICO TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 21 SOUTH AMERICA TIRE MATERIAL MARKET BY COUNTRY (USD MILLIONS), 2020-2029

TABLE 22 SOUTH AMERICA TIRE MATERIAL MARKET BY COUNTRY (KILOTONS), 2020-2029

TABLE 23 BRAZIL TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 24 BRAZIL TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 25 BRAZIL TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 26 BRAZIL TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 27 ARGENTINA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 28 ARGENTINA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 29 ARGENTINA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 30 ARGENTINA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 31 COLOMBIA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 32 COLOMBIA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 33 COLOMBIA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 34 COLOMBIA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 35 REST OF SOUTH AMERICA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 36 REST OF SOUTH AMERICA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 37 REST OF SOUTH AMERICA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 38 REST OF SOUTH AMERICA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 39 ASIA-PACIFIC TIRE MATERIAL MARKET BY COUNTRY (USD MILLIONS), 2020-2029

TABLE 40 ASIA-PACIFIC TIRE MATERIAL MARKET BY COUNTRY (KILOTONS), 2020-2029

TABLE 41 INDIA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 42 INDIA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 43 INDIA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 44 INDIA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 45 CHINA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 46 CHINA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 47 CHINA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 48 CHINA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 49 JAPAN TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 50 JAPAN TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 51 JAPAN TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 52 JAPAN TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 53 SOUTH KOREA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 54 SOUTH KOREA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 55 SOUTH KOREA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 56 SOUTH KOREA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 57 AUSTRALIA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 58 AUSTRALIA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 59 AUSTRALIA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 60 AUSTRALIA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 61 SOUTH-EAST ASIA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 62 SOUTH-EAST ASIA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 63 SOUTH-EAST ASIA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 64 SOUTH-EAST ASIA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 65 REST OF ASIA PACIFIC TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 66 REST OF ASIA PACIFIC TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 67 REST OF ASIA PACIFIC TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 68 REST OF ASIA PACIFIC TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 69 EUROPE TIRE MATERIAL MARKET BY COUNTRY (USD MILLIONS), 2020-2029

TABLE 70 EUROPE TIRE MATERIAL MARKET BY COUNTRY (KILOTONS), 2020-2029

TABLE 71 GERMANY TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 72 GERMANY TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 73 GERMANY TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 74 GERMANY TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 75 UK TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 76 UK TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 77 UK TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 78 UK TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 79 FRANCE TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 80 FRANCE TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 81 FRANCE TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 82 FRANCE TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 83 ITALY TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 84 ITALY TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 85 ITALY TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 86 ITALY TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 87 SPAIN TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 88 SPAIN TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 89 SPAIN TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 90 SPAIN TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 91 RUSSIA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 92 RUSSIA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 93 RUSSIA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 94 RUSSIA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 95 REST OF EUROPE TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 96 REST OF EUROPE TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 97 REST OF EUROPE TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 98 REST OF EUROPE TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 99 MIDDLE EAST AND AFRICA TIRE MATERIAL MARKET BY COUNTRY (USD MILLIONS), 2020-2029

TABLE 100 MIDDLE EAST AND AFRICA TIRE MATERIAL MARKET BY COUNTRY (KILOTONS), 2020-2029

TABLE 101 UAE TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 102 UAE TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 103 UAE TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 104 UAE TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 105 SAUDI ARABIA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 106 SAUDI ARABIA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 107 SAUDI ARABIA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 108 SAUDI ARABIA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 109 SOUTH AFRICA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 110 SOUTH AFRICA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 111 SOUTH AFRICA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 112 SOUTH AFRICA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 113 REST OF MIDDLE EAST AND AFRICA TIRE MATERIAL MARKET BY TYPE (USD MILLIONS), 2020-2029

TABLE 114 REST OF MIDDLE EAST AND AFRICA TIRE MATERIAL MARKET BY TYPE (KILOTONS), 2020-2029

TABLE 115 REST OF MIDDLE EAST AND AFRICA TIRE MATERIAL MARKET BY APPLICATION (USD MILLIONS), 2020-2029

TABLE 116 REST OF MIDDLE EAST AND AFRICA TIRE MATERIAL MARKET BY APPLICATION (KILOTONS), 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL TIRE MATERIAL MARKET BY TYPE, USD MILLION, 2020-2029

FIGURE 9 GLOBAL TIRE MATERIAL MARKET BY APPLICATION, USD MILLION, 2020-2029

FIGURE 10 GLOBAL TIRE MATERIAL MARKET BY REGION, USD MILLION, 2020-2029

FIGURE 11 PORTER’S FIVE FORCES MODEL

FIGURE 12 GLOBAL TIRE MATERIAL MARKET BY TYPE, USD MILLION, 2020-2029

FIGURE 13 GLOBAL TIRE MATERIAL MARKET BY APPLICATION, USD MILLION, 2020-2029

FIGURE 14 GLOBAL TIRE MATERIAL MARKET BY REGION, USD MILLION, 2020-2029

FIGURE 15 TIRE MATERIAL MARKET BY REGION 2020

FIGURE 16 MARKET SHARE ANALYSIS

FIGURE 17 ORION ENGINEERED CARBONS: COMPANY SNAPSHOT

FIGURE 18 ROYAL DUTCH SHELL: COMPANY SNAPSHOT

FIGURE 19 CHINA PETROLEUM & CHEMICAL CORPORATION: COMPANY SNAPSHOT

FIGURE 20 CHEVRON CORPORATION: COMPANY SNAPSHOT

FIGURE 21 NYNAS AB: COMPANY SNAPSHOT

FIGURE 22 PETRO CHINA COMPANY LIMITED: COMPANY SNAPSHOT

FIGURE 23 EXXON MOBIL CORPORATION: COMPANY SNAPSHOT

FIGURE 24 SIBUR INTERNATIONAL: COMPANY SNAPSHOT

FIGURE 25 AMERICAN ZINC RECYCLING LLC: COMPANY SNAPSHOT

FIGURE 26 PPG INDUSTRIES: COMPANY SNAPSHOT

DOWNLOAD FREE SAMPLE REPORT

License Type

SPEAK WITH OUR ANALYST

Want to know more about the report or any specific requirement?

WANT TO CUSTOMIZE THE REPORT?

Our Clients Speak

We asked them to research ‘ Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te

Yosuke Mitsui

Senior Associate Construction Equipment Sales & Marketing

We asked them to research ‘Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te