Base Year Value ()

x.x %

x.x %

CAGR ()

x.x %

x.x %

Forecast Year Value ()

x.x %

x.x %

Historical Data Period

Largest Region

Forecast Period

Mercado de archivos independientes del proveedor por tipo (PACS, software VNA), modo de entrega (en el sitio, híbrido, alojado en la nube), modelo de uso (departamentos individuales, departamentos múltiples, sitios múltiples) y por región (América del Norte, Europa, Asia Pacífico, América del Sur, Medio Oriente y África), tendencias globales y pronóstico de 2022 a 2029

Instant access to hundreds of data points and trends

- Market estimates from 2014-2029

- Competitive analysis, industry segmentation, financial benchmarks

- Incorporates SWOT, Porter's Five Forces and risk management frameworks

- PDF report or online database with Word, Excel and PowerPoint export options

- 100% money back guarantee

Descripción general del mercado de archivos independientes del proveedor

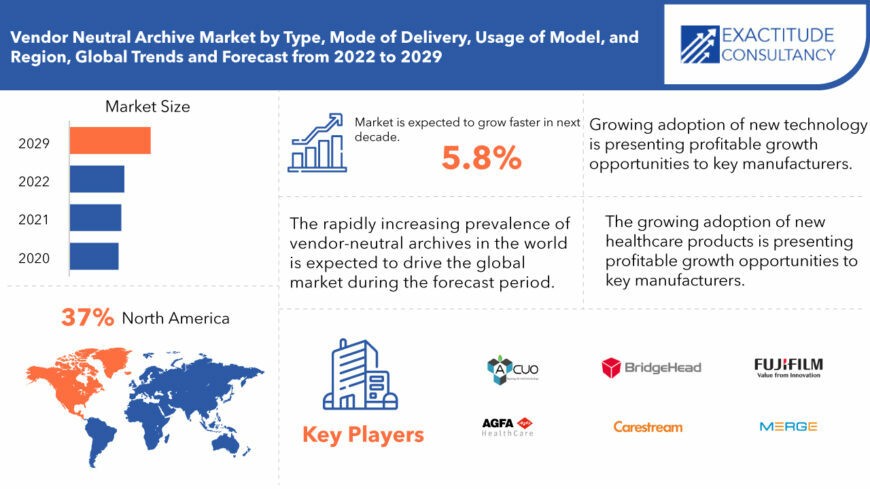

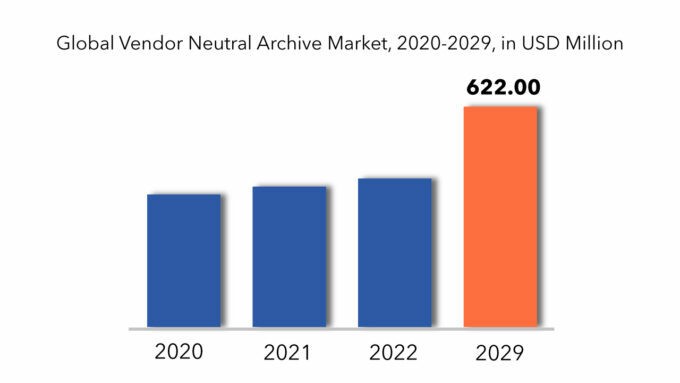

Se espera que el mercado global de archivos independientes de proveedores crezca a una tasa anual compuesta de más del 5,8 % entre 2022 y 2029. Se espera que alcance más de 622 millones de dólares en 2029, frente a los 374 millones de dólares de 2020.

La expansión observada en este mercado se puede atribuir a varios factores, entre ellos, el número sustancial de aprobaciones otorgadas para dispositivos de cierre vascular, la incidencia prevalente de enfermedades cardiovasculares, la creciente prevalencia de la obesidad, el énfasis creciente de las entidades del mercado en dispositivos de cierre vascular de gran calibre, la creciente demografía geriátrica, el panorama favorable de reembolso para procedimientos de radiología intervencionista y el mayor enfoque en el manejo eficaz de la pérdida de sangre durante las intervenciones quirúrgicas. Además, los mercados emergentes presentan perspectivas de crecimiento lucrativas para los participantes del mercado, junto con la proliferación de hospitales y centros quirúrgicos, que en conjunto ofrecen sólidas oportunidades de crecimiento. Sin embargo, desafíos como el requisito de profesionales altamente calificados, los riesgos inherentes asociados con los dispositivos de cierre vascular y el estricto marco regulatorio pueden impedir la expansión del mercado hasta cierto punto. El mercado de dispositivos de cierre vascular está segmentado en función del tipo, el acceso, el procedimiento y la región.

El mercado de dispositivos de cierre vascular (VCD) abarca una variedad de dispositivos médicos diseñados para lograr la hemostasia posterior a procedimientos vasculares mínimamente invasivos, en particular cateterismo cardíaco e intervenciones vasculares periféricas. Estos dispositivos son fundamentales para sellar los sitios de punción dentro de las arterias o venas, mitigando así el riesgo de complicaciones hemorrágicas posteriores al procedimiento. Los VCD presentan claras ventajas sobre las técnicas de compresión manual convencionales, que incluyen una hemostasia acelerada, un tiempo reducido para la deambulación, una menor incomodidad del paciente y estancias hospitalarias más breves.

| ATRIBUTO | DETALLES |

| Periodo de estudio | 2020-2029 |

| Año base | 2021 |

| Año estimado | 2022 |

| Año pronosticado | 2022-2029 |

| Periodo histórico | 2018-2020 |

| Unidad | Valor (miles de millones de USD) |

| Segmentación | Por tipo, por modo de entrega, uso del modelo |

| Por tipo |

|

| Por modo de entrega |

|

| Por uso del modelo |

|

| Por región |

|

El panorama regulatorio global que rige los dispositivos de cierre vascular se caracteriza por un marco multifacético que comprende estándares, pautas y regulaciones promulgadas por autoridades regulatorias en diferentes naciones y regiones. Entidades como la Administración de Alimentos y Medicamentos de los Estados Unidos (FDA), la Agencia Europea de Medicamentos (EMA) y la Agencia Japonesa de Productos Farmacéuticos y Dispositivos Médicos (PMDA) delinean los requisitos relacionados con la seguridad, eficacia y calidad de los dispositivos de cierre vascular mediante procesos de aprobación previos a la comercialización, mecanismos de vigilancia posterior a la comercialización y evaluaciones de rutina.

[título id="attachment_6568" align="aligncenter" width="870"]

Frequently Asked Questions

• What is the worth of the global vendor neutral archive market?

The vendor neutral archive market size has crossed USD 374 million in 2020 and will observe a CAGR of more than 5.8% up to 2027 driven by the rising technological advancements in molecular biology, genomics, and microbial diversity.

• What is the size of the North America vendor neutral archive industry?

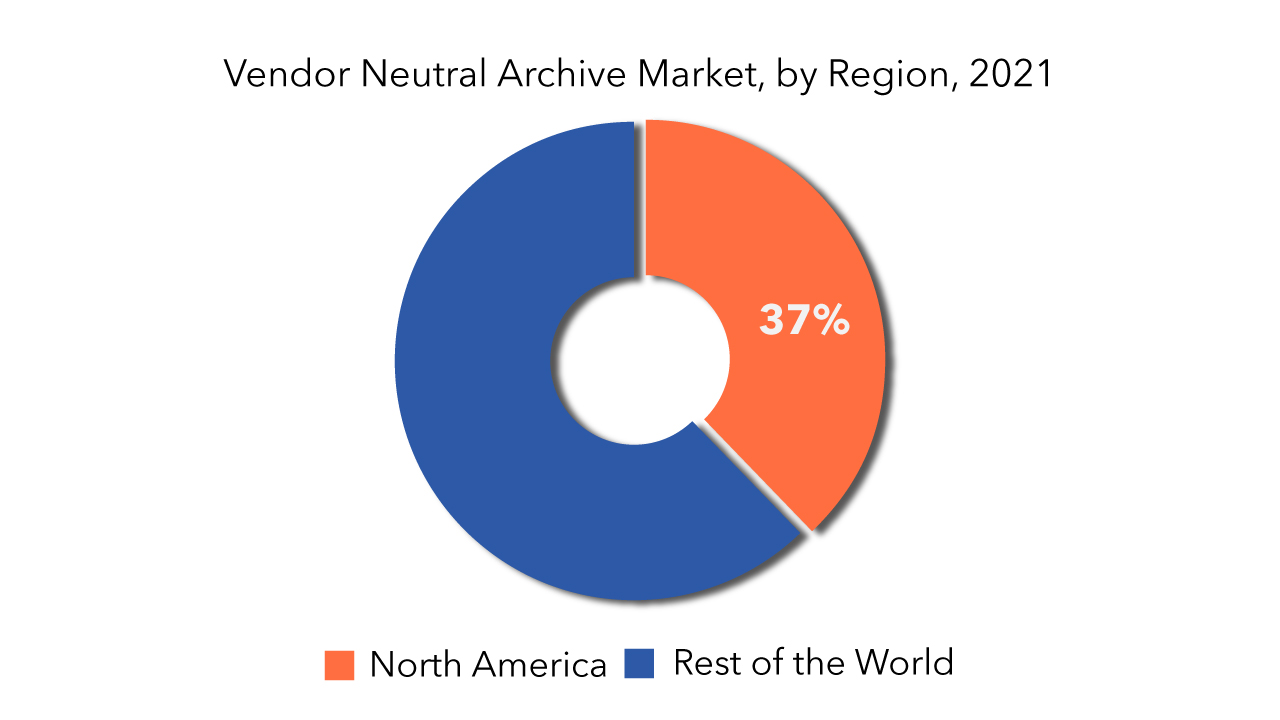

North America held more than 37% of the vendor neutral archive market revenue share in 2020 and will witness expansion with the surging demand for vendor neutral archive in countries, including U.S. and Canada.

• What are the upcoming trends of the vendor neutral archive market, globally?

The upcoming trends in the vendor neutral archive market are expansion in the technological advancements in vendor neutral archive will drive industry revenue in the next few years

• What is the CAGR of the vendor neutral archive market?

The global vendor neutral archive market registered a CAGR of 5.8% from 2022 to 2029. The application segment was the highest revenue contributor to the market, with 374 million in 2020, and is estimated to reach 622 million by 2029, with a CAGR of 7%.

• Which are the top companies to hold the market share in the vendor neutral archive market?

Key players profiled in the report include Acuo Technologies (U.S.), Agfa HealthCare (Belgium), BridgeHead Software (U.K.), Carestream Health (U.S.), Dell, Inc. (U.S.), GE Healthcare (U.K.), Fujifilm Corporation (Japan), Merge Health (U.S.), McKesson Corporation (U.S.), Philips Healthcare (The Netherlands), Siemens Healthcare (Germany), and TeraMedica (U.S.).

• What is the leading application of the vendor neutral archive market?

The healthcare application is expected to increase the most.

• Which is the largest regional market for vendor neutral archive market?

North America is the largest regional market for vendor neutral archive.

Vendor Neutral Archive Market Segment Analysis

The two key segments of the PACS market are departmental PACS and enterprise PACS. The vendor-neutral archive market is divided into three types: passive approximators, active approximators, and external hemostatic devices. The market for the vendor-neutral archive is dominated by passive approximators. The growing number of vascular closure device approvals, as well as the numerous benefits connected with these devices, such as ease of use and a lower complication rate in patients, can be attributable to the substantial proportion of this market. Along with the worldwide VNA market, the PACS market is included to provide a comparative overview of both healthcare information systems. The product lifecycles of each of these systems differ greatly. The vendor-neutral archives (VNA) market is thought to be in the same phase (exponential phase) as the PACS market was 10 to 15 years ago. The PACS market, on the other hand, is a mature industry defined by market participants attempting to invest in product innovation and seeking new consumer groups.

The market is divided into three segments based on delivery mode: on-premise VNAs, hybrid VNAs, and entirely cloud-hosted VNAs. Because this approach is preferred over others, on-premise VNAs currently dominate the industry in terms of overall revenue contribution. This choice is due to the superior data control and security afforded by on-premise VNA solutions. However, due to the high capital investment required for on-premise VNAs, hybrid VNA systems that include a cloud-based component for storage are currently attracting the interest of small and medium-sized healthcare facilities. As a result, hybrid VNA solutions are expected to grow faster than on-premise solutions.

The benefits of vendor-neutral archives over PACS in terms of interoperability, flexibility, and accessibility are driving market adoption of VNA technology. In addition, favorable and promising government reforms in the sector of healthcare information technology are encouraging the market. Rising data breaches, the complexity of the VNA idea, the lack of a proper industry-accepted definition of VNAs, and long VNA lifecycles are the key impediments to market expansion (that impact VNA deployment decisions). As a result, the market is poised to witness trends such as VNA integration with EHRs, the use of cloud computing solutions for VNA products, and a holistic approach to providing superior patient care.Picture archiving and communication systems (PACS) are one of the most extensively used technologies in hospitals around the world. PACS is used in more than 80% of hospitals in affluent countries such as the United States, the United Kingdom, and Japan. The scope is visible in developing countries, notably in Asian countries such as India and China. These countries' healthcare facilities are now transitioning from the usage of different services to integrated systems for sharing and storing medical pictures. PACS adoption is fast expanding in these countries as healthcare sectors improve, healthcare expenditure rises, and people become more aware of the need for picture archiving and communication systems. These technologies are generally used in radiology.

The benefit of an active vendor-neutral archive in shortening time to ambulation and hemostasis commanded more than 58 percent of revenue share in 2020. The active vascular closure device employs a variety of ways for direct closure of the artery entry site, including the use of collagen or suture-based materials. Increasing product availability to a bigger population opens up revenue generation opportunities for the segment. Collagen plug devices such as Angio-seal and Mynx, as well as ExoSeal and Starclose devices, are examples of these devices. As a result, more product releases by market participants will benefit segment growth.

Picture archiving and communication systems (PACS) are one of the most extensively used technologies in hospitals around the world. PACS is used in more than 80% of hospitals in affluent countries such as the United States, the United Kingdom, and Japan. The scope is visible in developing countries, notably in Asian countries such as India and China. These countries' healthcare facilities are now transitioning from the usage of different services to integrated systems for sharing and storing medical pictures. PACS adoption is fast expanding in these countries as healthcare sectors improve, healthcare expenditure rises, and people become more aware of the need for picture archiving and communication systems. These technologies are generally used in radiology.

[caption id="attachment_6572" align="aligncenter" width="680"]

Vendor Neutral Archive Market Key Players

The prominent players in the vendor-neutral archive market include Acuo Technologies (U.S.), Agfa HealthCare (Belgium), BridgeHead Software (U.K.), Carestream Health (U.S.), Dell, Inc. (U.S.), GE Healthcare (U.K.), Fujifilm Corporation (Japan), Merge Health (U.S.), McKesson Corporation (U.S.), Philips Healthcare (The Netherlands), Siemens Healthcare (Germany), and TeraMedica (U.S.).

Who Should Buy? Or Key stakeholders

- Investors

- Environment, Health, and Safety Professionals

- Research Organizations

- Medical industry

- Regulatory Authorities

- Others

Key Takeaways

- The global vendor-neutral archive market is expected to grow at more than 5.8% CAGR.

- The market for the vendor-neutral archive is dominated by passive approximators.

- Based on delivery mode, on-premise VNAs currently dominate the industry.

- The North America market is predicted to lead the global vendor neutral archive market.

- The major trend in the Vendor Neutral Archive (VNA) market is the integration of artificial intelligence (AI) for advanced data analytics and workflow optimization.

Vendor Neutral Archive Market Regional Analysis

The vendor-neutral archive market is divided into major regions- North America, Europe, South America, Asia Pacific, and middle east & Africa. North America is the largest regional segment in 2021.

- North America: includes the US, Canada, Mexico

- Europe: includes UK, Germany, France, Italy, Spain, Russia, and Rest of Europe

- Asia Pacific: includes China, Japan, South Korea, India, Australia, ASEAN and Rest of APAC

- South America: includes Brazil, Argentina and Rest of South America

- Middle East & Africa: includes Turkey, UAE, Saudi Arabia, South Africa, and Rest of MEA

When compared to other regional markets, the North America market is predicted to lead the global vendor neutral archive market with a greater revenue share, and this dominance is expected to continue during the forecast period. This might be ascribed to the region's well-developed healthcare industry and the presence of important market participants. Europe has the second-largest revenue share in the global vendor neutral archive market, followed by Asia Pacific, Latin America, and the Middle East and Africa, in that order. The Asia Pacific market is expected to grow the fastest in terms of revenue, owing to increased adoption of imaging in various departments such as cardiology, pathology, oncology, and dermatology, as well as increased government initiatives for the development of healthcare sector in emerging markets.

[caption id="attachment_6573" align="aligncenter" width="680"]

Key Market Segments: Global vascular closure devices Market

Vendor Neutral Archive Market by Type, 2020-2029, (USD Million)- PACS

- VNA Software

- On-Site

- Hybrid

- Cloud-Hosted

- Single Department

- Multiple Department

- Multiple Sites

- North America

- Europe

- Asia Pacific

- South America

- Middle East And Africa

Key Question Answered

- What is the current market size of this high growth market?

- What is the overall growth rate?

- What are the key growth areas, types, Applications?

- Key reasons for growth

- Challenges for growth

- What technological developments are happening in this area?

- INTRODUCCIÓN

- DEFINICIÓN DE MERCADO

- SEGMENTACIÓN DEL MERCADO

- CRONOGRAMAS DE INVESTIGACIÓN

- SUPUESTOS Y LIMITACIONES

- METODOLOGÍA DE LA INVESTIGACIÓN

- MINERÍA DE DATOS

- INVESTIGACIÓN SECUNDARIA

- INVESTIGACIÓN PRIMARIA

- ASESORAMIENTO DE EXPERTOS EN LA MATERIA

- CONTROLES DE CALIDAD

- REVISIÓN FINAL

- TRIANGULACIÓN DE DATOS

- ENFOQUE DE ABAJO HACIA ARRIBA

- ENFOQUE DE ARRIBA HACIA ABAJO

- FLUJO DE INVESTIGACIÓN

- FUENTES DE DATOS

- MINERÍA DE DATOS

- RESUMEN EJECUTIVO

- PANORAMA DEL MERCADO

- PERSPECTIVA DEL MERCADO DE ARCHIVOS NEUTRAL CON RESPECTO A PROVEEDORES GLOBALES

- IMPULSORES DEL MERCADO

- RESTRICCIONES DEL MERCADO

- OPORTUNIDADES DE MERCADO

- IMPACTO DEL COVID-19 EN EL MERCADO DE ARCHIVOS INDEPENDIENTES DEL PROVEEDOR

- MODELO DE LAS CINCO FUERZAS DE PORTER

- AMENAZA DE NUEVOS INGRESANTES

- AMENAZA DE SUSTITUTOS

- PODER DE NEGOCIACIÓN DE LOS PROVEEDORES

- PODER DE NEGOCIACIÓN DE LOS CLIENTES

- GRADO DE COMPETENCIA

- ANÁLISIS DE LA CADENA DE VALOR DE LA INDUSTRIA

- PERSPECTIVA DEL MERCADO DE ARCHIVOS NEUTRAL CON RESPECTO A PROVEEDORES GLOBALES

- MERCADO GLOBAL DE ARCHIVOS NEUTRAL EN MATERIA DE PROVEEDORES POR TIPO (MILLONES DE USD)

- PACÍFICOS

- SOFTWARE DE ANÁLISIS DE VENTANAS

- MERCADO GLOBAL DE ARCHIVOS NEUTRAL EN RELACIÓN CON EL PROVEEDOR POR MODO DE ENTREGA (MILLONES DE USD)

- IN SITU

- HÍBRIDO

- ALOJADO EN LA NUBE

- MERCADO GLOBAL DE ARCHIVOS NEUTRAL EN RELACIÓN CON EL PROVEEDOR POR USO DEL MODELO (MILLONES DE USD)

- DEPARTAMENTO ÚNICO

- DEPARTAMENTO MÚLTIPLE

- SITIOS MÚLTIPLES

- MERCADO DE ARCHIVOS NEUTRAL EN MUNDO POR REGIÓN

- AMERICA DEL NORTE

- A NOSOTROS

- CANADÁ

- MÉXICO

- SUDAMERICA

- BRASIL

- ARGENTINA

- COLOMBIA

- RESTO DE SUDAMÉRICA

- EUROPA

- ALEMANIA

- Reino Unido

- FRANCIA

- ITALIA

- ESPAÑA

- RUSIA

- RESTO DE EUROPA

- ASIA PACÍFICO

- INDIA

- PORCELANA

- JAPÓN

- COREA DEL SUR

- AUSTRALIA

- ASIA SUDESTE

- RESTO DE ASIA PACÍFICO

- ORIENTE MEDIO Y ÁFRICA

- Emiratos Árabes Unidos

- ARABIA SAUDITA

- SUDÁFRICA

- RESTO DE ORIENTE MEDIO Y ÁFRICA

- AMERICA DEL NORTE

- PERFILES DE EMPRESAS* (DESCRIPCIÓN GENERAL DEL NEGOCIO, RESEÑA DE LA EMPRESA, PRODUCTOS OFRECIDOS, DESARROLLOS RECIENTES)

- TECNOLOGÍAS ACUO

- AGFA SALUD

- SOFTWARE DE CABEZA DE PUENTE

- SALUD DE CARESTREAM

- Compañía: DELL, INC.

- ATENCIÓN MÉDICA GE

- CORPORACIÓN FUJIFILM

- FUSIONAR SALUD

- CORPORACIÓN MCKESSON

- ATENCIÓN MÉDICA PHILIPS

- ATENCIÓN MÉDICA SIEMENS

- TERAMEDICA (EE. UU.). CIRUGÍA INTUITIVA

- OTROS JUGADORES *EL LISTADO DE EMPRESAS ES ORIENTATIVO

LISTA DE TABLAS

TABLE 1 GLOBAL VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 2 GLOBAL VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 3 GLOBAL VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 4 GLOBAL VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 5 GLOBAL VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 6 GLOBAL VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 7 GLOBAL VENDOR NEUTRAL ARCHIVE MARKET BY REGION (USD MILLIONS) 2020-2029

TABLE 8 GLOBAL VENDOR NEUTRAL ARCHIVE MARKET BY REGION 2020-2029

TABLE 9 US VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 10 US VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 11 US VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 12 US VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 13 US VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 14 US VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 15 CANADA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 16 CANADA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 17 CANADA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 18 CANADA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 19 CANADA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 20 CANADA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 21 MEXICO VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 22 MEXICO VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 23 MEXICO VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 24 MEXICO VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 25 MEXICO VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 26 MEXICO VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 27 BRAZIL VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 28 BRAZIL VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 29 BRAZIL VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 30 BRAZIL VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 31 BRAZIL VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 32 BRAZIL VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 33 ARGENTINA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 34 ARGENTINA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 35 ARGENTINA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 36 ARGENTINA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 37 ARGENTINA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 38 ARGENTINA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 39 COLOMBIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 40 COLOMBIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 41 COLOMBIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 42 COLOMBIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 43 COLOMBIA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 44 COLOMBIA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 45 REST OF SOUTH AMERICA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 46 REST OF SOUTH AMERICA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 47 REST OF SOUTH AMERICA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 48 REST OF SOUTH AMERICA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 49 REST OF SOUTH AMERICA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 50 REST OF SOUTH AMERICA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 51 INDIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 52 INDIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 53 INDIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 54 INDIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 55 INDIA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 56 INDIA VENDOR NEUTRAL ARCHIVE MARKET BY END-USER 2020-2029

TABLE 57 CHINA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 58 CHINA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 59 CHINA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 60 CHINA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 61 CHINA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 62 CHINA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 63 JAPAN VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 64 JAPAN VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 65 JAPAN VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 66 JAPAN VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 67 JAPAN VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 68 JAPAN VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 69 SOUTH KOREA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 70 SOUTH KOREA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 71 SOUTH KOREA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 72 SOUTH KOREA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 73 SOUTH KOREA M MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 74 SOUTH KOREA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 75 AUSTRALIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 76 AUSTRALIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 77 AUSTRALIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 78 AUSTRALIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 79 AUSTRALIA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 80 AUSTRALIA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 81 SOUTH-EAST ASIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 82 SOUTH-EAST ASIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 83 SOUTH-EAST ASIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 84 SOUTH-EAST ASIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 85 SOUTH-EAST ASIA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 86 SOUTH-EAST ASIA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 87 REST OF ASIA PACIFIC VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 88 REST OF ASIA PACIFIC VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 89 REST OF ASIA PACIFIC VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 90 REST OF ASIA PACIFIC VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 91 REST OF ASIA PACIFIC VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 92 REST OF ASIA PACIFIC VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 93 GERMANY VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 94 GERMANY VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 95 GERMANY VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 96 GERMANY VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 97 GERMANY VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 98 GERMANY VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 99 UK VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 100 UK VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 101 UK VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 102 UK VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 103 UK VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 104 UK VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 105 FRANCE VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 106 FRANCE VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 107 FRANCE VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 108 FRANCE VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 109 FRANCE VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 110 FRANCE VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 111 ITALY VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 112 ITALY VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 113 ITALY VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 114 ITALY VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 115 ITALY VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 116 ITALY VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 117 SPAIN VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 118 SPAIN VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 119 SPAIN VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 120 SPAIN VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 121 SPAIN VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 122 SPAIN VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 123 RUSSIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 124 RUSSIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 125 RUSSIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 126 RUSSIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 127 RUSSIA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 128 RUSSIA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 129 REST OF EUROPE VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 130 REST OF EUROPE VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 131 REST OF EUROPE VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 132 REST OF EUROPE VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 133 REST OF EUROPE VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 134 REST OF EUROPE VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 135 UAE VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 136 UAE VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 137 UAE VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 138 UAE VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 139 UAE VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 140 UAE VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 141 SAUDI ARABIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 142 SAUDI ARABIA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 143 SAUDI ARABIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 144 SAUDI ARABIA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 145 SAUDI ARABIA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 146 SAUDI ARABIA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 147 SOUTH AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 148 SOUTH AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 149 SOUTH AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 150 SOUTH AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 151 SOUTH AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 152 SOUTH AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

TABLE 153 REST OF MIDDLE EAST AND AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE(USD MILLIONS) 2020-2029

TABLE 154 REST OF MIDDLE EAST AND AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY TYPE 2020-2029

TABLE 155 REST OF MIDDLE EAST AND AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY (USD MILLIONS) 2020-2029

TABLE 156 REST OF MIDDLE EAST AND AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY 2020-2029

TABLE 157 REST OF MIDDLE EAST AND AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL(USD MILLIONS) 2020-2029

TABLE 158 REST OF MIDDLE EAST AND AFRICA VENDOR NEUTRAL ARCHIVE MARKET BY USAGE OF MODEL 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL VENDORS NEUTRAL ARCHIVE MARKET BY VEHICLE TYPE, USD MILLION, 2020-2029

FIGURE 9 GLOBAL VENDORS NEUTRAL ARCHIVE MARKET BY MODE OF DELIVERY, USD MILLION, 2020-2029

FIGURE 10 GLOBAL VENDORS NEUTRAL ARCHIVE MARKET BY END USER, USD MILLION, 2020-2029

FIGURE 11 GLOBAL VENDORS NEUTRAL ARCHIVE MARKET BY REGION, USD MILLION, 2020-2029

FIGURE 12 PORTER’S FIVE FORCES MODEL

FIGURE 13 NORTH AMERICA VENDOR NEUTRAL ARCHIVE MARKET SNAPSHOT

FIGURE 14 EUROPE VENDOR NEUTRAL ARCHIVE MARKET SNAPSHOT

FIGURE 15 ASIA PACIFIC VENDOR NEUTRAL ARCHIVE MARKET SNAPSHOT

FIGURE 16 SOUTH AMERICA VENDOR NEUTRAL ARCHIVE MARKET SNAPSHOT

FIGURE 17 MIDDLE EAST & AFRICA VENDOR NEUTRAL ARCHIVE MARKET SNAPSHOT

FIGURE 18 ACUO TECHNOLOGIES: COMPANY SNAPSHOT

FIGURE 19 AGFA HEALTHCARE: COMPANY SNAPSHOT

FIGURE 20 BRIDGEHEAD SOFTWARE : COMPANY SNAPSHOT

FIGURE 21 CARESTREAM HEALTH: COMPANY SNAPSHOT

FIGURE 22 DELL, INC. : COMPANY SNAPSHOT

FIGURE 23 GE HEALTHCARE : COMPANY SNAPSHOT

FIGURE 24 FUJIFILM CORPORATION : COMPANY SNAPSHOT

FIGURE 25 MERGE HEALTH: COMPANY SNAPSHOT

FIGURE 26 MCKESSON CORPORATION : COMPANY SNAPSHOT

FIGURE 27 PHILIPS HEALTHCARE: COMPANY SNAPSHOT

FIGURE 28 SIEMENS HEALTHCARE: COMPANY SNAPSHOT

FIGURE 29 TERAMEDICA: COMPANY SNAPSHOT

DOWNLOAD FREE SAMPLE REPORT

License Type

SPEAK WITH OUR ANALYST

Want to know more about the report or any specific requirement?

WANT TO CUSTOMIZE THE REPORT?

Our Clients Speak

We asked them to research ‘ Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te

Yosuke Mitsui

Senior Associate Construction Equipment Sales & Marketing

We asked them to research ‘Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te