Base Year Value ()

x.x %

x.x %

CAGR ()

x.x %

x.x %

Forecast Year Value ()

x.x %

x.x %

Historical Data Period

Largest Region

Forecast Period

Mercato dell'anidride ftalica per processo (ossidazione catalitica dell'o-xilene, ossidazione catalitica del naftalene), applicazione (plastificanti, resine alchidiche, resine poliestere insature, altri), settore di utilizzo finale (vernici e rivestimenti, automotive, elettrico ed elettronico, edilizia e costruzioni, agricoltura, nautica, altri) e regione, tendenze globali e previsioni dal 2022 al 2029

Instant access to hundreds of data points and trends

- Market estimates from 2014-2029

- Competitive analysis, industry segmentation, financial benchmarks

- Incorporates SWOT, Porter's Five Forces and risk management frameworks

- PDF report or online database with Word, Excel and PowerPoint export options

- 100% money back guarantee

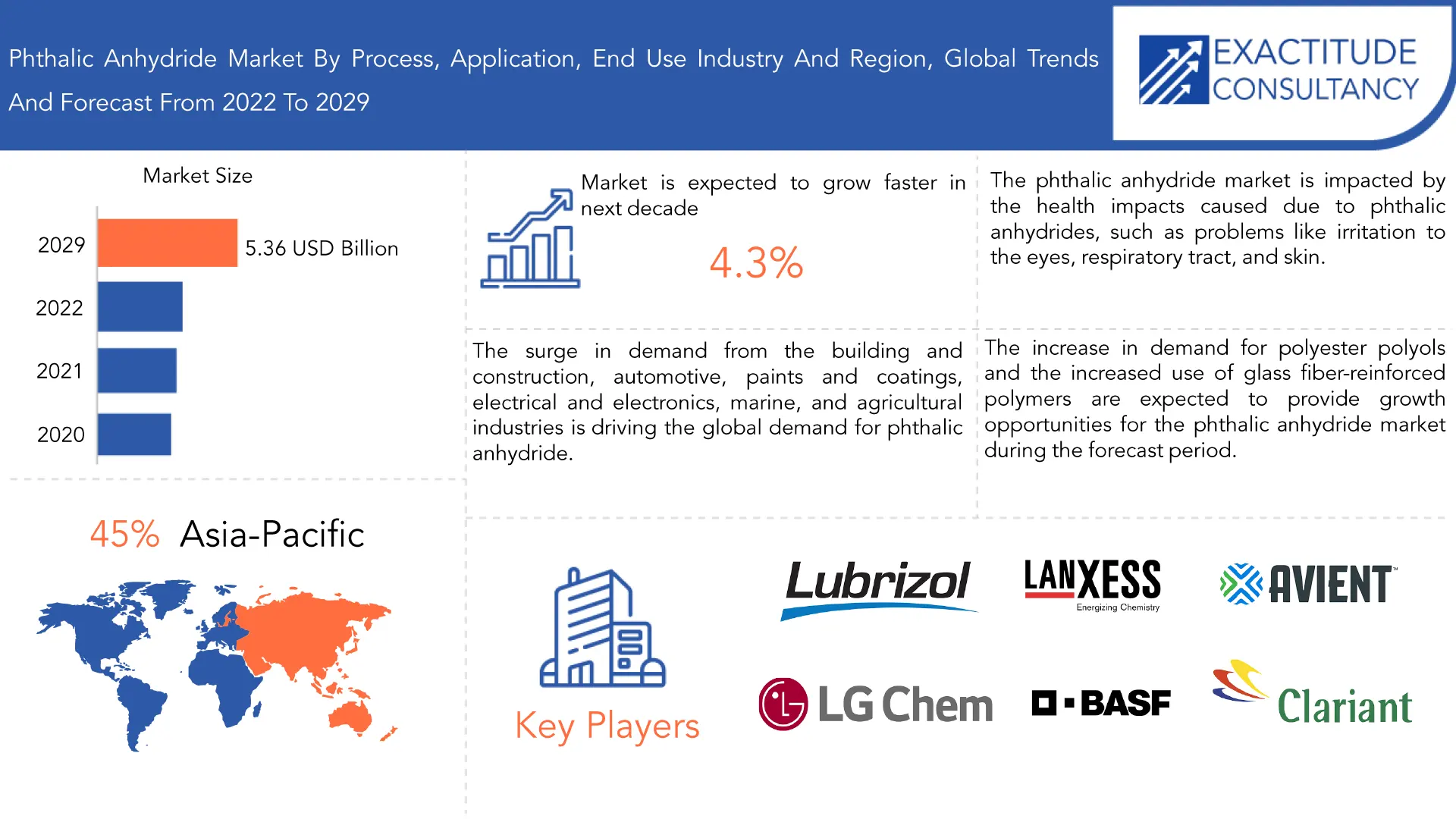

Panoramica del mercato dell'anidride ftalica

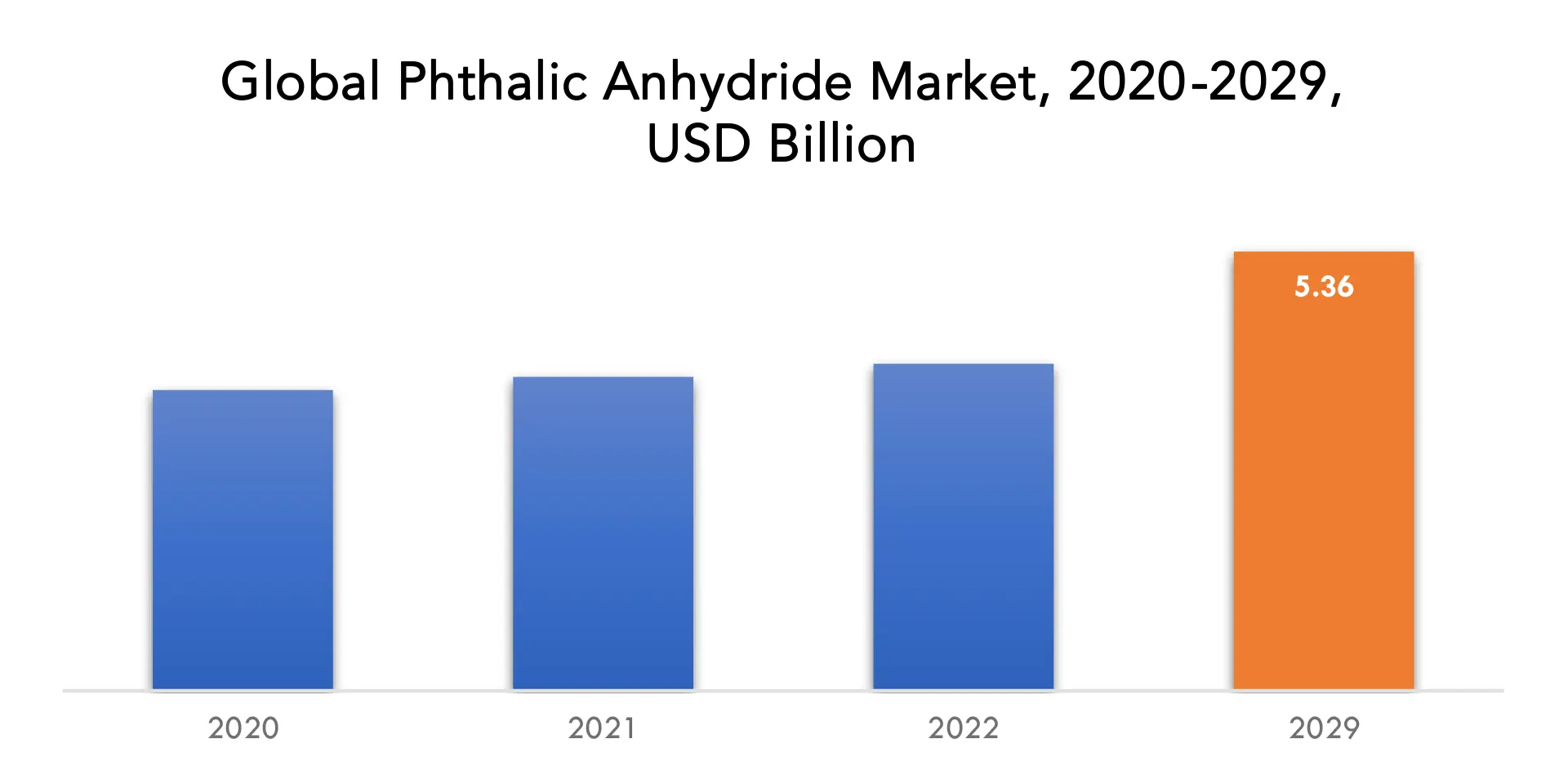

Si prevede che il mercato dell'anidride ftalica crescerà al 4,3% di CAGR dal 2022 al 2029. Si prevede che raggiungerà oltre 5,36 miliardi di USD entro il 2029 dai 3,83 miliardi di USD del 2021.

L'anidride ftalica è un composto chimico con formula C8H4O3. È una delle sostanze chimiche più importanti nella produzione di esteri ftalici e deriva dall'ossidazione dell'orto-xilene o naftalene. L'anidride ftalica è un solido bianco con un odore forte e pungente che sublima ad alte temperature. I plastificanti , in particolare gli esteri ftalici, sono una delle applicazioni più comuni per l'anidride ftalica. Questi esteri sono utilizzati per migliorare la flessibilità, la durata e la trasparenza delle materie plastiche. Sono frequentemente utilizzati nella produzione di PVC (cloruro di polivinile), ampiamente utilizzato nei settori dell'edilizia , dell'automotive e dell'imballaggio.

L'anidride ftalica viene anche utilizzata per produrre resine alchidiche, che sono rivestimenti in pitture, vernici e smalti. Queste resine offrono un'aderenza eccezionale, resistenza alle intemperie e durevolezza. Viene anche utilizzata come precursore nella produzione di vari coloranti, pigmenti e prodotti farmaceutici. Tuttavia, l'anidride ftalica e i suoi derivati hanno sollevato preoccupazioni sui loro potenziali effetti sulla salute e sull'ambiente. Alcuni ftalati sono stati collegati in studi a effetti negativi sulla salute umana, tra cui disturbi endocrini e disturbi dell'apparato riproduttivo. Come risultato di queste preoccupazioni, c'è stata una maggiore enfasi sullo sviluppo di plastificanti alternativi e sulla riduzione dell'uso di ftalati in varie applicazioni. Alcune regioni hanno implementato misure normative per limitare l'uso di alcuni ftalati in specifici prodotti di consumo, con l'obiettivo di ridurre i potenziali rischi associati al loro uso.

Si prevede che un aumento degli investimenti nel settore delle vernici e dei rivestimenti stimolerà il mercato dell'anidride ftalica. L'anidride ftalica è una resina di riferimento fondamentale nella produzione di vernici e rivestimenti basati su materiali ad alte prestazioni e resina alchidica, come i rivestimenti architettonici a base di solventi. L'espansione del settore delle vernici e dei rivestimenti è dovuta ai rapidi investimenti infrastrutturali nei paesi in via di sviluppo. Ad esempio, nel 2019 l'industria indiana delle vernici era valutata oltre 57 trilioni di rupie indiane. Inoltre, i materiali contenenti anidride ftalica sono ampiamente utilizzati nelle applicazioni di rivestimento per automobili, elettrodomestici, dispositivi medici e mobili. Le anidridi acide sono utilizzate come plastificanti per PVC e altre materie plastiche per migliorare la stabilità della temperatura nei rivestimenti di fili e cavi. Di conseguenza, si prevede che il crescente utilizzo di anidride ftalica in vernici e rivestimenti stimolerà la crescita del mercato.

[caption id="allegato_25697" align="aligncenter" width="1920"]

Numerosi ostacoli limitano il mercato dell'anidride ftalica. Innanzitutto, c'è una crescente domanda di plastificanti alternativi a causa di normative più severe e crescenti preoccupazioni sui potenziali effetti sulla salute e sull'ambiente dei ftalati. Inoltre, la volatilità dei prezzi delle materie prime, in particolare per l'orto-xilene e il naftalene, ha un impatto sul mercato. La disponibilità di alternative e lo spostamento in vari settori verso soluzioni più sostenibili e rispettose dell'ambiente frenano anche la crescita del mercato.

Nonostante le sfide, il mercato dell'anidride ftalica promette molto per una serie di opportunità. L'aumento della domanda di PVC in settori come l'edilizia, i trasporti e l'imballaggio andrà a vantaggio dell'industria. Inoltre, l'emergere di bioplasticizzanti realizzati con biomateriali e senza ftalati apre nuove prospettive di espansione del settore. Anche il potenziale inutilizzato delle economie emergenti, in particolare quelle nella regione Asia-Pacifico e alimentate dalla rapida urbanizzazione e industrializzazione, ha un impatto sulle prospettive di crescita del mercato. Inoltre, i progressi tecnici e le iniziative di ricerca mirate a migliorare la sostenibilità e le prestazioni dei prodotti a base di anidride ftalica presentano prospettive di diversificazione ed espansione del mercato.

The pandemic had a significant impact on all industry participants as all factories, production lines, and other operations had to close. Worldwide halts and supply chain disruptions hampered production. Following the pandemic, governments continue to impose a number of restrictions, such as operating with only half the workforce and fewer hours, which impedes the market's cycle of production. Less demand from the automotive, electronics, paint & coating, and other related industries accounts for the losses. After the pandemic, the market is anticipated to rebound, with sectors aiming to finish the ongoing projects at higher production rates in order to make up for the losses already factored in.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2029 |

| Base year | 2021 |

| Estimated year | 2022 |

| Forecasted year | 2022-2029 |

| Historical period | 2018-2020 |

| Unit | Value (USD Billion), Value (Kilotons) |

| Segmentation | By process, By Application, By end-use industry, By Region |

| By Process |

|

| By Application |

|

| By End Use Industry |

|

| By Region |

|

Frequently Asked Questions

• What is the projected market size & growth rate of the phthalic anhydride market?

The phthalic anhydride market was valued at USD 3.99 billion in 2022 and is projected to reach USD 5.36 billion by 2029, growing at a CAGR of 4.3% from 2022 to 2029.

• What are the factors driving the phthalic anhydride market?

Growing usage of phthalic anhydride in the manufacturing of plasticizers and increasing consumption of alkyd resin in the paints and coatings industry are the key factors boosting the phthalic anhydride market growth.

• What are the top players operating in the phthalic anhydride market?

The major players in the phthalic anhydride market include LANXESS, Clariant, Avient Corporation, The Lubrizol Corporation, LG Chem, BASF SE, 3M, Dow, DuPont, and LSB INDUSTRIES.

• What segments are covered in the phthalic anhydride market report?

The global phthalic anhydride market is segmented on the basis of process, application, end-use industry, and geography.

• Which region held the largest share of the phthalic anhydride market in 2021?

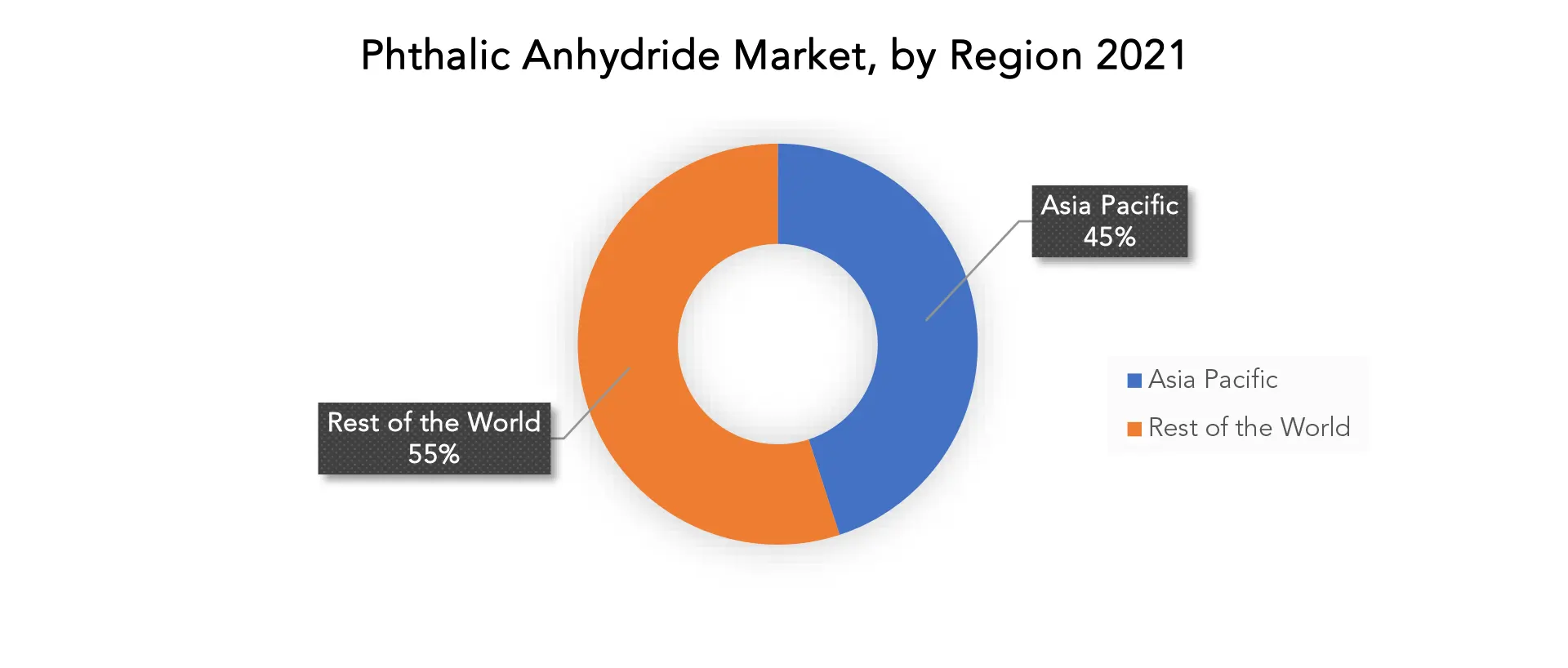

Asia-Pacific held the largest share of the phthalic anhydride market in 2021.

Phthalic Anhydride Market Segment Analysis

The phthalic anhydride market is segmented based on process, application, end-use industry, and region. By process, the market is segmented into O-Xylene catalytic oxidation and naphthalene catalytic oxidation. By application, the market is segmented into plasticizers, alkyd resins, unsaturated polyester resins, and others. By end-use industry, the market is segmented into paints & coatings, automotive, electrical & electronics, building & construction, agriculture, marine, and others.

In 2021, the o-xylene catalytic oxidation segment held a significant market share for phthalic anhydride due to the lower feed utilization and more expensive feedstock of the naphthalene catalytic oxidation process. Due to its liquid state, the o-xylene oxidation process allows for a simpler feed system than the naphthalene oxidation process, which is the main factor propelling the demand for the o-xylene process in the phthalic anhydride market during the forecast period.

Due to its extensive properties, including flexibility, bendability, and durability, which ensure its high performance for a longer tenure, the plasticizer segment accounted for a significant share of the phthalic anhydride market in 2021. Phthalic anhydride is increasingly in demand from the wire and cable, film and sheet, paint and coating, transportation, and medical industries.

The building and construction sector accounts for the largest revenue share in the global market in terms of end-user. Due to the wide range of PVC, UPR, and alkyd resin end users in various products, the construction industry is anticipated to be the largest market for phthalic anhydride.

[caption id="attachment_25699" align="aligncenter" width="1920"]

Phthalic Anhydride Market Players

The phthalic anhydride market key players include LANXESS, Clariant, Avient Corporation, The Lubrizol Corporation, LG Chem, BASF SE, 3M, Dow, DuPont, LSB INDUSTRIES, and others.

Recent Developments:- 22 May 2023: BASF’s Coatings division has launched a crowdsourcing digital tool to streamline and enhance color formula search for customers of its two paint brands, NORBIN and Shancai.

- 22 March 2023: BASF introduced a new Ultramid Deep Gloss grade, optimized for highly glossy automotive interior parts, and applied for the first time to the garnish of Toyota ‘s new Prius.

Who Should Buy? Or Key Stakeholders

- Manufacturers

- Chemical Industry

- End users companies

- Government organizations

- Research organizations

- Investment research firms

- Others

Phthalic Anhydride Market Regional Analysis

The phthalic anhydride market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).

- North America: includes the US, Canada, Mexico, Rest of North America

- Asia Pacific: includes China, Japan, South Korea, India, Australia, and Rest of APAC

- Europe: includes UK, Germany, France, Italy, Russia, Spain, and Rest of Europe

- South America: includes Brazil, Argentina, Colombia and Rest of South America

- Middle East & Africa: includes UAE, Saudi Arabia, South Africa, and Rest of MEA

Due to the significant increase in government spending on infrastructure development and the quick industrialization of nations like China and India, the Asia-Pacific region held a significant market share in 2021. The demand for phthalic anhydride in the area increased as a result. As phthalic anhydride is used as a raw material for the creation of finished goods, the demand for it is rising across a variety of end-user industries, including building & construction, automotive, paints & coatings, electrical & electronics, marine, and agriculture. Additionally, the region's expanding construction sector is anticipated to drive up demand for phthalic anhydride and create a high demand for PVC products.

During the anticipated time frame, North America is anticipated to display a steady demand for phthalic anhydride from the construction and renovation sector. However, due to the toxicity of phthalic anhydride, strict environmental regulations in Europe and North America are anticipated to restrict the market in some ways. Due to government initiatives to boost the tourism industry, the Middle East and Africa are likely to experience a moderate demand for phthalic anhydride from the expanding construction industry.

[caption id="attachment_25701" align="aligncenter" width="1920"]

Key Market Segments: Phthalic Anhydride Market

Phthalic Anhydride Market by process, 2020-2029, (USD Billion, Kilotons)- O-Xylene Catalytic Oxidation

- Naphthalene Catalytic Oxidation

- Plasticizers

- Alkyd Resins

- Unsaturated Polyester Resins

- Others

- Paints & Coatings

- Automotive

- Electrical & Electronics

- Building & Construction

- Agriculture

- Marine

- Others

- North America

- Asia Pacific

- Europe

- South America

- Middle East And Africa

Exactitude Consultancy Services Key Objectives

- Increasing sales and market share

- Developing new technology

- Improving profitability

- Entering new markets

- Enhancing brand reputation

Key Question Answered

- What is the expected growth rate of the phthalic anhydride market over the next 7 years?

- What are the end-user industries driving demand for the market and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-Pacific, the middle east, and Africa?

- How is the economic environment affecting the phthalic anhydride market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the phthalic anhydride market?

- What is the current and forecasted size and growth rate of the global phthalic anhydride market?

- What are the key drivers of growth in the phthalic anhydride market?

- Who are the major players in the market and what is their market share?

- What are the distribution channels and supply chain dynamics in the phthalic anhydride market?

- What are the technological advancements and innovations in the phthalic anhydride market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the phthalic anhydride market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the phthalic anhydride market?

- What are the service offerings and specifications of leading players in the market?

- What is the pricing trend of phthalic anhydride in the market and what is the impact of raw material prices on the price trend?

- INTRODUCTION

- MARKET DEFINITION

- MARKET SEGMENTATION

- RESEARCH TIMELINES

- ASSUMPTIONS AND LIMITATIONS

- RESEARCH METHODOLOGY

- DATA MINING

- SECONDARY RESEARCH

- PRIMARY RESEARCH

- SUBJECT-MATTER EXPERTS’ ADVICE

- QUALITY CHECKS

- FINAL REVIEW

- DATA TRIANGULATION

- BOTTOM-UP APPROACH

- TOP-DOWN APPROACH

- RESEARCH FLOW

- DATA SOURCES

- DATA MINING

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- GLOBAL PHTHALIC ANHYDRIDE MARKET OUTLOOK

- MARKET DRIVERS

- MARKET RESTRAINTS

- MARKET OPPORTUNITIES

- IMPACT OF COVID-19 ON THE PHTHALIC ANHYDRIDE MARKET

- PORTER’S FIVE FORCES MODEL

- THREAT FROM NEW ENTRANTS

- THREAT FROM SUBSTITUTES

- BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER OF CUSTOMERS

- DEGREE OF COMPETITION

- INDUSTRY VALUE CHAIN ANALYSIS

- GLOBAL PHTHALIC ANHYDRIDE MARKET OUTLOOK

- GLOBAL PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION, KILOTONS), 2020-2029

- O-XYLENE CATALYTIC OXIDATION

- NAPHTHALENE CATALYTIC OXIDATION

- GLOBAL PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION, KILOTONS),2020-2029

- PLASTICIZERS

- ALKYD RESINS

- UNSATURATED POLYESTER RESINS

- OTHERS

- GLOBAL PHTHALIC ANHYDRIDE MARKET BY END-USE INDUSTRY (USD BILLION, KILOTONS),2020-2029

- PAINTS & COATINGS

- AUTOMOTIVE

- ELECTRICAL & ELECTRONICS

- BUILDING & CONSTRUCTION

- AGRICULTURE

- MARINE

- OTHERS

- GLOBAL PHTHALIC ANHYDRIDE MARKET BY REGION (USD BILLION, KILOTONS),2020-2029

- NORTH AMERICA

- US

- CANADA

- MEXICO

- REST OF NORTH AMERICA

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

- COMPANY PROFILES*

(BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCTS OFFERED, RECENT DEVELOPMENTS)

- LANXESS

- CLARIANT

- AVIENT CORPORATION

- THE LUBRIZOL CORPORATION

- LG CHEM

- BASF SE

- 3M

- DOW

- DUPONT

- LSB INDUSTRIES

*THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 2 GLOBAL PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 3 GLOBAL PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 4 GLOBAL PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 5 GLOBAL PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 6 GLOBAL PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 7 GLOBAL PHTHALIC ANHYDRIDE MARKET BY REGION (USD BILLION), 2020-2029

TABLE 8 GLOBAL PHTHALIC ANHYDRIDE MARKET BY REGION (KILOTONS), 2020-2029

TABLE 9 NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 10 NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 11 NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 12 NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 13 NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 14 NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 15 NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 16 NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY COUNTRY (KILOTONS), 2020-2029

TABLE 17 US PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 18 US PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 19 US PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 20 US PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 21 US PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 22 US PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 23 CANADA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 24 CANADA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 25 CANADA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 26 CANADA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 27 CANADA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 28 CANADA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 29 MEXICO PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 30 MEXICO PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 31 MEXICO PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 32 MEXICO PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 33 MEXICO PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 34 MEXICO PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 35 REST OF NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 36 REST OF NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 37 REST OF NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 38 REST OF NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 39 REST OF NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 40 REST OF NORTH AMERICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 41 SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 42 SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 43 SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 44 SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 45 SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 46 SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 47 SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 48 SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY COUNTRY (KILOTONS), 2020-2029

TABLE 49 BRAZIL PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 50 BRAZIL PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 51 BRAZIL PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 52 BRAZIL PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 53 BRAZIL PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 54 BRAZIL PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 55 ARGENTINA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 56 ARGENTINA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 57 ARGENTINA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 58 ARGENTINA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 59 ARGENTINA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 60 ARGENTINA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 61 COLOMBIA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 62 COLOMBIA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 63 COLOMBIA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 64 COLOMBIA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 65 COLOMBIA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 66 COLOMBIA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 67 REST OF SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 68 REST OF SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 69 REST OF SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 70 REST OF SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 71 REST OF SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 72 REST OF SOUTH AMERICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 73 ASIA -PACIFIC PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 74 ASIA -PACIFIC PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 75 ASIA -PACIFIC PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 76 ASIA -PACIFIC PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 77 ASIA -PACIFIC PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 78 ASIA -PACIFIC PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 79 ASIA -PACIFIC PHTHALIC ANHYDRIDE MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 80 ASIA -PACIFIC PHTHALIC ANHYDRIDE MARKET BY COUNTRY (KILOTONS), 2020-2029

TABLE 81 INDIA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 82 INDIA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 83 INDIA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 84 INDIA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 85 INDIA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 86 INDIA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 87 CHINA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 88 CHINA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 89 CHINA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 90 CHINA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 91 CHINA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 92 CHINA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 93 JAPAN PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 94 JAPAN PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 95 JAPAN PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 96 JAPAN PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 97 JAPAN PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 98 JAPAN PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 99 SOUTH KOREA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 100 SOUTH KOREA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 101 SOUTH KOREA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 102 SOUTH KOREA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 103 SOUTH KOREA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 104 SOUTH KOREA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 105 AUSTRALIA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 106 AUSTRALIA PHTHALIC ANHYDRIDE MARKET BY APPLICATIONBY PROCESS (KILOTONS), 2020-2029

TABLE 107 AUSTRALIA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 108 AUSTRALIA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 109 AUSTRALIA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 110 AUSTRALIA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 111 REST OF ASIA PACIFIC PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 112 REST OF ASIA PACIFIC PHTHALIC ANHYDRIDE MARKET BY APPLICATIONBY PROCESS (KILOTONS), 2020-2029

TABLE 113 REST OF ASIA PACIFIC PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 114 REST OF ASIA PACIFIC PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 115 REST OF ASIA PACIFIC PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 116 REST OF ASIA PACIFIC PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 117 EUROPE PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 118 EUROPE PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 119 EUROPE PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 120 EUROPE PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 121 EUROPE PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 122 EUROPE PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 123 EUROPE PHTHALIC ANHYDRIDE MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 124 EUROPE PHTHALIC ANHYDRIDE MARKET BY COUNTRY (KILOTONS), 2020-2029

TABLE 125 GERMANY PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 126 GERMANY PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 127 GERMANY PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 128 GERMANY PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 129 GERMANY PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 130 GERMANY PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 131 UK PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 132 UK PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 133 UK PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 134 UK PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 135 UK PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 136 UK PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD KILOTONS), 2020-2029

TABLE 137 FRANCE PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 138 FRANCE PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 139 FRANCE PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 140 FRANCE PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 141 FRANCE PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 142 FRANCE PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 143 ITALY PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 144 ITALY PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 145 ITALY PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 146 ITALY PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 147 ITALY PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 148 ITALY PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 149 SPAIN PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 150 SPAIN PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 151 SPAIN PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 152 SPAIN PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 153 SPAIN PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 154 SPAIN PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 155 RUSSIA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 156 RUSSIA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 157 RUSSIA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 158 RUSSIA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 159 RUSSIA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 160 RUSSIA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 161 REST OF EUROPE PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 162 REST OF EUROPE PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 163 REST OF EUROPE PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 164 REST OF EUROPE PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 165 REST OF EUROPE PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 166 REST OF EUROPE PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 167 MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 168 MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 169 MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 170 MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 171 MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 172 MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 173 MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 174 MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY COUNTRY (KILOTONS), 2020-2029

TABLE 175 UAE PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 176 UAE PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 177 UAE PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 178 UAE PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 179 UAE PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 180 UAE PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 181 SAUDI ARABIA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 182 SAUDI ARABIA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 183 SAUDI ARABIA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 184 SAUDI ARABIA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 185 SAUDI ARABIA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 186 SAUDI ARABIA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 187 SOUTH AFRICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 188 SOUTH AFRICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 189 SOUTH AFRICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 190 SOUTH AFRICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 191 SOUTH AFRICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 192 SOUTH AFRICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

TABLE 193 REST OF MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (USD BILLION), 2020-2029

TABLE 194 REST OF MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY PROCESS (KILOTONS), 2020-2029

TABLE 195 REST OF MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 196 REST OF MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY APPLICATION (KILOTONS), 2020-2029

TABLE 197 REST OF MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (USD BILLION), 2020-2029

TABLE 198 REST OF MIDDLE EAST AND AFRICA PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY (KILOTONS), 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL PHTHALIC ANHYDRIDE MARKET BY PROCESS, USD BILLION, KILOTONS, 2020-2029

FIGURE 9 GLOBAL PHTHALIC ANHYDRIDE MARKET BY APPLICATION, USD BILLION, KILOTONS, 2020-2029

FIGURE 10 GLOBAL PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY, USD BILLION, KILOTONS, 2020-2029

FIGURE 11 GLOBAL PHTHALIC ANHYDRIDE MARKET BY REGION, USD BILLION, KILOTONS, 2020-2029

FIGURE 12 PORTER’S FIVE FORCES MODEL

FIGURE 13 GLOBAL PHTHALIC ANHYDRIDE MARKET BY PROCESS, USD BILLION, 2021

FIGURE 14 GLOBAL PHTHALIC ANHYDRIDE MARKET BY APPLICATION, USD BILLION, 2021

FIGURE 15 GLOBAL PHTHALIC ANHYDRIDE MARKET BY END USE INDUSTRY, USD BILLION, 2021

FIGURE 16 GLOBAL PHTHALIC ANHYDRIDE MARKET BY REGION, USD BILLION, 2021

FIGURE 17 MARKET SHARE ANALYSIS

FIGURE 18 LANXESS: COMPANY SNAPSHOT

FIGURE 19 CLARIANT: COMPANY SNAPSHOT

FIGURE 20 AVIENT CORPORATION: COMPANY SNAPSHOT

FIGURE 21 THE LUBRIZOL CORPORATION: COMPANY SNAPSHOT

FIGURE 22 LG CHEM: COMPANY SNAPSHOT

FIGURE 23 BASF SE.: COMPANY SNAPSHOT

FIGURE 24 3M: COMPANY SNAPSHOT

FIGURE 25 DOW: COMPANY SNAPSHOT

FIGURE 26 DUPONT: COMPANY SNAPSHOT

FIGURE 27 LSB INDUSTRIES: COMPANY SNAPSHOT

DOWNLOAD FREE SAMPLE REPORT

License Type

SPEAK WITH OUR ANALYST

Want to know more about the report or any specific requirement?

WANT TO CUSTOMIZE THE REPORT?

Our Clients Speak

We asked them to research ‘ Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te

Yosuke Mitsui

Senior Associate Construction Equipment Sales & Marketing

We asked them to research ‘Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te