Base Year Value ()

x.x %

x.x %

CAGR ()

x.x %

x.x %

Forecast Year Value ()

x.x %

x.x %

Historical Data Period

Largest Region

Forecast Period

推力ベクトル制御市場:技術別(ジンバルノズル、フレックスノズル、スラスタ、回転ノズル、その他)、システム別(推力ベクトル作動システム、推力ベクトル噴射システム、推力ベクトルスラスタシステム)、アプリケーション別(打ち上げ機、ミサイル、衛星、戦闘機)、エンドユーザー別(宇宙機関、防衛および航空宇宙)および地域別、2023年から2029年までの世界的動向および予測

Instant access to hundreds of data points and trends

- Market estimates from 2014-2029

- Competitive analysis, industry segmentation, financial benchmarks

- Incorporates SWOT, Porter's Five Forces and risk management frameworks

- PDF report or online database with Word, Excel and PowerPoint export options

- 100% money back guarantee

推力ベクトル制御市場の概要

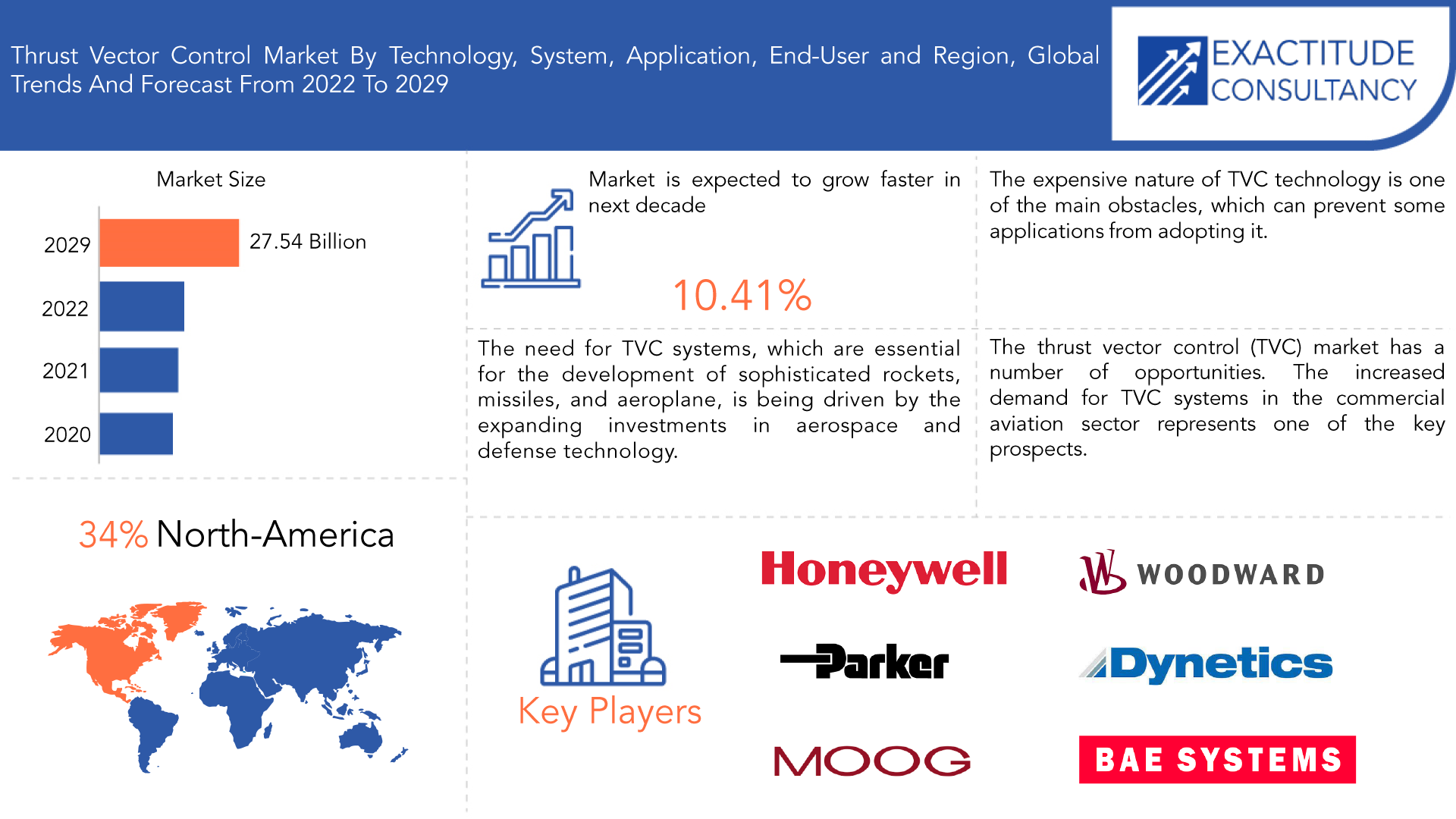

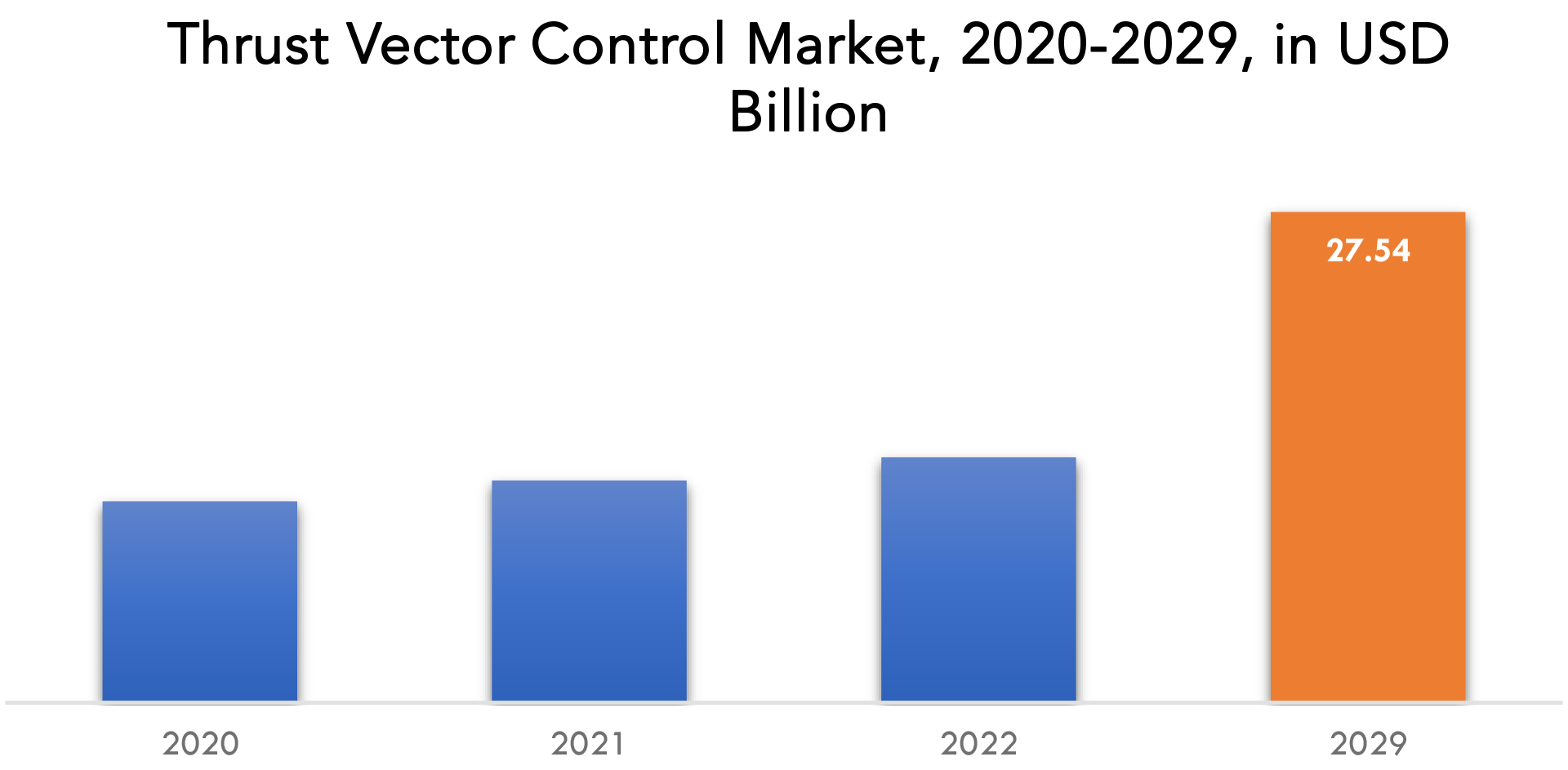

推力ベクトル制御市場は、2022年から2029年にかけて10.41%のCAGRで成長すると予想されています。2020年の 113億ドルから2029年には275億4,000万ドルを超えると予想されています。

推力の方向を調整するために、ロケットエンジンやジェットエンジンでは、推力ベクトル制御 (TVC) と呼ばれる技術が使用されています。排気ガスの方向を変更してロケットや航空機の方向を変えるには、エンジンの排気ノズルを操作する必要があります。TVC システムでは、通常、ノズルが移動し、推力の方向は機械式または油圧式のアクチュエータによって制御されます。より高度な TVC システムでは、より高い精度と制御性を提供する電気式または電子式のアクチュエータが使用される場合があります。ロケットやミサイルの敏捷性と精度を高めるために、TVC が頻繁に使用されます。さらに、ジェットエンジンで利用して航空機の性能と操縦性を高めることもできます。アクチュエータ、制御、材料技術の新たな開発により、TVC 技術は継続的に改善され、推力の方向に対するさらに高い精度と制御が可能になっています。

推力ベクトル制御 (TVC) 市場を構成する産業には、ロケット、ミサイル、航空機エンジンに TVC 技術が採用されている航空宇宙および防衛部門があります。高性能ロケットとミサイル、およびより機敏で操縦性に優れた航空機に対する需要の高まりにより、TVCシステム市場は今後数年間で急速に拡大すると予想されています。市場を牽引しているのは、精密誘導兵器の需要の高まり、商用および軍事目的の無人航空機 (UAV)の使用拡大、燃料効率の向上と排出量の削減を目的とした商用航空機での TVC 技術の使用拡大などの要因です。

推力ベクトル制御 (TVC) 市場を牽引する要因は多岐にわたります。2 つの主な要因は、無人航空機 (UAV) の使用増加と精密誘導爆弾の需要増加です。さらに、高度なロケット、ミサイル、航空機の開発に不可欠な TVC システムの必要性は、航空宇宙および防衛技術への投資拡大によって推進されています。

| 属性 | 詳細 |

| 研究期間 | 2020-2029 |

| 基準年 | 2021 |

| 推定年 | 2022 |

| 予測年 | 2022-2029 |

| 歴史的時代 | 2018-2020 |

| ユニット | 価値(10億米ドル) |

| セグメンテーション | テクノロジー別、システム別、アプリケーション別、エンドユーザー別、地域別 |

| テクノロジー別 |

|

| システム別 |

|

| アプリケーション別 |

|

| エンドユーザー別 |

|

| 地域別 |

|

成長の原動力にもかかわらず、推力ベクトル制御 (TVC) 市場には一定の障壁があります。TVC 技術の高価な性質は主な障害の 1 つであり、一部のアプリケーションでは採用できない可能性があります。TVC システムは複雑であるため、保守や修理に費用がかかる場合もあり、全体的なコストも増加する可能性があります。

推力ベクトル制御 (TVC) 市場には、いくつかのチャンスがあります。航空会社が航空機の性能を向上させながら排出量と燃料使用量を削減しようとしているため、商業航空部門での TVC システムの需要が高まっており、これが重要な見通しの 1 つです。農業、鉱業、インフラ検査など、多くの業界でUAVの使用が拡大していることも、TVC 技術にとって大きなチャンスとなっています。

COVID-19パンデミックの流行は、世界中の推力ベクトル化市場に重大な悪影響を及ぼしています。COVID-19の流行により、ほぼすべての主要国で経済成長が鈍化し、消費者の購買パターンに影響を及ぼしました。多くの国の交通システムで実施されたロックダウンの結果、需給ギャップが拡大し、国内外のサプライチェーンに悪影響を及ぼしています。小規模サプライヤーやいくつかのOEMは、十分な資金がないため、事業を遂行することができません。

[キャプション id="attachment_19977" align="aligncenter" width="1920"]

Frequently Asked Questions

• What is the expected CAGR in terms of revenue for the global thrust vector control market over the forecast period (2020–2029)?

The global thrust vector control market revenue is projected to expand at a CAGR of 10.41% during the forecast period.

• What was the global thrust vector control market valued at in 2020?

The global thrust vector control market was valued at USD 11.30 Billion in 2020.

• Who are the major players operating in the market?

The thrust vector control market key players include Honeywell International Inc., SABCA, Moog Inc., Dynetics Inc., Woodward Inc., Sierra Nevada Corporation, Jansen Aircraft Systems Control Inc., Parker Hannifin Inc, and BAE Systems, Wickman Spacecraft & Propulsion Company.

• Which segment has the largest share in the thrust vector control market?

The thrust vector control market vendors should focus on grabbing business opportunities from the flex nozzle segment as it accounted for the largest market share in the base year.

• What are the key factors driving the growth of thrust vector control market?

The key factors driving the thrust vector control market growth are:

- Need for thrust reverser to tackle adverse climatic conditions during landing

- Growing demand for commercial and general aircraft

Thrust Vector Control Market Segment Analysis

The thrust vector control market is segmented based on technology, system, application, end-user and region.

Based on technology market is divided into gimbal nozzle, flex nozzle, thrusters, rotating nozzle, others; based on system market is divided into thrust vector actuation system, thrust vector injection system, thrust vector thruster system; based on application market is divided into launch vehicles, missiles, satellites, fighter aircraft; and based on end-user market is divided into space agencies, and defense & aerospace.

A significant portion of the market's growth throughout the projection period will be attributed to the flex nozzle segment. The underwater nozzle, which is attached to the main motor by a flexible joint, can be vectorized in all directions and at certain angles with the help of the FNC device's actuation mechanism. As a result, throughout the forecast period, the flex nozzle segment of the worldwide thrust vector control (TVC) market is anticipated to rise due to the rising popularity of small satellite launchers.

The highest revenue-generating segment in 2021 was the thrust vector actuation system segment in terms of system, and it is anticipated that it would remain in that position throughout the projected period. Both the Raytheon advanced sea-sparrow missile and the long-range guided multiple launch rocket system from Lockheed Martin use these actuation technologies.

In terms of market share, the aircraft segment now holds the top spot among application segments for thrust vector control (TVC). This is a result of the rising demand for aircraft that use less fuel and have better performance, lower emissions, and more advanced safety measures. To accomplish these objectives, commercial and military aircraft are using TVC technology more frequently. By utilizing TVC systems, aircraft may do complex man oeuvres, have better takeoff and landing performance, and have a smaller turning radius. Also, the growing demand for unmanned aerial vehicles (UAVs) and investments in aerospace technology are fueling the expansion of the TVC market in the aircraft sector.

In terms of market share, the thrust vector control (TVC) market's aerospace and defense category now holds the lead. This is due to new propulsion systems with better performance, finer control, and more mobility are becoming more and more in demand for aerospace and defense applications. In order to accomplish these objectives, the aerospace and defense sector uses TVC technology in the propulsion systems of rockets, missiles, aeroplane, unmanned aerial vehicles (UAVs), spacecraft, and ships and submarines. Also, the TVC market in the aerospace and defense sector is expanding as a result of rising investments in satellite launches, space research, and defense technology.

[caption id="attachment_19978" align="aligncenter" width="1920"]

Thrust Vector Control Market Key Players

The Thrust Vector Control Market key players include Honeywell International Inc., SABCA, Moog Inc., Dynetics Inc., Woodward Inc., Sierra Nevada Corporation, Jansen Aircraft Systems Control Inc., Parker Hannifin Inc, BAE Systems, Wickman Spacecraft & Propulsion Company, and others.

Recent Developments:- 09 March 2023: Honeywell (Nasdaq: HON) announced a new collaboration with Marriott International to improve in-room comfort and control for guests who stay at hotels across Marriott Bonvoy’s portfolio of extraordinary hotel brands.

- 15 December 2022: Honeywell and Johnson Matthey (JM), announced they will work together to deploy low carbon1 hydrogen solutions. The companies will offer JM's innovative LCH technology, coupled with Honeywell's leading carbon capture technology to produce lower carbon intensity hydrogen at scale.

Who Should Buy? Or Key Stakeholders

- Investors

- Government Organizations

- Military Organizations

- End-user Companies

- Research Organizations

- Regulatory Authorities

- Others

Thrust Vector Control Market Regional Analysis

The Thrust Vector Control Market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).

- North America: includes the US, Canada, Mexico, and Rest of North America

- Asia Pacific: includes China, Japan, South Korea, India, Australia, and Rest of APAC

- Europe: includes UK, Germany, France, Italy, Spain, Netherlands, and Rest of Europe

- South America: includes Brazil, Argentina, and Rest of South America

- Middle East & Africa: includes UAE, South Africa, and the Rest of MEA

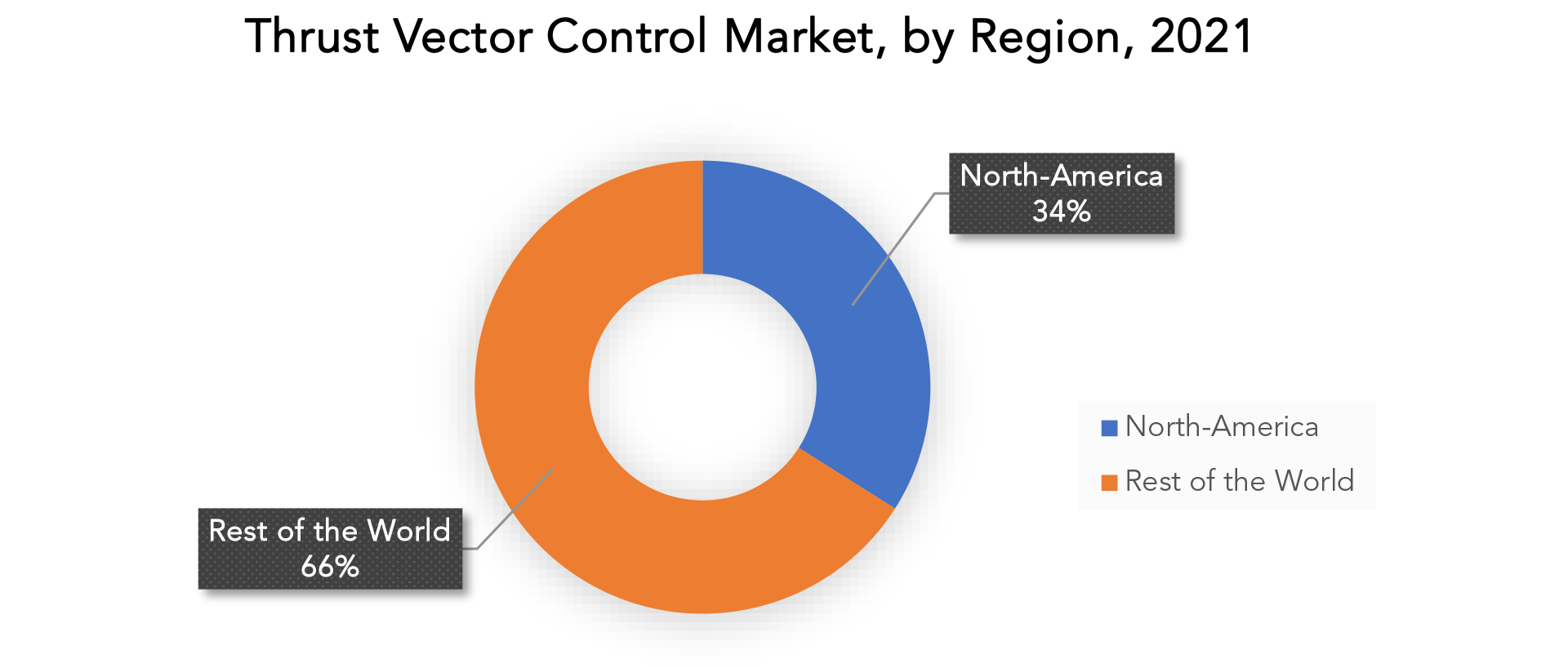

The largest market share was held by North America, which is expected to maintain its dominance during the projection period. The biggest defense spending and increasing space exploration operations are the causes of the growth. Rising satellite launches and rising fighter jet purchases with thrust vector control will also contribute to regional market expansion.

The US government's increasing spending on the military and defense industry also contributes to the expansion of the TVC system in North America. For instance, the US government spent USD 593.40 billion on the military in 2016, and USD 598.70 billion in 2017, according to the US Government Spending Study. It is anticipated that these rising investments would continue to support rising military aircraft production. The demand for TVC systems in the area is then anticipated to increase as a result.

Throughout the course of the forecast period, the market in the Asia Pacific region is anticipated to rise significantly with the highest CAGR. This is because the government is spending more money on launching new rockets and launchers.

[caption id="attachment_19979" align="aligncenter" width="1920"]

Key Market Segments: Thrust Vector Control Market

Thrust Vector Control Market By Technology, 2020-2029, (USD Billion)- Gimbal Nozzle

- Flex Nozzle

- Thrusters

- Rotating Nozzle

- Others

- Thrust Vector Actuation System

- Thrust Vector Injection System

- Thrust Vector Thruster System

- Launch Vehicles

- Missiles

- Satellites

- Fighter Aircraft

- Space Agencies

- Defense

- North America

- Asia Pacific

- Europe

- South America

- Middle East And Africa

Exactitude Consultancy Services Key Objectives:

- Increasing sales and market share

- Developing new technology

- Improving profitability

- Entering new markets

- Enhancing brand reputation

Key Question Answered

- What is the expected growth rate of the thrust vector control market over the next 7 years?

- Who are the major players in the thrust vector control market and what is their market share?

- What are the end-user industries driving demand for market and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-pacific, Middle East, and Africa?

- How is the economic environment affecting the thrust vector control market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the thrust vector control market?

- What is the current and forecasted size and growth rate of the global thrust vector control market?

- What are the key drivers of growth in the thrust vector control market?

- Who are the major players in the market and what is their market share?

- What are the distribution channels and supply chain dynamics in the thrust vector control market?

- What are the technological advancements and innovations in the thrust vector control market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the thrust vector control market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the thrust vector control market?

- What are the product offerings and specifications of leading players in the market?

- 導入

- 市場の定義

- 市場セグメンテーション

- 研究タイムライン

- 前提と制限

- 研究方法

- データマイニング

- 二次調査

- 一次研究

- 専門家のアドバイス

- 品質チェック

- 最終レビュー

- データの三角測量

- ボトムアップアプローチ

- トップダウンアプローチ

- 研究の流れ

- データソース

- データマイニング

- エグゼクティブサマリー

- 市場概要

- 推力ベクトル制御の世界市場の見通し

- 市場の推進要因

- 市場の制約

- 市場機会

- Impact of Covid-19 on Thrust Vector Control Market

- Porter’s five forces model

- Threat from new entrants

- Threat from substitutes

- Bargaining power of suppliers

- Bargaining power of customers

- Degree of competition

- Industry value chain Analysis

- 推力ベクトル制御の世界市場の見通し

- Global Thrust Vector Control Market By Technology (USD Billion)

- Gimbal Nozzle

- Flex Nozzle

- Thrusters

- Rotating Nozzle

- Others

- Global Thrust Vector Control Market By System (USD Billion)

- Thrust Vector Actuation System

- Thrust Vector Injection System

- Thrust Vector Thruster System

- Global Thrust Vector Control Market By Application (USD Billion)

- Launch Vehicles

- Missiles

- Satellites

- Fighter Aircraft

- Global Thrust Vector Control Market By End-User (USD Billion)

- Space Agencies

- Defense

- Global Thrust Vector Control Market By Region (USD Billion)

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest Of South America

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Netherlands

- Rest Of Europe

- Asia Pacific

- India

- China

- Japan

- South Korea

- Australia

- Rest Of Asia Pacific

- Middle East and Africa

- UAE

- South Africa

- Rest Of Middle East and Africa

- North America

- Company Profiles*

(Business Overview, Company Snapshot, Products Offered, Recent Developments)

- Honeywell International Inc.

- SABCA

- Moog Inc.

- Dynetics Inc.

- Woodward Inc.

- Sierra Nevada Corporation

- Jansen Aircraft Systems Control Inc.

- Parker Hannifin Inc.

- BAE Systems

- Wickman Spacecraft & Propulsion Company

*The Company List Is Indicative

LIST OF TABLES

TABLE 1 GLOBAL THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 2 GLOBAL THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 3 GLOBAL THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 4 GLOBAL THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 5 GLOBAL THRUST VECTOR CONTROL MARKET BY REGION (USD BILLION), 2020-2029

TABLE 6 NORTH AMERICA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 7 NORTH AMERICA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 8 NORTH AMERICA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 9 NORTH AMERICA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 10 NORTH AMERICA THRUST VECTOR CONTROL MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 11 US THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 12 US THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 13 US THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 14 US THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 15 CANADA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (BILLION), 2020-2029

TABLE 16 CANADA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 17 CANADA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 18 CANADA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 19 MEXICO THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 20 MEXICO THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 21 MEXICO THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 22 MEXICO THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 23 SOUTH AMERICA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 24 SOUTH AMERICA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 25 SOUTH AMERICA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 26 SOUTH AMERICA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 27 SOUTH AMERICA THRUST VECTOR CONTROL MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 28 BRAZIL THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 29 BRAZIL THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 30 BRAZIL THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 31 BRAZIL THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 32 ARGENTINA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 33 ARGENTINA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 34 ARGENTINA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 35 ARGENTINA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 36 REST OF SOUTH AMERICA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 37 REST OF SOUTH AMERICA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 38 REST OF SOUTH AMERICA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 39 REST OF SOUTH AMERICA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 40 ASIA -PACIFIC THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 41 ASIA -PACIFIC THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 42 ASIA -PACIFIC THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 43 ASIA -PACIFIC THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 44 ASIA -PACIFIC THRUST VECTOR CONTROL MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 45 INDIA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 46 INDIA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 47 INDIA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 48 INDIA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 49 CHINA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 50 CHINA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 51 CHINA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 52 CHINA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 53 JAPAN THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 54 JAPAN THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 55 JAPAN THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 56 JAPAN THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 57 SOUTH KOREA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 58 SOUTH KOREA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 59 SOUTH KOREA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 60 SOUTH KOREA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 61 AUSTRALIA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 62 AUSTRALIA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 63 AUSTRALIA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 64 AUSTRALIA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 65 REST OF ASIA PACIFIC THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 66 REST OF ASIA PACIFIC THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 67 REST OF ASIA PACIFIC THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 68 REST OF ASIA PACIFIC THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 69 EUROPE THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 70 EUROPE THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 71 EUROPE THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 72 EUROPE THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 73 EUROPE THRUST VECTOR CONTROL MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 74 GERMANY THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 75 GERMANY THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 76 GERMANY THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 77 GERMANY THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 78 UK THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 79 UK THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 80 UK THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 81 UK THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 82 FRANCE THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 83 FRANCE THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 84 FRANCE THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 85 FRANCE THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 86 ITALY THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 87 ITALY THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 88 ITALY THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 89 ITALY THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 90 SPAIN THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 91 SPAIN THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 92 SPAIN THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 93 SPAIN THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 94 NETHERLANDS THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 95 NETHERLANDS THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 96 NETHERLANDS THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 97 NETHERLANDS THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 98 REST OF EUROPE THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 99 REST OF EUROPE THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 100 REST OF EUROPE THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 101 REST OF EUROPE THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 102 MIDDLE EAST AND AFRICA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 103 MIDDLE EAST AND AFRICA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 104 MIDDLE EAST AND AFRICA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 105 MIDDLE EAST AND AFRICA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 106 MIDDLE EAST ABD AFRICA THRUST VECTOR CONTROL MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 107 UAE THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 108 UAE THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 109 UAE THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 110 UAE THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 111 SOUTH AFRICA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 112 SOUTH AFRICA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 113 SOUTH AFRICA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 114 SOUTH AFRICA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 115 REST OF MIDDLE EAST AND AFRICA THRUST VECTOR CONTROL MARKET BY TECHNOLOGY (USD BILLION), 2020-2029

TABLE 116 REST OF MIDDLE EAST AND AFRICA THRUST VECTOR CONTROL MARKET BY SYSTEM (USD BILLION), 2020-2029

TABLE 117 REST OF MIDDLE EAST AND AFRICA THRUST VECTOR CONTROL MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 118 REST OF MIDDLE EAST AND AFRICA THRUST VECTOR CONTROL MARKET BY END-USER (USD BILLION), 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL THRUST VECTOR CONTROL MARKET BY TECHNOLOGY, USD BILLION, 2020-2029

FIGURE 9 GLOBAL THRUST VECTOR CONTROL MARKET BY SYSTEM, USD BILLION, 2020-2029

FIGURE 10 GLOBAL THRUST VECTOR CONTROL MARKET BY APPLICATION, USD BILLION, 2020-2029

FIGURE 11 GLOBAL THRUST VECTOR CONTROL MARKET BY ORGANIZATION SIZE, USD BILLION, 2020-2029

FIGURE 12 GLOBAL THRUST VECTOR CONTROL MARKET BY REGION, USD BILLION, 2020-2029

FIGURE 13 PORTER’S FIVE FORCES MODEL

FIGURE 14 GLOBAL THRUST VECTOR CONTROL MARKET BY TECHNOLOGY, USD BILLION, 2021

FIGURE 15 GLOBAL THRUST VECTOR CONTROL MARKET BY SYSTEM, USD BILLION, 2021

FIGURE 16 GLOBAL THRUST VECTOR CONTROL MARKET BY APPLICATION, USD BILLION, 2021

FIGURE 17 GLOBAL THRUST VECTOR CONTROL MARKET BY END-USER, USD BILLION, 2021

FIGURE 18 GLOBAL THRUST VECTOR CONTROL MARKET BY REGION, USD BILLION, 2021

FIGURE 19 MARKET SHARE ANALYSIS

FIGURE 20 HONEYWELL INTERNATIONAL INC.: COMPANY SNAPSHOT

FIGURE 21 SABCA: COMPANY SNAPSHOT

FIGURE 22 MOOG INC.: COMPANY SNAPSHOT

FIGURE 23 DYNETICS INC.: COMPANY SNAPSHOT

FIGURE 24 WOODWARD INC.: COMPANY SNAPSHOT

FIGURE 25 SIERRA NEVADA CORPORATION: COMPANY SNAPSHOT

FIGURE 26 JANSEN AIRCRAFT SYSTEMS CONTROL INC.: COMPANY SNAPSHOT

FIGURE 27 PARKER HANNIFIN INC.: COMPANY SNAPSHOT

FIGURE 28 BAE SYSTEMS: COMPANY SNAPSHOT

FIGURE 29 WICKMAN SPACECRAFT & PROPULSION COMPANY: COMPANY SNAPSHOT

DOWNLOAD FREE SAMPLE REPORT

License Type

SPEAK WITH OUR ANALYST

Want to know more about the report or any specific requirement?

WANT TO CUSTOMIZE THE REPORT?

Our Clients Speak

We asked them to research ‘ Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te

Yosuke Mitsui

Senior Associate Construction Equipment Sales & Marketing

We asked them to research ‘Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te