Base Year Value ()

x.x %

x.x %

CAGR ()

x.x %

x.x %

Forecast Year Value ()

x.x %

x.x %

Historical Data Period

Largest Region

Forecast Period

軟磁性材料市場:タイプ別(ソフトフェライト、電磁鋼、コバルト)、用途別(モーター、変圧器、オルタネーター)、最終用途別(自動車、電子機器・通信、電気)および地域別、2023年から2029年までの世界的な動向と予測

Instant access to hundreds of data points and trends

- Market estimates from 2014-2029

- Competitive analysis, industry segmentation, financial benchmarks

- Incorporates SWOT, Porter's Five Forces and risk management frameworks

- PDF report or online database with Word, Excel and PowerPoint export options

- 100% money back guarantee

軟磁性材料市場の概要

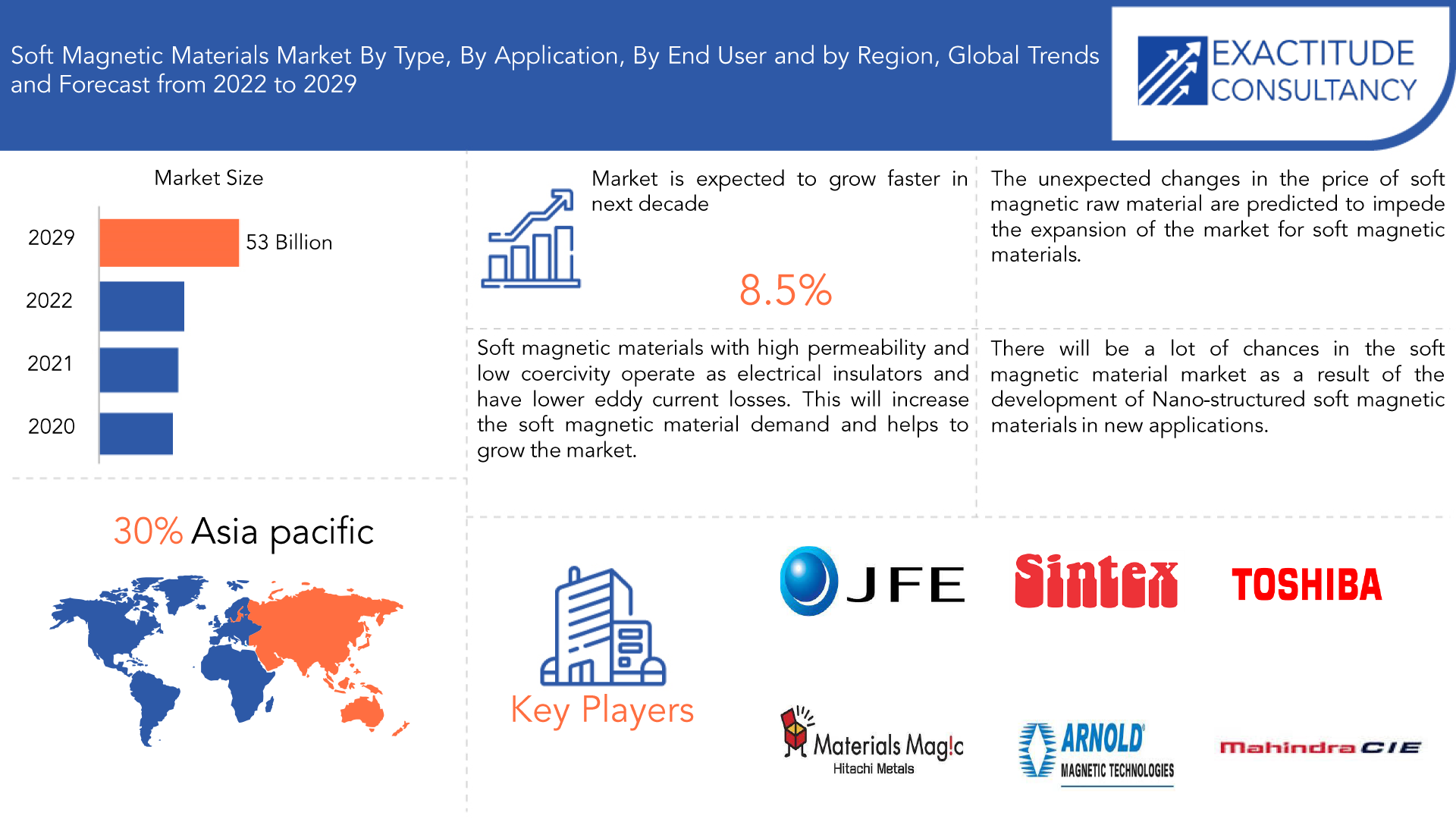

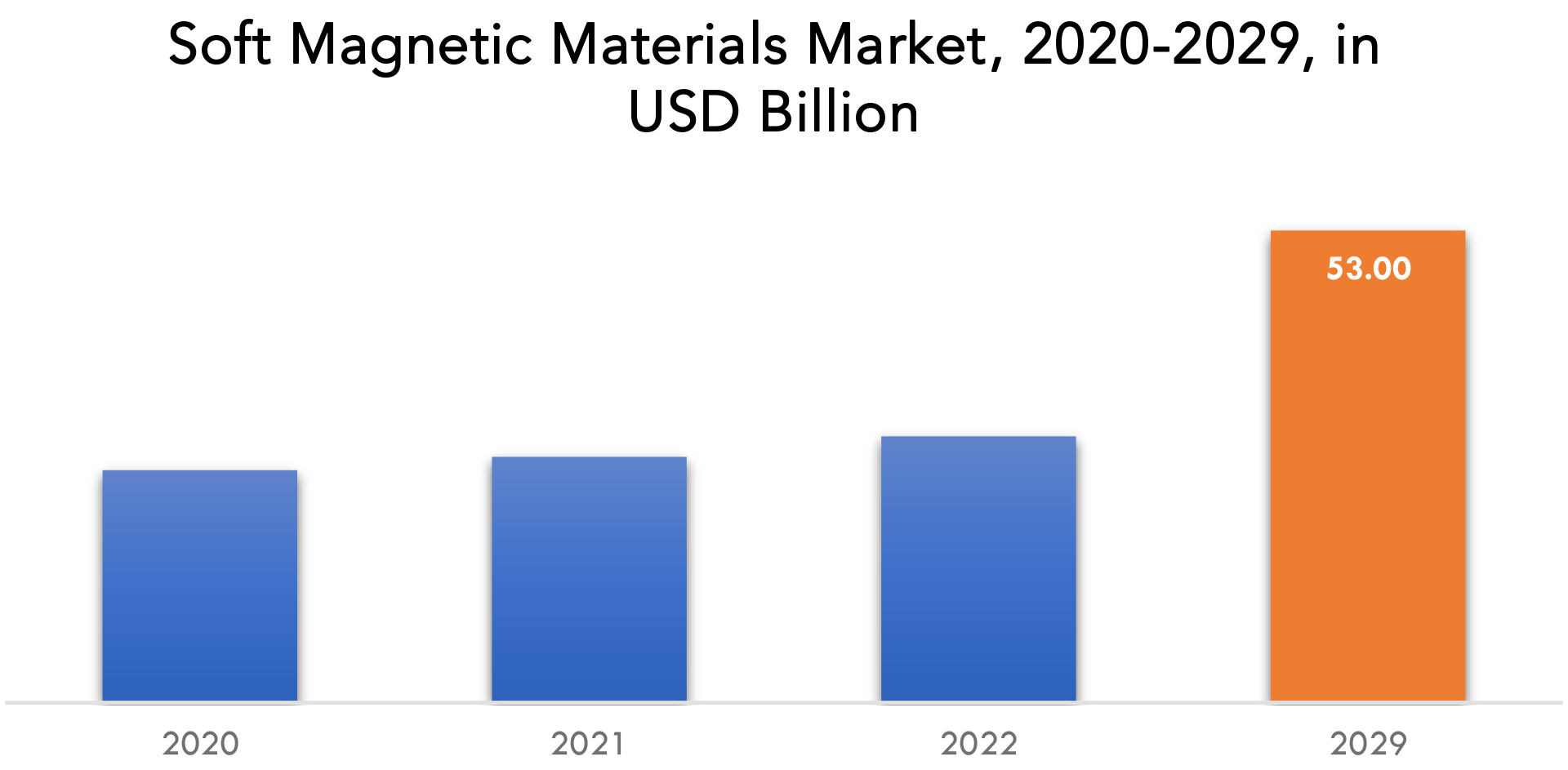

軟磁性材料市場は、2020年から2029年にかけて8.5%のCAGRで成長すると予想されています。2020年の261億米ドルから2029年には530億米ドルを超えると予想されています。

私たちが日常的に使っているものの多くには、軟磁性材料が使われています。電子用鉄、シリコン鋼、ソフトフェライトなど、伝統的な軟磁性材料は、1世紀以上、あるいはほぼ1世紀にわたって利用されてきました。アモルファス合金やナノ結晶合金などの最新の軟磁性材料でさえ、40年以上前から生産されています。製造プロセスと合金の組成は継続的に改善されてきました。たとえば、1.7 T、50 Hzでのコア損失は1.2 W/kgから0.7 W/kgに減少し、シリコン鋼の厚さは0.30 mmから0.23 mmに減少しました。シートの厚さをさらに32 mmに減らすと、コア損失は0.21 W/kgに低下します。

軟磁性材料は、磁化曲線が急峻に上昇し、ヒステリシス ループが小さく狭いため、磁化サイクルごとのエネルギー損失が低い材料です。軟磁性材料は、モーター巻線によって生成される磁場を改善するため、モーター用途でよく使用されます。さらに、鉄シリコン合金や鉄コバルト合金などの鉄ベースの材料は、モーター用途で主に使用されています。現在、モーター部品は主に粉末冶金技術を使用して製造されています。軟磁性材料は渦電流損失を減らし、モーターの効率を高めます。

磁場、電流、変位、機械的応力を測定する機能部品には、軟磁性材料が含まれます。高飽和磁化、最小保磁力、小さなヒステリシス損失、最大の透磁率など、軟磁性材料はさまざまな特徴を備えています。世界中の変圧器、インダクタ、モーター、発電機の磁気コアに使用されています。純鉄、シリコン鉄合金、ニッケル鉄合金は、よく使用される軟磁性材料の一部です。

Due to advantages including minimal noise, compact design, and energy savings, soft magnetic materials are typically utilized in electric motors, which are commonly seen in electric vehicles. Moreover, brushless DC motors, stepper motors, brushed DC motors, switch reluctance motors, claw pole motors, transformers, and alternators all frequently employ soft magnetic materials in their stators. Soft magnetic materials with high permeability and low coercivity operate as electrical insulators and have lower eddy current losses. They also have high electrical resistivity to iron. This will likely result in a significant increase in soft magnetic material demand, which will propel the market for these materials to expand.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2029 |

| Base year | 2021 |

| Estimated year | 2022 |

| Forecasted year | 2022-2029 |

| Historical period | 2018-2020 |

| Unit | Value (USD BILLION) |

| Segmentation | By Type, By Application, By End-User, By Region |

| By Type |

|

| By Application |

|

| By End-User |

|

| By Region |

|

Iron, nickel, and/or cobalt are the principal metals in amorphous alloys, together with boron, carbon, phosphorus, or silicon. Industrial users are using magnetic components made from amorphous alloys to run processes more effectively, save energy, and save operating costs. Amorphous soft magnetic materials are ideal for the majority of electrical and electronic applications due to important characteristics like lower core losses at higher frequencies, higher & wide range of permeability, increased operational temperatures, low coercive field, core weight & volume reduction ability, excellent corrosion resistance, versatility, good mechanical strength, flux density, and various hysteresis loops, among others. It would fuel the expansion of this market even further.

To get a competitive edge, the main corporations are typically refocusing their efforts on creating new and inventive goods and expanding their production capabilities in the market for soft magnetic materials. There will be a lot of chances in the soft magnetic material market as a result of the development of nano-structured soft magnetic materials in new applications. The growing investments by major market players further offer the numerous growth opportunities within the market.

The unexpected changes in the price of soft magnetic raw material are predicted to impede the expansion of the market for soft magnetic materials. As a result, it hampered the flow of soft magnetic raw materials and presented difficulties for producers. The prices of iron ore saw a substantial decline 2019, due to the seasonal decline in superalloy demand and the recovery of supply by iron ore majors restrain for the market growth.

需要と供給の面では、COVID-19パンデミックの流行は、軟磁性材料を含む多くの市場に悪影響を及ぼしています。パンデミックの結果、人工呼吸器などの医療機器の需要が増加し、最適な制御、調整された気流、高いトルク密度、低騒音のモーターの必要性が高まっています。コロナウイルスによって引き起こされた世界中の患者の増加により、人工呼吸器の需要が高まっており、モーターの需要が高まり、最終的には軟磁性材料市場の拡大を促進する可能性があります。COVID-19は、生産と需要に直接影響を与えること、サプライチェーンと市場の混乱を引き起こすこと、企業と金融市場への経済的影響という3つの方法で世界経済に影響を与える可能性があります。

[キャプション id="attachment_17072" align="aligncenter" width="1920"]

Frequently Asked Questions

• What is the worth of soft magnetic materials market?

The soft magnetic materials market is expected to grow at 8.5% CAGR from 2020 to 2029. It is expected to reach above USD 53 billion by 2029 from USD 26.1 billion in 2020.

• What is the size of the Asia pacific soft magnetic materials industry?

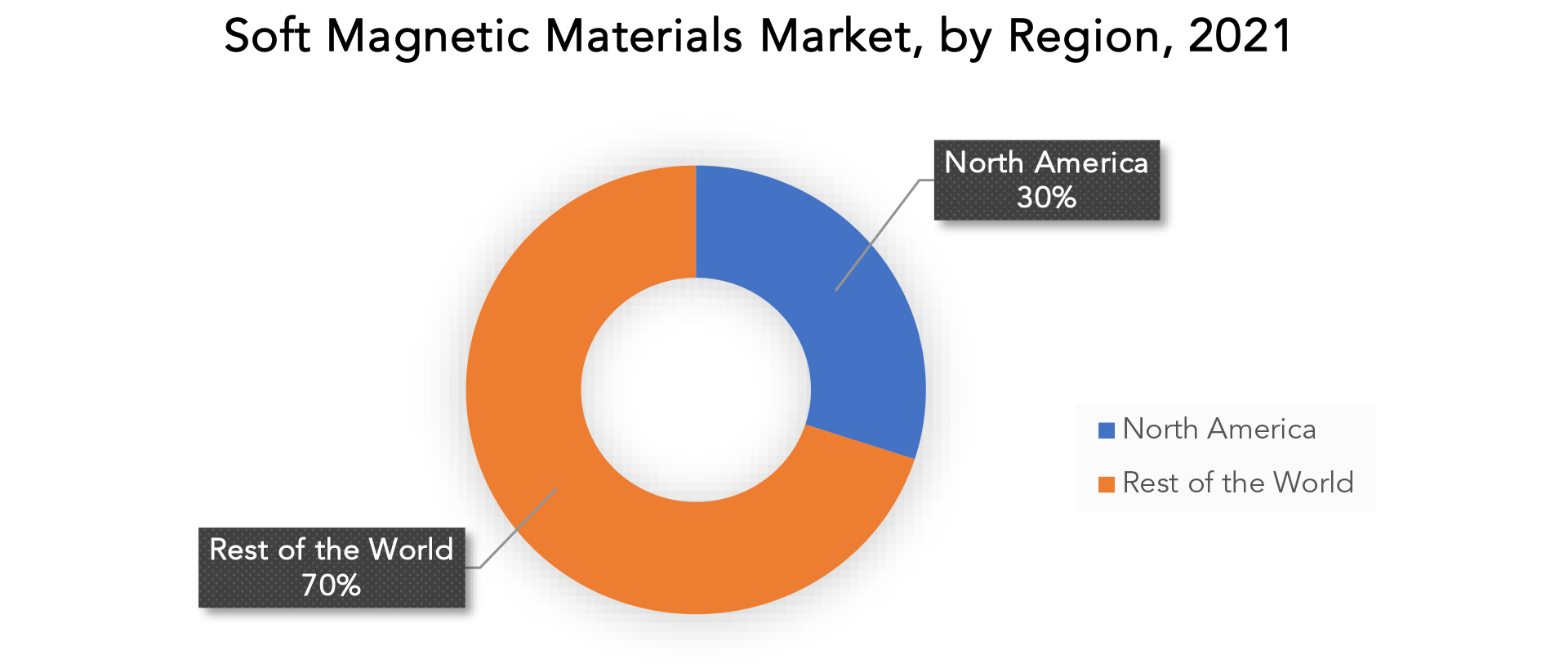

Asia Pacific held more than 30 % of the soft magnetic materials market revenue share in 2021 and will witness expansion in the forecast period.

• What are some of the market's driving forces?

Due to advantages including minimal noise, compact design, and energy savings, soft magnetic materials are typically utilized in electric motors, which are commonly seen in electric vehicles. Moreover, brushless DC motors, stepper motors, brushed DC motors, switch reluctance motors, claw pole motors, transformers, and alternators all frequently employ soft magnetic materials in their stators. Soft magnetic materials with high permeability and low coercivity operate as electrical insulators and have lower eddy current losses. They also have high electrical resistivity to iron. This will likely result in a significant increase in soft magnetic material demand, which will propel the market for these materials to expand.

• Which are the top companies to hold the market share in soft magnetic materials market?

The soft magnetic materials market key players Hitachi Metals.ltd, Toshiba Materials, GKN Sinter Metals inc, Sintex, Mate Co.Ltd, JFE Steel Group, Mahindra CIE, Meyer Sintermetal AG, Arnold Magnetic Technologies.

• What is the leading type of soft magnetic materials market?

Based on type, the electric steel market captured a sizable portion. Electric steel decreases magnetic losses while also providing electrical insulation, high permeability, low coercivity, and high electrical resistivity to iron. It is utilized in a variety of devices, including inductors, motors, generators, and electrical power transformers. Moreover, it provides a small hysteresis area that eventually results in decreased eddy current loss, boosting the application's effectiveness. Electric steel is widely used in a variety of applications due to its beneficial qualities, which is causing its utilization to rise rapidly and fostering the expansion of the market as a whole.

• Which is the largest regional market for soft magnetic materials market?

Asia Pacific held 30% of the overall market share of soft magnetic materials. Due to the presence of iron ore mining, the market for soft magnetic materials in the world was dominated by the Asia-Pacific region. The biggest producers and consumers in the Asia-Pacific region are underdeveloped nations like China and India. Manufacturers of soft magnetic materials from North American and European nations are motivated to invest in the Asia-Pacific region by the availability of cheap labor and the desire to pursue new market niches. The Asia-Pacific region's countries are experiencing robust industrialization, and this region's geographic advantages—such as the presence of iron mines in China and India—are what are driving the market for soft magnetic materials there.

Soft Magnetic Materials Market Segment Analysis

The soft magnetic materials market is segmented based on type, applications, end-use and region.

By type (soft ferrite, electrical steel, cobalt), by applications (motor, transformer, alternator), by end-use (automotive, electronics & telecommunication, electrical) and region.

Based on type, the electric steel market captured a sizable portion. Electric steel decreases magnetic losses while also providing electrical insulation, high permeability, low coercivity, and high electrical resistivity to iron. It is utilized in a variety of devices, including inductors, motors, generators, and electrical power transformers. Moreover, it provides a small hysteresis area that eventually results in decreased eddy current loss, boosting the application's effectiveness. Electric steel is widely used in a variety of applications due to its beneficial qualities, which is causing its utilization to rise rapidly and fostering the expansion of the market as a whole.

Based on Applications, the majority of revenues more than 50% were generated by electric motors. Several end-use industries, including electric transmission, consumer electronics, electric vehicles, and medical equipment, use electric motors. The soft magnetic material market's second-leading application sector is transformers, where soft magnetic materials are used in transformer cores. Expansion in the transformer sector, which is evident from numerous investments, is anticipated to accelerate market growth.

Based on end use, the electrical and electronics industry held a sizable market share for soft magnetic materials. This resulted from a significant demand for soft magnetic materials in the electricity-generating industry's key power transmission components. Nonetheless, given the industry's transition from a fossil fuel to an electric eco-system, the automobile sector is expected to show positive growth.

[caption id="attachment_17091" align="aligncenter" width="1920"]

Soft Magnetic Materials Market Players

The Soft Magnetic Materials market key players Hitachi Metals.ltd, Toshiba Materials, GKN Sinter Metals inc, Sintex, Mate Co.Ltd, JFE Steel Group, Mahindra CIE, Meyer Sintermetal AG, Arnold Magnetic Technologies.

06-02-2023: - JFE Steel Corporation, which is expanding the electrical steel sheet capacity of its West Japan Works (Kurashiki Area) for startup targeted at the first half of the fiscal year starting in April 2024, announced today that it is now planning an additional expansion targeted at a startup in the fiscal year beginning April 2026

21-12-2022: - JFE Steel Corporation today announced that together with IHI Corporation it will conduct a demonstration test of an automated transport system using retrofitted vehicles at its East Japan Works (Keihin District) from February 2023, aiming to test all sections of the demonstration route within the fiscal year ending in March 2024.

Who Should Buy? Or Key Stakeholders

- Soft magnetic materials Suppliers

- Manufacturing

- Construction

- Auto sector

- Investors

- Others

Soft Magnetic Materials Market Regional Analysis

The Soft Magnetic Materials market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).

- North America: includes the US, Canada, Mexico

- Asia Pacific: includes China, Japan, South Korea, India, Australia, ASEAN and Rest of APAC

- Europe: includes UK, Germany, France, Italy, Spain, Russia, and Rest of Europe

- South America: includes Brazil, Argentina and Rest of South America

- Middle East & Africa: includes Turkey, UAE, Saudi Arabia, South Africa, and Rest of MEA

Asia Pacific held 30% of the overall market share of soft magnetic materials. Due to the presence of iron ore mining, the market for soft magnetic materials in the world was dominated by the Asia-Pacific region. The biggest producers and consumers in the Asia-Pacific region are underdeveloped nations like China and India. Manufacturers of soft magnetic materials from North American and European nations are motivated to invest in the Asia-Pacific region by the availability of cheap labor and the desire to pursue new market niches. The Asia-Pacific region's countries are experiencing robust industrialization, and this region's geographic advantages—such as the presence of iron mines in China and India—are what are driving the market for soft magnetic materials there.

The second-largest regional category, with a revenue share of more than 15.0%, was North America. The U.S. is the primary source of the growth. Electric motors, which are widely employed in many industrial applications like pumping, compressed air, fans, refrigeration, material processing, and handling, are heavily consumed in the nation. Despite a decline in industrial production in 2019 that was prolonged by COVID-19, there was some relief for the nation in May 2020 as some industries, including consumer goods, business equipment, transit equipment, defense and space equipment, and construction supplies, reported gains as they partially resumed operations. Over the projection period, it is anticipated that rising industrial activity would fuel demand for electric motors and ultimately soft magnetic materials.

[caption id="attachment_17100" align="aligncenter" width="1920"]

Key Market Segments: Soft Magnetic Materials Market

Soft Magnetic Materials Market By Type, 2020-2029, (USD Billion) (Tons)- Soft Ferrite

- Electrical Steel

- Cobalt

- Motor

- Transformer

- Alternator

- Automotive

- Electronics & Telecommunication

- Electrical

- North America

- Asia Pacific

- Europe

- South America

- Middle East And Africa

Exactitude Consultancy Services Key Objectives:

- Increasing sales and market share

- Developing new technology

- Improving profitability

- Entering new markets

- Enhancing brand reputation

Key Question Answered

- What is the expected growth rate of the soft magnetic materials market over the next 7 years?

- Who are the major players in the soft magnetic materials market and what is their market share?

- What are the end-user industries driving demand for market and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-Pacific, Middle East, and Africa?

- How is the economic environment affecting the soft magnetic materials market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the soft magnetic materials market?

- What is the current and forecasted size and growth rate of the global soft magnetic materials market?

- What are the key drivers of growth in the soft magnetic materials market?

- Who are the major players in the market and what is their market share?

- What are the distribution channels and supply chain dynamics in the soft magnetic materials market?

- What are the technological advancements and innovations in the soft magnetic materials market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the soft magnetic materials market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the soft magnetic materials market?

- What are the service offerings and specifications of leading players in the market?

- What is the pricing trend of Soft Magnetic Materials in the market and what is the impact of raw material prices on the price trend?

- 導入

- 市場の定義

- 市場セグメンテーション

- 研究タイムライン

- 前提と制限

- 研究方法

- データマイニング

- 二次調査

- 一次研究

- 専門家のアドバイス

- 品質チェック

- 最終レビュー

- データの三角測量

- ボトムアップアプローチ

- トップダウンアプローチ

- 研究の流れ

- データソース

- データマイニング

- エグゼクティブサマリー

- 市場概要

- 世界の軟磁性材料の展望

- 市場の推進要因

- 市場の制約

- 市場機会

- 軟磁性材料市場へのCOVID-19の影響

- ポーターの5つの力モデル

- 新規参入者からの脅威

- 代替品の脅威

- サプライヤーの交渉力

- 顧客の交渉力

- 競争の度合い

- 業界バリューチェーン分析

- 世界の軟磁性材料の展望

- 世界の軟磁性材料市場(タイプ別、10億米ドル、トン)2020-2029年

- ソフトフェライト

- 電気鋼

- コバルト

- 世界の軟磁性材料市場(用途別、10億米ドル、トン)2020-2029年

- モーター

- トランス

- オルタネーター

- 世界の軟磁性材料市場 最終用途別(10億米ドル) (トン) 2020-2029

- 自動車

- エレクトロニクスと通信

- 電気

- 世界の軟磁性材料市場 地域別(10億米ドル) (トン) 2020-2029

- 北米

- 私たち

- カナダ

- メキシコ

- 南アメリカ

- ブラジル

- アルゼンチン

- コロンビア

- 南米のその他の地域

- ヨーロッパ

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他のヨーロッパ

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- オーストラリア

- 東南アジア

- その他のアジア太平洋地域

- 中東およびアフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東およびアフリカ

- 北米

- 企業プロフィール*

(事業概要、会社概要、提供製品、最近の動向)

- 日立金属株式会社

- 東芝マテリアル

- GKNシンターメタルズ

- シンテックス

- メイト株式会社

- JFEスチールグループ

- マヒンドラCIE

- マイヤーシンターメタルAG

- アーノルドマグネティックテクノロジーズ

*企業リストは参考です

表のリスト

TABLE 1 GLOBAL SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 2 GLOBAL SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 3 GLOBAL SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 4 GLOBAL SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 5 GLOBAL SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 6 GLOBAL SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 7 GLOBAL SOFT MAGNETIC MATERIALS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 8 GLOBAL SOFT MAGNETIC MATERIALS MARKET BY REGION (TONS) 2020-2029

TABLE 9 NORTH AMERICA SOFT MAGNETIC MATERIALS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 10 NORTH AMERICA SOFT MAGNETIC MATERIALS MARKET BY COUNTRY (TONS) 2020-2029

TABLE 11 US SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 12 US SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 13 US SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 14 US SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 15 US SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 16 US SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 17 CANADA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 18 CANADA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 19 CANADA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 20 CANADA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 21 CANADA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 22 CANADA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 23 MEXICO SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 24 MEXICO SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 25 MEXICO SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 26 MEXICO SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 27 MEXICO SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 28 MEXICO SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 29 SOUTH AMERICA SOFT MAGNETIC MATERIALS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 30 SOUTH AMERICA SOFT MAGNETIC MATERIALS MARKET BY COUNTRY (TONS) 2020-2029

TABLE 31 BRAZIL SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 32 BRAZIL SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 33 BRAZIL SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 34 BRAZIL SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 35 BRAZIL SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 36 BRAZIL SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 37 ARGENTINA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 38 ARGENTINA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 39 ARGENTINA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 40 ARGENTINA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 41 ARGENTINA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 42 ARGENTINA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 43 COLOMBIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 44 COLOMBIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 45 COLOMBIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 46 COLOMBIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 47 COLOMBIA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 48 COLOMBIA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 49 REST OF SOUTH AMERICA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 50 REST OF SOUTH AMERICA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 51 REST OF SOUTH AMERICA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 52 REST OF SOUTH AMERICA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 53 REST OF SOUTH AMERICA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 54 REST OF SOUTH AMERICA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 55 ASIA-PACIFIC SOFT MAGNETIC MATERIALS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 56 ASIA-PACIFIC SOFT MAGNETIC MATERIALS MARKET BY COUNTRY (TONS) 2020-2029

TABLE 57 INDIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 58 INDIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 59 INDIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 60 INDIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 61 INDIA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 62 INDIA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 63 CHINA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 64 CHINA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 65 CHINA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 66 CHINA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 67 CHINA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 68 CHINA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 69 JAPAN SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 70 JAPAN SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 71 JAPAN SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 72 JAPAN SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 73 JAPAN SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 74 JAPAN SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 75 SOUTH KOREA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 76 SOUTH KOREA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 77 SOUTH KOREA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 78 SOUTH KOREA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 79 SOUTH KOREA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 80 SOUTH KOREA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 81 AUSTRALIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 82 AUSTRALIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 83 AUSTRALIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 84 AUSTRALIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 85 AUSTRALIA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 86 AUSTRALIA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 87 SOUTH-EAST ASIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 88 SOUTH-EAST ASIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 89 SOUTH-EAST ASIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 90 SOUTH-EAST ASIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 91 SOUTH-EAST ASIA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 92 SOUTH-EAST ASIA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 93 REST OF ASIA PACIFIC SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 94 REST OF ASIA PACIFIC SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 95 REST OF ASIA PACIFIC SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 96 REST OF ASIA PACIFIC SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 97 REST OF ASIA PACIFIC SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 98 REST OF ASIA PACIFIC SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 99 EUROPE SOFT MAGNETIC MATERIALS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 100 EUROPE SOFT MAGNETIC MATERIALS MARKET BY COUNTRY (TONS) 2020-2029

TABLE 101 GERMANY SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 102 GERMANY SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 103 GERMANY SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 104 GERMANY SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 105 GERMANY SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 106 GERMANY SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 107 UK SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 108 UK SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 109 UK SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 110 UK SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 111 UK SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 112 UK SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 113 FRANCE SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 114 FRANCE SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 115 FRANCE SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 116 FRANCE SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 117 FRANCE SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 118 FRANCE SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 119 ITALY SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 120 ITALY SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 121 ITALY SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 122 ITALY SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 123 ITALY SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 124 ITALY SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 125 SPAIN SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 126 SPAIN SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 127 SPAIN SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 128 SPAIN SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 129 SPAIN SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 130 SPAIN SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 131 RUSSIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 132 RUSSIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 133 RUSSIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 134 RUSSIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 135 RUSSIA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 136 RUSSIA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 137 REST OF EUROPE SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 138 REST OF EUROPE SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 139 REST OF EUROPE SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 140 REST OF EUROPE SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 141 REST OF EUROPE SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 142 REST OF EUROPE SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 143 MIDDLE EAST AND AFRICA SOFT MAGNETIC MATERIALS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 144 MIDDLE EAST AND AFRICA SOFT MAGNETIC MATERIALS MARKET BY COUNTRY (TONS) 2020-2029

TABLE 145 UAE SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 146 UAE SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 147 UAE SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 148 UAE SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 149 UAE SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 150 UAE SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 151 SAUDI ARABIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 152 SAUDI ARABIA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 153 SAUDI ARABIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 154 SAUDI ARABIA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 155 SAUDI ARABIA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 156 SAUDI ARABIA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 157 SOUTH AFRICA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 158 SOUTH AFRICA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020-2029

TABLE 159 SOUTH AFRICA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 160 SOUTH AFRICA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 161 SOUTH AFRICA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 162 SOUTH AFRICA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 163 REST OF MIDDLE EAST AND AFRICA SOFT MAGNETIC MATERIALS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 164 REST OF MIDDLE EAST AND AFRICA SOFT MAGNETIC MATERIALS MARKET BY TYPE (TONS) 2020- 2029

TABLE 165 REST OF MIDDLE EAST AND AFRICA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 166 REST OF MIDDLE EAST AND AFRICA SOFT MAGNETIC MATERIALS MARKET BY APPLICATION (TONS) 2020-2029

TABLE 167 REST OF MIDDLE EAST AND AFRICA SOFT MAGNETIC MATERIALS MARKET BY END USER (USD BILLION) 2020-2029

TABLE 168 REST OF MIDDLE EAST AND AFRICA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

TABLE 169 REST OF MIDDLE EAST AND AFRICA SOFT MAGNETIC MATERIALS MARKET BY END USER (TONS) 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL SOFT MAGNETIC MATERIALS BY TYPE, USD BILLION, 2020-2029

FIGURE 9 GLOBAL SOFT MAGNETIC MATERIALS BY END USER, USD BILLION, 2020-2029

FIGURE 10 GLOBAL SOFT MAGNETIC MATERIALS BY APPLICATION USD BILLION, 2020-2029

FIGURE 11 GLOBAL SOFT MAGNETIC MATERIALS BY REGION, USD BILLION, 2020-2029

FIGURE 12 GLOBAL SOFT MAGNETIC MATERIALS BY TYPE, USD BILLION, 2021

FIGURE 13 GLOBAL SOFT MAGNETIC MATERIALSBY END USER, USD BILLION, 2021

FIGURE 14 GLOBAL SOFT MAGNETIC MATERIAL SBY APPLICATION USD BILLION, 2021

FIGURE 15 GLOBAL SOFT MAGNETIC MATERIALS BY REGION, USD BILLION, 2021

FIGURE 16 PORTER’S FIVE FORCES MODEL

FIGURE 17 MARKET SHARE ANALYSIS

FIGURE 18 HITACHI METALS: COMPANY SNAPSHOT

FIGURE 19 TOSHIBA MATERIALS: COMPANY SNAPSHOT

FIGURE 20 GKN SINTER METALS: COMPANY SNAPSHOT

FIGURE 21 SINTEX: COMPANY SNAPSHOT

FIGURE 22 MATE CO.LTD: COMPANY SNAPSHOT

FIGURE 23 JFE STEEL GROUP: COMPANY SNAPSHOT

FIGURE 24 MAHINDRA CIE: COMPANY SNAPSHOT

FIGURE 25 MEYER SINTERMETAL AG: COMPANY SNAPSHOT

FIGURE 26 ARNOLD MAGNETIC TECHNOLOGIES: COMPANY SNAPSHOT

DOWNLOAD FREE SAMPLE REPORT

License Type

SPEAK WITH OUR ANALYST

Want to know more about the report or any specific requirement?

WANT TO CUSTOMIZE THE REPORT?

Our Clients Speak

We asked them to research ‘ Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te

Yosuke Mitsui

Senior Associate Construction Equipment Sales & Marketing

We asked them to research ‘Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te