Base Year Value ()

x.x %

x.x %

CAGR ()

x.x %

x.x %

Forecast Year Value ()

x.x %

x.x %

Historical Data Period

Largest Region

Forecast Period

서버 아키텍처(블레이드 서버, 랙 마운트 서버) 플랫폼(육상, 공중, 해군, 무인 차량, 우주), 애플리케이션(정보, 감시 및 정찰(ISR), 전자전, 지휘 및 통제, 통신 및 항법, 무기 및 사격 통제, 웨어러블, 기타), 설치 유형(신규 설치, 업그레이드), 구성 요소(하드웨어, 소프트웨어), 서비스 및 지역별 군용 임베디드 시스템 시장 2022년부터 2029년까지의 글로벌 트렌드 및 예측

Instant access to hundreds of data points and trends

- Market estimates from 2014-2029

- Competitive analysis, industry segmentation, financial benchmarks

- Incorporates SWOT, Porter's Five Forces and risk management frameworks

- PDF report or online database with Word, Excel and PowerPoint export options

- 100% money back guarantee

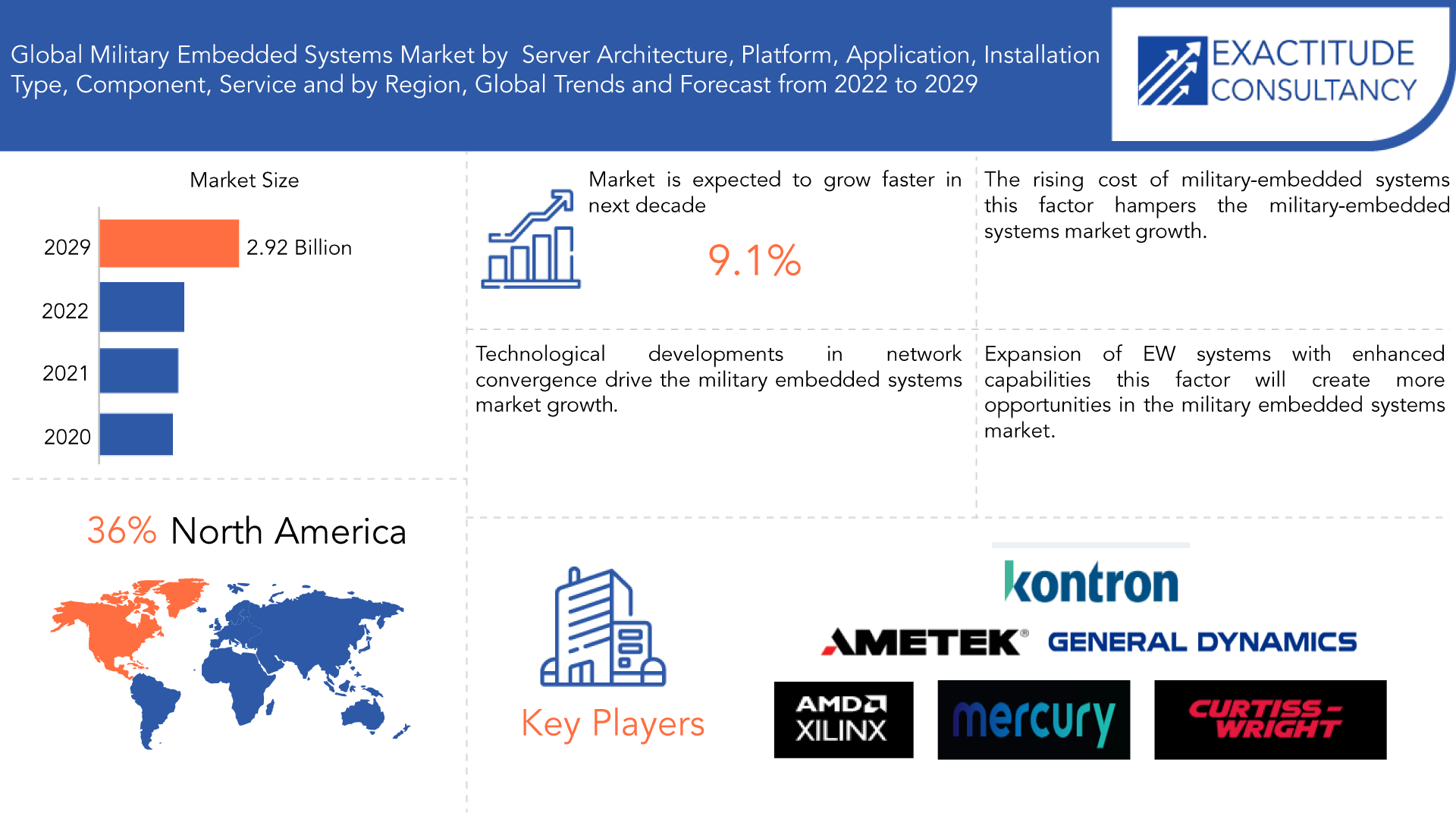

군사 임베디드 시스템 시장 개요

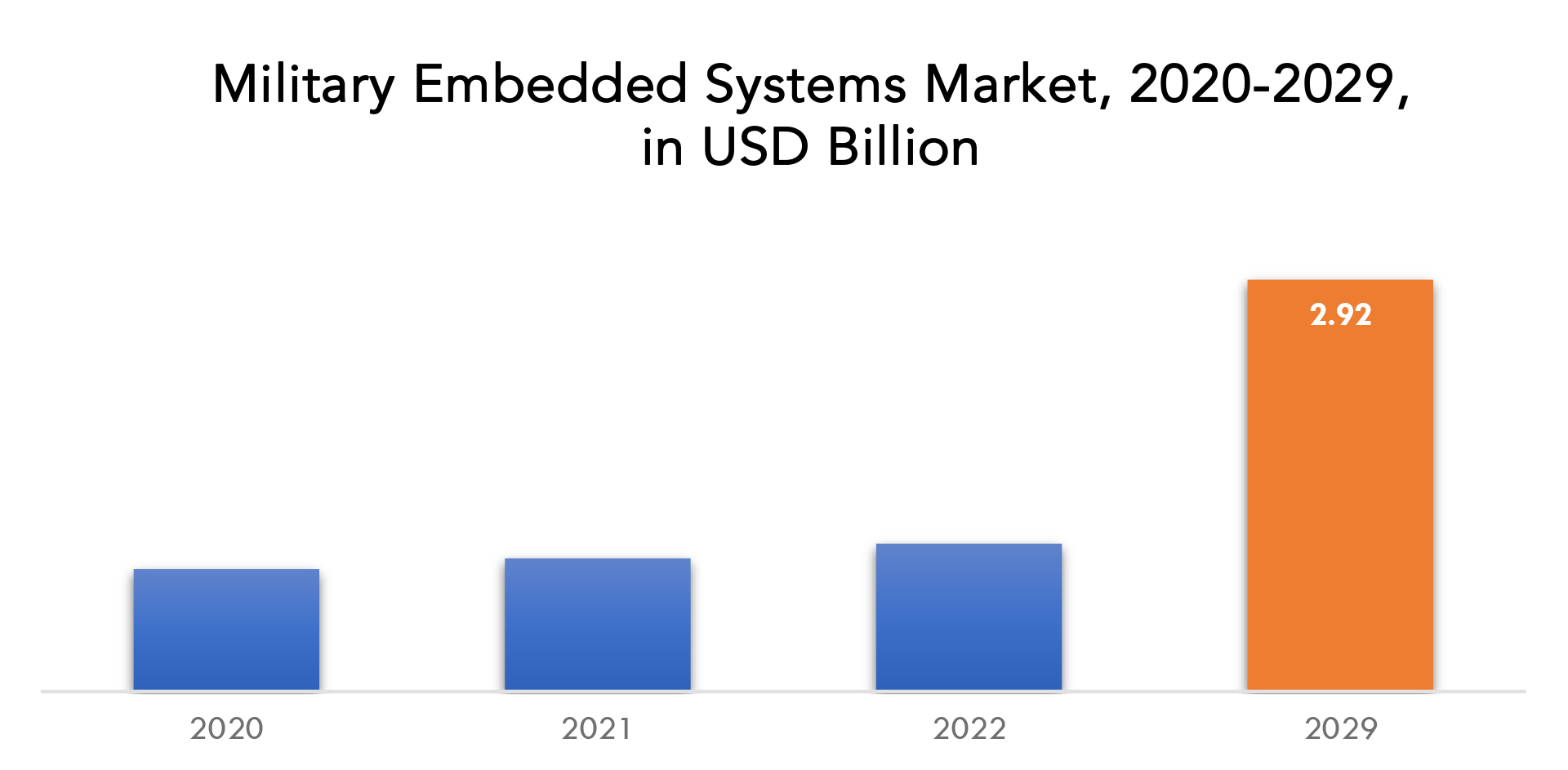

글로벌 군사 임베디드 시스템 시장은 2020년부터 2029년까지 9.1%의 CAGR로 성장할 것으로 예상됩니다. 2020년 8억 7천만 달러에서 2029년에는 29억 2천만 달러를 넘어설 것으로 예상됩니다.

군용 임베디드 시스템은 군용 애플리케이션에서 임베디드 시스템 기술을 사용하는 것을 말합니다. 임베디드 시스템은 최소한의 사용자 개입 또는 사용자 개입 없이 특정 기능을 수행하도록 설계된 컴퓨터 시스템입니다. 일반적으로 산업용 제어 시스템, 의료 기기, 자동차 시스템 및 군용 시스템을 포함한 광범위한 애플리케이션에서 사용하도록 설계되었습니다. 군용 애플리케이션에서 임베디드 시스템은 무기 시스템, 통신 시스템 및 내비게이션 시스템을 포함한 다양한 시스템을 제어하는 데 사용됩니다 . 이러한 시스템은 군사 작전의 성공에 중요하며 매우 안정적이고 안전하며 효율적이어야 합니다. 군용 애플리케이션에서 임베디드 시스템을 사용하는 데는 몇 가지 과제가 있습니다. 군용 시스템은 고온, 고습 및 높은 수준의 진동을 포함한 극한 환경에서 작동할 수 있어야 합니다. 또한 사이버 공격 및 기타 위협 으로부터 보호하기 위해 매우 안전해야 합니다 . 또한 군용 시스템은 실패로 인해 심각한 결과가 초래될 수 있으므로 매우 안정적이어야 합니다.

이러한 과제를 해결하기 위해 군용 임베디드 시스템은 군용 애플리케이션의 특정 요구 사항에 맞게 최적화된 특수 하드웨어 및 소프트웨어를 사용하여 설계됩니다. 이러한 시스템은 종종 환경 테스트를 지정하는 MIL-STD-810G 및 전자기 호환성 테스트를 지정하는 MIL-STD-461을 포함한 엄격한 군 표준을 충족하도록 제작됩니다. 전반적으로 군용 임베디드 시스템은 현대 군사 작전에서 중요한 역할을 하며 군인이 정밀하고 효율적으로 통신하고, 항해하고, 임무를 수행할 수 있도록 합니다.

| 기인하다 | 세부 |

| 학습 기간 | 2020-2029 |

| 기준년도 | 2021 |

| 추정 연도 | 2022 |

| 예상 연도 | 2022-2029 |

| 역사적 기간 | 2018-2020 |

| 단위 | 가치(10억 달러) |

| 분할 | 서버 아키텍처별, 플랫폼별, 애플리케이션별, 설치별, 구성 요소별, 서비스별, 지역별. |

| By Server Architecture |

|

| By Platform |

|

| By Application |

|

| By Installation Type |

|

| By Component |

|

| By Service |

|

| By Region |

|

Modern military operations are becoming increasingly reliant on technology. Embedded systems are a key component of this technology, providing the control and intelligence needed to operate weapons systems, communication networks, and other critical military systems. Military operations require situational awareness, which is the ability to quickly and accurately assess the situation on the ground. Embedded systems provide the necessary data and intelligence to enable soldiers and commanders to make informed decisions based on real-time information. As military systems become more sophisticated, the need for embedded systems technology increases. For example, unmanned aerial vehicles (UAVs) and other autonomous systems rely heavily on embedded systems to operate safely and efficiently. Military embedded systems are designed to be highly reliable and efficient, minimizing the risk of system failures that could jeopardize military operations. They are also optimized for the specific requirements of military applications, enabling soldiers to operate more effectively in the field.

An important factor accelerating market growth is an increase in the demand for fuel-efficient aircraft. Other recent developments integrating cloud computing technologies and wireless in the military, such as network-centric operations and electronic warfare, an increase in the popularity of portable devices with embedded systems, an increase in technological advancements in network convergence, the emergence of electronic and network-centric warfare, and an increase in network convergence are also major drivers of market growth.

Military spending increases by the government are predicted to fuel market expansion. Governments all across the world place a high priority on modernizing military and defense hardware. This situation has greatly expanded both the global supply for unmanned applications and the market opportunity for military embedded systems. Also, it is expected that over the course of the next several decades, the military embedded systems market revenue will increase due to the widespread deployment of multi-core processors, wireless technologies, and innovative warfare systems. Also, the military embedded systems market will see new growth prospects during the above projection period due to the expansion of the potential for software innovation in military computers and the rise in the creation of EW systems with improved capabilities.

Overall, the increasing use of Military Embedded Systems reflects the growing importance of technology in modern military operations, as well as the need for highly reliable and efficient military systems that can operate in challenging environments.

[caption id="attachment_18650" align="aligncenter" width="1920"]

Frequently Asked Questions

• What is the worth of the global military embedded system market?

The global military embedded system market is expected to grow at 9.1 % CAGR from 2020 to 2029. It is expected to reach above USD 2.92 billion by 2029 from USD 0.87 billion in 2020.

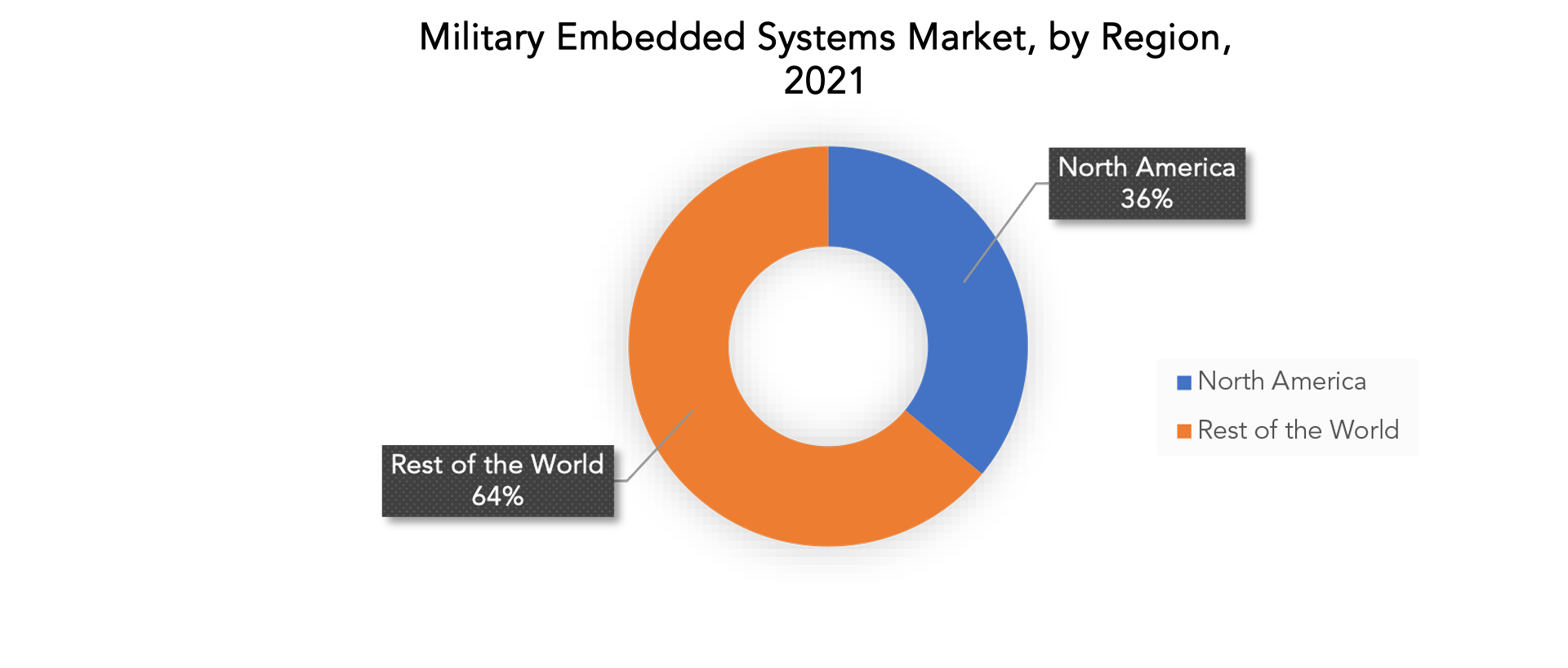

• Which region is dominating the military embedded system market?

North America dominated the global market, and it is anticipated that it will continue to grow at the highest rate throughout the forecast period.

• What are some of the market's driving forces?

Technological developments in network convergence, increasing demand for new and advanced electronic combat systems, and growing use of EW systems for geospatial intelligence gathering are some factors that help to propel the military embedded systems market growth.

• Which are the top companies to hold the market share in the military embedded system market?

The Military Embedded Systems market key players include CURTISS-WRIGHT CORPORATION, KONTRON (S&T AG), MERCURY SYSTEMS, Inc., Ametek, General Dynamics Corporation, Xilinx, Inc., Concurrent Technologies, Eurotech, Dell Technologies, Aitech Defense Systems, Autotec, General Micro Systems, Inc, Advantech Co., Ltd., Thales Group, Smart Embedded Computing, NXP Semiconductors, Advanced Micro Peripherals, Elma Electronic, Texas Instruments Incorporated, Intel Corporation, Radisys, Crystal Group, Vadatech, Avdor Helet, North Atlantic Industries, Inc.

Military Embedded System Market Segment Analysis

The global military embedded system market is segmented based on server architecture, platform, application, installation type, component, service, and region.

Based on server the market is bifurcated into Blade Server and Rack-Mount Server. The architecture blade server segment is dominating the market. In blade server architecture Open VPX dominates Military Embedded Systems Market. For crucial military applications, Open VPX has made substantial advancements in system speeds, dependability, upgradeability, packaging, and SWaP-C (size, weight, and performance-cooling).

Based on the platform the market is bifurcated into land, airborne, naval, unmanned vehicle, and space. The naval segment is dominating the market. Technologies used in naval applications, such as battleships, and submarines, are referred to as navy military embedded systems. The naval section is further separated into destroyers, frigates, corvettes, OPVs, aircraft carriers, and submarines. Defense ships are made expressly for use by coast guards and naval forces to protect water borders. In terms of use, design structure, capabilities, and technologies, these ships differ from commercial ships.

By component the market is bifurcated into hardware and software. The software segment is dominating the market. A combination of computer hardware and software called an embedded system is made to carry out a certain task. Furthermore, embedded systems may function as a component of a larger system. The system may be programmed or it may simply carry out specific tasks. Embedded The software controls the system and the hardware. Managing the operation of a group of hardware components without compromising their intended purpose or efficiency is the core objective of embedded system software.

By application, the market is bifurcated into Intelligence, Surveillance, & Reconnaissance (ISR), Electronic Warfare, Command & Control, Communication & Navigation, Weapon & Fire Control, Wearables, and Others. By installation type, the market is bifurcated into new installations, and upgrades. By service, the market is bifurcated into design, test certification, deployment, renewal, and seamless life cycle support.

[caption id="attachment_18651" align="aligncenter" width="1920"]

Military Embedded System Market Key Players

The Military Embedded Systems market key players include Curtiss-Wright Corporation, Kontron (S&T Ag), Mercury Systems, Inc., Ametek, General Dynamics Corporation, Xilinx, Inc., Concurrent Technologies, Eurotech, Dell Technologies, Aitech Defense Systems, Autotec, General Micro Systems, Inc, Advantech Co., Ltd., Thales Group, Smart Embedded Computing, NXP Semiconductors, Advanced Micro Peripherals, Elma Electronic, Texas Instruments Incorporated, Intel Corporation, Radisys, Crystal Group, Vadatech, Avdor Helet, North Atlantic Industries, Inc.

Industry Development:September 2022 - Curtiss-Wright’s Defense Solutions division, a leading supplier of Modular Open Systems Approach (MOSA)-based solutions engineered for success, announced that it has again been selected by a leading defense system integrator to provide its embedded Security IP module technology. Under the contract, Curtiss-Wright will supply its XMC-528 Mezzanine Card to add state-of-the-art security protection to an existing system within a DoD end-state application.

General Micro Systems launched two MOSA-inspired 3U Open VPX “single board systems” with more processing, sto, rage, and I/O than is available in 6U-sized boards twice the size. Based on an Intel® 11th gen Tiger Lake-H 8 core i7 CPU with 64GB of memory, X9 SPIDER VPX boards are available in conduction- and air-cooled versions. Both products are intended for deployed military and aerospace or rugged applications and were designed in alignment with The Open Group Sensor Open Systems Architecture (SOSA™) technical standard.

Who Should Buy? Or Key stakeholders

- Military Embedded Systems Supplier

- Research Organizations

- Supply Chain Industries

- Investors

- Regulatory Authorities

- Military and Defense Sector

- Aviation and Marine Industry

- Industrial Sectors

- Others

Military Embedded Systems Market Regional Analysis

The Military Embedded System market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).

- North America: includes the US, Canada, Mexico

- Asia Pacific: includes China, Japan, South Korea, India, Australia, ASEAN, and the Rest of APAC

- Europe: includes the UK, Germany, France, Italy, Spain, Russia, and the Rest of Europe

- South America: includes Brazil, Argentina, and the Rest of South America

- Middle East & Africa: includes Turkey, UAE, Saudi Arabia, South Africa, and the Rest of MEA

In 2021, North America dominated the global market, and it is anticipated that it will continue to grow at the highest rate throughout the forecast period. Applications of cutting-edge technology are widely used in North America. As a country with advanced technology, the United States offers tremendous investment possibilities in embedded system technology. Increased expenditures in integrated military capabilities and next-generation communication technology helped the industry in this region expand. The market is expected to rise as a result of increased spending on military equipment and capabilities as well as the adoption of network-centric infrastructure. The two most significant nations in North America are the United States and Canada. In North America, the market for military-embedded systems is dominated by the United States.

North America has a strong military presence, with the United States having the largest military in the world. This creates a large market for military embedded systems, as the military relies heavily on this technology to operate effectively. North America is home to many of the world's leading technology companies, including those that specialize in embedded systems. This has led to the development of advanced military embedded systems that are highly reliable, secure, and efficient. The governments of North American countries, particularly the United States, invest heavily in military technology. This investment includes funding for the development of advanced military embedded systems that are designed to meet the specific needs of the military. These are some factors that also help to propel the North American region’s growth in the military-embedded system market.

Key Market Segments: Military Embedded Systems Market

Military Embedded Systems Market By Server Architecture, 2020-2029, (USD Billion)- Blade Server

- Rack-Mount Server

- Land

- Airborne

- Naval

- Unmanned Vehicles

- Space

- New Installation

- Upgrade

- Hardware

- Software

- Design

- Test & Certification

- Deployment

- Renewal

- Seamless Life Cycle Support

- North America

- Asia Pacific

- Europe

- Latin America

- Middle East And Africa

Exactitude Consultancy Services Key Objectives:

- Increasing sales and market share

- Developing new technology

- Improving profitability

- Entering new markets

- Enhancing brand reputation

Key Question Answered

- What is the current size of the military embedded system market?

- What is the expected growth rate of the military embedded system market over the next 7 years?

- Who are the major players in the military embedded system market and what is their market share?

- What are the end-user industries driving demand for the market and what is their outlook?

- What are the opportunities for growth in emerging markets such as the Asia-pacific, the middle east, and Africa?

- How is the economic environment affecting the high strength of the steel market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the military-embedded system market?

- What is the current and forecasted size and growth rate of the global military embedded system market?

- What are the key drivers of growth in the military embedded system market?

- Who are the major players in the market and what is their market share?

- What are the military embedded system market's distribution channels and supply chain dynamics?

- What are the technological advancements and innovations in the military embedded system market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the military embedded system market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the military embedded system market?

- What are the product offerings specifications of leading players in the market?

- What is the pricing trend of military embedded systems in the market?

- INTRODUCTION

- MARKET DEFINITION

- MARKET SEGMENTATION

- RESEARCH TIMELINES

- ASSUMPTIONS AND LIMITATIONS

- RESEARCH METHODOLOGY

- DATA MINING

- SECONDARY RESEARCH

- PRIMARY RESEARCH

- SUBJECT-MATTER EXPERTS’ ADVICE

- QUALITY CHECKS

- FINAL REVIEW

- DATA TRIANGULATION

- BOTTOM-UP APPROACH

- TOP-DOWN APPROACH

- RESEARCH FLOW

- DATA SOURCES

- DATA MINING

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- GLOBAL MILITARY EMBEDDED SYSTEMS MARKET OUTLOOK

- MARKET DRIVERS

- MARKET RESTRAINTS

- MARKET OPPORTUNITIES

- IMPACT OF COVID-19 ON THE MILITARY EMBEDDED SYSTEMS MARKET

- PORTER’S FIVE FORCES MODEL

- THREAT FROM NEW ENTRANTS

- THREAT FROM SUBSTITUTES

- BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER OF CUSTOMERS

- DEGREE OF COMPETITION

- INDUSTRY VALUE CHAIN ANALYSIS

- GLOBAL MILITARY EMBEDDED SYSTEMS MARKET OUTLOOK

- GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE, 2020-2029, (USD BILLION)

- BLADE SERVER

- RACK-MOUNT SERVER

- GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM, 2020-2029, (USD BILLION)

- LAND

- AIRBORNE

- NAVAL

- UNMANNED VEHICLES

- SPACE

- GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION, 2020-2029, (USD BILLION)

- INTELLIGENCE, SURVEILLANCE, & RECONNAISSANCE (ISR)

- ELECTRONIC WARFARE

- COMMAND & CONTROL

- COMMUNICATION & NAVIGATION

- WEAPON & FIRE CONTROL

- WEARABLES

- OTHERS

- GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE, 2020-2029, (USD BILLION)

- NEW INSTALLATION

- UPGRADE

- GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT, 2020-2029, (USD BILLION)

- HARDWARE

- SOFTWARE

- GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE, 2020-2029, (USD BILLION)

- DESIGN

- TEST & CERTIFICATION

- DEPLOYMENT

- RENEWAL

- SEAMLESS LIFE CYCLE SUPPORT

- GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY REGION, 2020-2029, (USD BILLION)

- NORTH AMERICA

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

- COMPANY PROFILES* (BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCTS OFFERED, RECENT DEVELOPMENTS)

12.1. VOESTALPINE AG

12.2. POSCO GROUP

12.3. ARCELORMITTAL S.A.

12.4. SSAB AB

12.5. NIPPON STEEL & SUMITOMO METAL CORPORATION

12.6. TATA STEEL

12.7. UNITED STATES STEEL CORPORATION

12.12. BAOSTEEL GROUP CORPORATION

12.9. SEVERSTAL JSC

12.10. JFE STEEL CORPORATION *THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 TABLE 1 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY TYPE (USD BILLION) 2020-2029

TABLE 2 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 3 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 4 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 5 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 6 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 7 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 8 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY REGION (USD BILLION) 2020-2029

TABLE 9 NORTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 10 NORTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 11 NORTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 12 NORTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 13 NORTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 14 NORTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 15 NORTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 16 US MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 17 US MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 18 US MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 19 US MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 20 US MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 21 US MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 22 CANADA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 23 CANADA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 24 CANADA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 25 CANADA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 26 CANADA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 27 CANADA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 28 MEXICO MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 29 MEXICO MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 30 MEXICO MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 31 MEXICO MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 32 MEXICO MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 33 MEXICO MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 34 SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 35 SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 36 SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 37 SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 38 SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 39 SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 40 SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 41 BRAZIL MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 42 BRAZIL MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 43 BRAZIL MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 44 BRAZIL MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 45 BRAZIL MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 46 BRAZIL MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 47 ARGENTINA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 48 ARGENTINA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 49 ARGENTINA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 50 ARGENTINA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 51 ARGENTINA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 52 ARGENTINA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 53 COLOMBIA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 54 COLOMBIA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 55 COLOMBIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 56 COLOMBIA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 57 COLOMBIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 58 COLOMBIA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 59 REST OF SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 60 REST OF THE SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 61 REST OF SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 62 REST OF THE SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 63 REST OF SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 64 REST OF SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 65 ASIA-PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 66 ASIA-PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 67 ASIA-PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 68 ASIA-PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 69 ASIA-PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 70 ASIA-PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 71 ASIA-PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 72 INDIA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 73 INDIA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 74 INDIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 75 INDIA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 76 INDIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 77 INDIA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 78 CHINA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 79 CHINA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 80 CHINA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 81 CHINA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 82 CHINA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 83 CHINA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 84 JAPAN MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 85 JAPAN MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 86 JAPAN MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 87 JAPAN MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 88 JAPAN MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 89 JAPAN MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 90 SOUTH KOREA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 91 SOUTH KOREA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 92 SOUTH KOREA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 93 SOUTH KOREA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 94 SOUTH KOREA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 95 SOUTH KOREA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 96 AUSTRALIA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 97 AUSTRALIA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 98 AUSTRALIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 99 AUSTRALIA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 100 AUSTRALIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 101 AUSTRALIA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 102 SOUTH-EAST ASIA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 103 SOUTH-EAST ASIA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 104 SOUTH-EAST ASIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 105 SOUTH-EAST ASIA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 106 SOUTH-EAST ASIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 107 SOUTH-EAST ASIA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 108 REST OF ASIA PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 109 REST OF ASIA PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 110 REST OF ASIA PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 111 REST OF ASIA PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 112 REST OF ASIA PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 113 REST OF ASIA PACIFIC MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 114 EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 115 EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 116 EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 117 EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 118 EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 119 EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 120 EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 121 GERMANY MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 122 GERMANY MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 123 GERMANY MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 124 GERMANY MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 125 GERMANY MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 126 GERMANY MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 127 UK MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 128 UK MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 129 UK MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 130 UK MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 131 UK MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 132 UK MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 133 FRANCE MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 134 FRANCE MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 135 FRANCE MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 136 FRANCE MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 137 FRANCE MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 138 FRANCE MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 139 ITALY MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 140 ITALY MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 141 ITALY MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 142 ITALY MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 143 ITALY MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 144 ITALY MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 145 SPAIN MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 146 SPAIN MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 147 SPAIN MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 148 SPAIN MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 149 SPAIN MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 150 SPAIN MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 151 RUSSIA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 152 RUSSIA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 153 RUSSIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 154 RUSSIA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 155 RUSSIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 156 RUSSIA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 157 REST OF EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 158 REST OF EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 159 REST OF EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 160 REST OF EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 161 REST OF EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 162 REST OF EUROPE MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 163 MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 164 MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 165 MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 166 MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 167 MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 168 MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 169 MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 170 UAE MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 171 UAE MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 172 UAE MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 173 UAE MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 174 UAE MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 175 UAE MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 176 SAUDI ARABIA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 177 SAUDI ARABIA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 178 SAUDI ARABIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 179 SAUDI ARABIA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 180 SAUDI ARABIA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 181 SAUDI ARABIA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 182 SOUTH AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 183 SOUTH AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 184 SOUTH AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 185 SOUTH AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 186 SOUTH AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 187 SOUTH AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

TABLE 188 REST OF THE MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION (USD BILLION) 2020-2029

TABLE 189 REST OF THE MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE (USD BILLION) 2020-2029

TABLE 190 REST OF THE MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE (USD BILLION) 2020-2029

TABLE 191 REST OF THE MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT (USD BILLION) 2020-2029

TABLE 192 REST OF THE MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE (USD BILLION) 2020-2029

TABLE 193 REST OF THE MIDDLE EAST AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM (USD BILLION) 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE, USD BILLION, 2020-2029

FIGURE 9 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM, USD BILLION, 2020-2029

FIGURE 10 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION, USD BILLION, 2020-2029

FIGURE 11 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE, USD BILLION, 2020-2029

FIGURE 12 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT, USD BILLION, 2020-2029

FIGURE 13 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE, USD BILLION, 2020-2029

FIGURE 14 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY REGION, USD BILLION, 2020-2029

FIGURE 15 PORTER’S FIVE FORCES MODEL

FIGURE 16 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY SERVER ARCHITECTURE, USD BILLION, 2021

FIGURE 17 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY PLATFORM, USD BILLION, 2021

FIGURE 18 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY APPLICATION, USD BILLION, 2021

FIGURE 19 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY INSTALLATION TYPE, USD BILLION, 2021

FIGURE 20 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY COMPONENT, USD BILLION, 2021

FIGURE 21 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY SERVICE, USD BILLION, 2021

FIGURE 22 GLOBAL MILITARY EMBEDDED SYSTEMS MARKET BY REGION, USD BILLION, 2021

FIGURE 23 NORTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET SNAPSHOT

FIGURE 24 EUROPE MILITARY EMBEDDED SYSTEMS MARKET SNAPSHOT

FIGURE 25 SOUTH AMERICA MILITARY EMBEDDED SYSTEMS MARKET SNAPSHOT

FIGURE 26 ASIA PACIFIC MILITARY EMBEDDED SYSTEMS MARKET SNAPSHOT

FIGURE 27 MIDDLE EAST ASIA AND AFRICA MILITARY EMBEDDED SYSTEMS MARKET SNAPSHOT

FIGURE 28 MARKET SHARE ANALYSIS

FIGURE 29 CURTISS-WRIGHT CORPORATION: COMPANY SNAPSHOT

FIGURE 30 KONTRON (S&T AG): COMPANY SNAPSHOT

FIGURE 31 MERCURY SYSTEMS, INC.: COMPANY SNAPSHOT

FIGURE 32 AMETEK: COMPANY SNAPSHOT

FIGURE 33 GENERAL DYNAMICS CORPORATION: COMPANY SNAPSHOT

FIGURE 34 XILINX, INC.: COMPANY SNAPSHOT

FIGURE 35 CONCURRENT TECHNOLOGIES: COMPANY SNAPSHOT

FIGURE 36 EUROTECH: COMPANY SNAPSHOT

FIGURE 37 DELL TECHNOLOGIES: COMPANY SNAPSHOT

FIGURE 38 10 AITECH DEFENSE SYSTEMS: COMPANY SNAPSHOT

DOWNLOAD FREE SAMPLE REPORT

License Type

SPEAK WITH OUR ANALYST

Want to know more about the report or any specific requirement?

WANT TO CUSTOMIZE THE REPORT?

Our Clients Speak

We asked them to research ‘ Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te

Yosuke Mitsui

Senior Associate Construction Equipment Sales & Marketing

We asked them to research ‘Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te