Base Year Value ()

x.x %

x.x %

CAGR ()

x.x %

x.x %

Forecast Year Value ()

x.x %

x.x %

Historical Data Period

Largest Region

Forecast Period

Plasma Fractionation Market by Product (Immunoglobulins (Intravenous, Subcutaneous), Coagulation Factors, Albumin), Application (Immunology, Hematology, Neurology), End User (Hospital, Clinical Research Lab, Academic Institutes) And Region, Global Trends and Forecast From 2023 to 2029

Instant access to hundreds of data points and trends

- Market estimates from 2014-2029

- Competitive analysis, industry segmentation, financial benchmarks

- Incorporates SWOT, Porter's Five Forces and risk management frameworks

- PDF report or online database with Word, Excel and PowerPoint export options

- 100% money back guarantee

Plasma Fractionation Market Overview

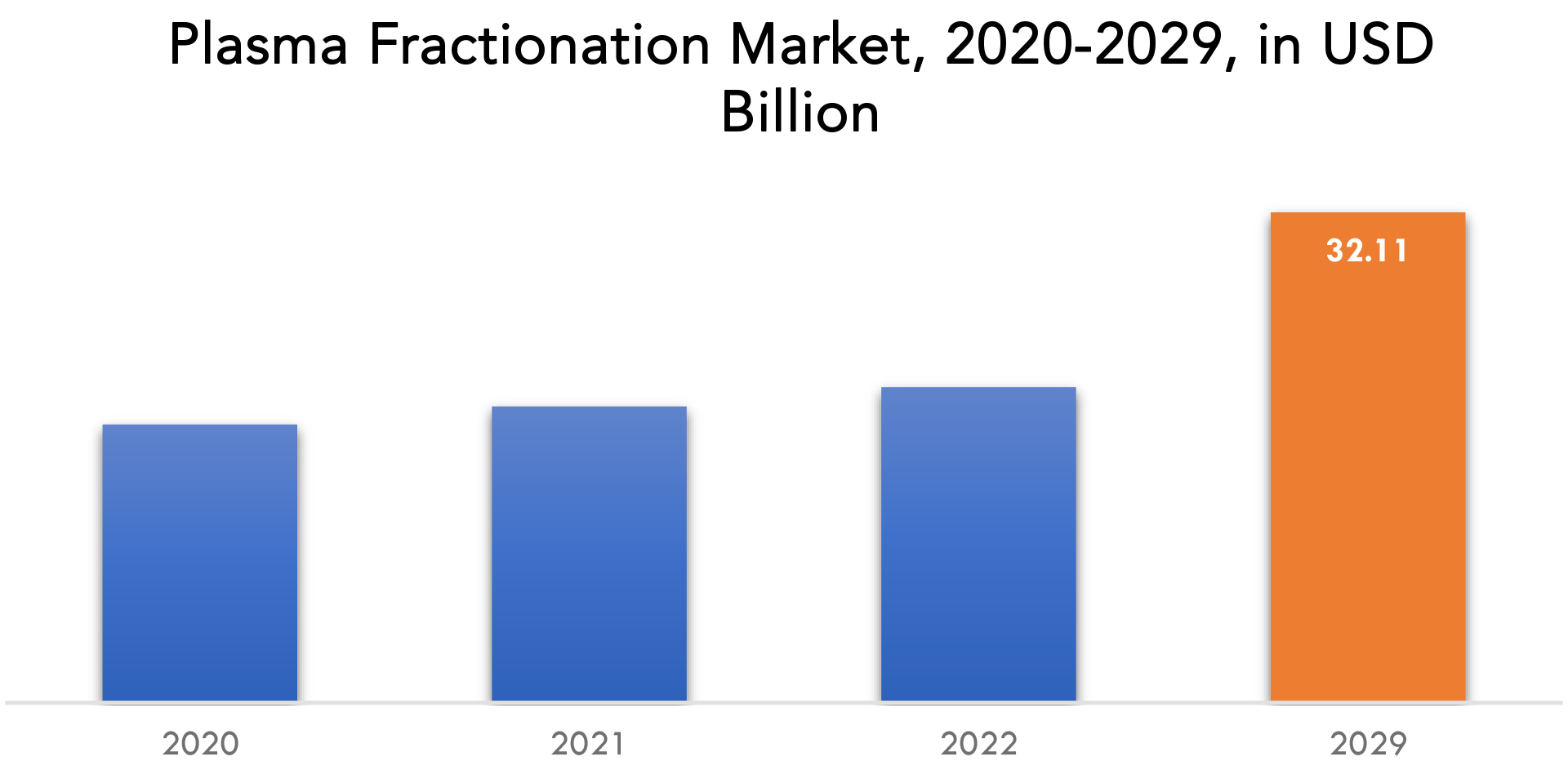

The plasma fractionation market is expected to grow at 6.5% CAGR from 2023 to 2029. It is expected to reach above USD 32.11 billion by 2029 from USD 18.22 billion in 2022.

In addition to salt, water, and enzymes, plasma delivers vital minerals, hormones, and proteins throughout the body. Because of this, plasma plays a crucial role in the treatment of several significant medical conditions. Its essential elements, such as antibodies, clotting factors, the proteins albumin and fibrinogen, can be dissected out and used as treatments for people with burns, shock, immune deficiency disorders, and other uncommon chronic illnesses. Blood plasma fractionation is the term used to describe the process of dividing the plasma into its individual proteins. These fractions have a wide range of therapeutic applications, such as the treatment of immune deficiencies or congenital diseases, the restoration of blood volume following trauma, and the development of highly efficient technologies for the inactivation of viral contaminants, such as hepatitis viruses and the human immunodeficiency virus (HIV).

For several immunologic, hematologic, and neurologic disorders, immunoglobulins are the first line of treatment. Due to technological improvements, the prevalence of numerous immunological illnesses has increased during the past ten years. Due to a rise in the number of individuals with immunodeficiency diagnoses, growing genetic research to characterize and identify immunodeficiency will also increase the clinical requirement for immunoglobulins. IVIg has a few on- and off-label indications, according to IG Living, a publication for the immune globulin (IG) community. In recent years, the use of immunoglobulin for off-label indications has surpassed that for on-label applications; off-label indications make up about 20–60% of its clinical use. These factors are driving market growth. Alpha-1-antitrypsin and immunoglobulins are expected to be used more frequently in a variety of medical specialties worldwide, which will likely fuel market expansion. The growth of blood collection facilities around the world is another significant factor propelling the development of this market.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2029 |

| Base year | 2021 |

| Estimated year | 2022 |

| Forecasted year | 2022-2029 |

| Historical period | 2018-2020 |

| Unit | Value (USD BILLION), (THOUSAND UNITS) |

| Segmentation | By Product, By Application, By End-User and By Region. |

| By PRODUCT

|

|

| By APPLICATION

|

|

| By END-USER

|

|

| By Region

|

|

Plasma fractionation is one of the pharmaceutical industry's most strictly regulated segments. The potential for blood transfer, the attention of regulatory agencies relies on the safety and quality of fractionated plasma products due to borne pathogens (bacteria, viruses, and prions) and other disorders connected to transfusions (such as transmissible spongiform encephalopathies, including variant Creutzfeldt-Jakob disease). To ensure the caliber and security of plasma products, the WHO established standards for the plasma fractionation procedure. In addition to acting as a barrier for new players to enter the industry, the market's strict restrictions limit local small players' ability to develop internationally. While making investments in local or regional markets, like China, multinational corporations also encounter some difficulties. High costs associated with the plasma fractionation and restricted reimbursements and the disruptions that occur due to the incompetent alternatives are expected to be the major market restraints.

Influenza pandemics are sporadic, unforeseen occurrences that have a huge negative impact on society and the economy. In the US, there have been hospitalizations linked to influenza. The prevalence of these contagious diseases is predicted to rise and expected to create opportunities for items made from plasma.

The coronavirus pandemic positively impacted the market, it was projected that greater government spending and business involvement in plasma therapy research and development during pandemic accelerated market expansion. Additionally, the COVID-19 pandemic gave biotechnology and biopharma companies various opportunities to take part in R&D studies concerning plasma therapies.

Despite the current coronavirus pandemic's negative consequences on some enterprises, it has been noted that the global industry has expanded greatly over the previous several years. As the COVID-19 pandemic approached its worst stage, more people were negatively influenced by the viral infection and experienced major issues; this spurred the use of plasma as a treatment. However, because of increased government funding and business involvement in research and development, it is projected that the price of this therapy would increase, limiting market expansion. Additionally, the fact that fractionation therapy was successful in treating COVID-19 patients offered patients hope for plasma therapy.

[caption id="attachment_14898" align="aligncenter" width="1920"]

Frequently Asked Questions

• What is the worth of plasma fractionation market?

The plasma fractionation market is worth USD 20.66 billion and is forecasted to reach above USD 32.11 billion by 2029.

• What are some of the market's driving forces?

Alpha-1-antitrypsin and immunoglobulins are expected to be used more frequently in a variety of medical specialties worldwide, which will likely fuel market expansion. The growth of blood collection facilities around the world is another significant factor propelling the development of this market.

• Which are the top companies to hold the market share in plasma fractionation market?

The plasma fractionation market key players include Grifols S.A., CSL Limited, Takeda Pharmaceutical Company Limited, Octapharma AG, Kedrion S.p.A, LFB S.A., Biotest AG, Sanquin, Bio Products Laboratory Ltd., Intas Pharmaceuticals Ltd

• What is the leading application of plasma fractionation market?

A vital class of medicines known as protein products fractionated from human plasma is used to prevent, manage, and treat life-threatening illnesses brought on by injury, congenital deficits, immunologic disorders, or infections.

• Which is the largest regional market for plasma fractionation market?

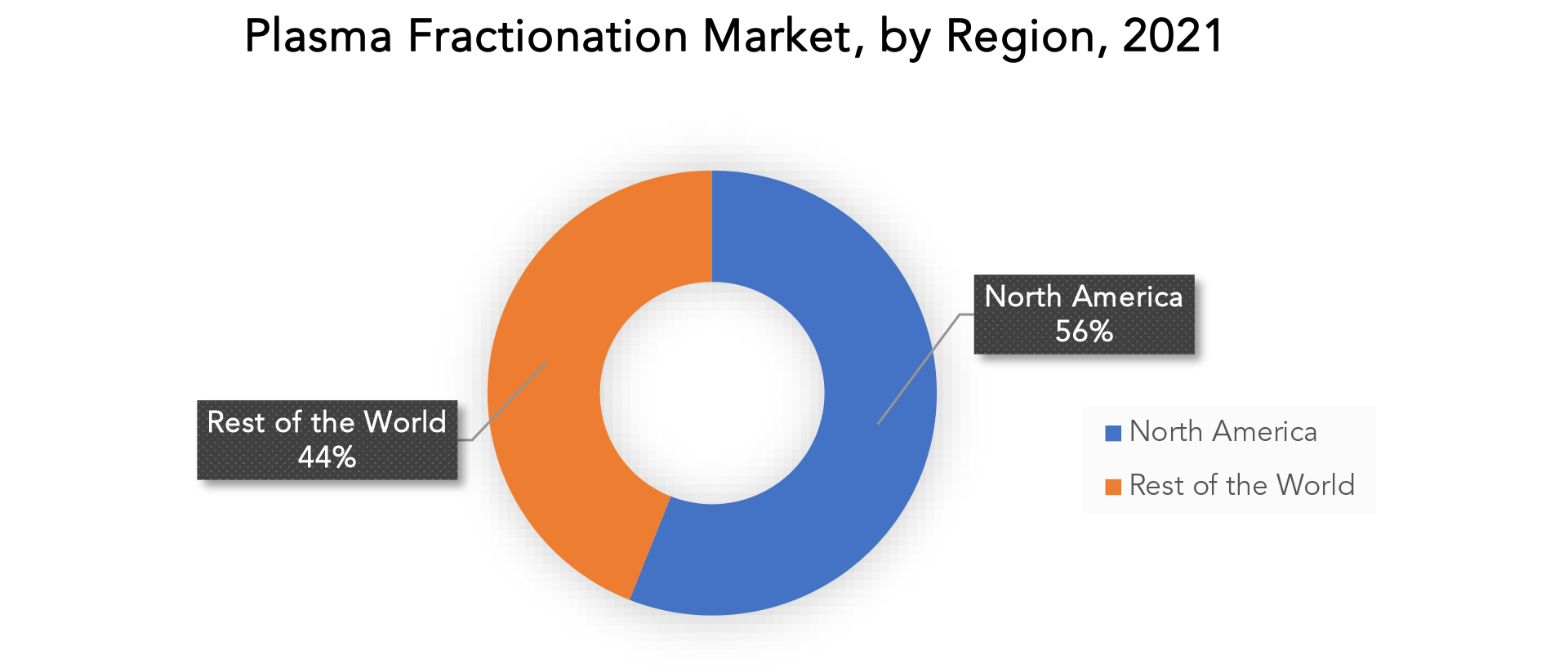

North America is anticipated to have the greatest market share for plasma fractionation worldwide in 2022 because more people are using plasma fractionated goods on a regular basis and more novel items are being developed. The North America plasma fractionation market accounts of 56% of the total global market share.

Plasma Fractionation Market Segment Analysis

Plasma fractionation market is segmented based on by product, application, end user and region.

According to product type, the immunoglobulins segment is anticipated to hold the biggest market share for plasma fractionation in 2022. Due to the wide commercial availability of plasma-derived immunoglobulins in comparison to other plasma-derived products and the expanding use of immunoglobulins, particularly for the treatment of people with primary immune deficiencies or chronic inflammatory demyelinating polyneuropathy, this segment holds a significant market share.

According on application, the plasma fractionation market is anticipated to be dominated by the neurology segment in 2022. The substantial market share of this sector is related to elements like the widespread use of plasma-derived products for the treatment of neurological illnesses and the rising prevalence of neurological disorders.

According to end user, the plasma fractionation market is anticipated to be dominated by the hospitals & clinics segment in 2022. One of the main drivers of this segment's growth is the expanding usage of plasma-based products in numerous therapies, along with the expansion of hospitals and rising healthcare costs.

[caption id="attachment_14904" align="aligncenter" width="1920"]

Plasma Fractionation Market Players

The plasma fractionation market key players include Grifols S.A., CSL Limited, Takeda Pharmaceutical Company Limited, Octapharma AG, Kedrion S.p.A, LFB S.A., Biotest AG, Sanquin, Bio Products Laboratory Ltd., Intas Pharmaceuticals Ltd

January 11, 2023; Grifols a global leader in plasma medicines with more than 110 years contributing to improve the health and well-being of people, announced that its plasma-protein based fibrin sealant (FS) for controlling surgical bleeding obtained positive topline results from a phase 3b clinical trial in pediatric patients. Having met all primary and secondary endpoints, the study is expected to facilitate regulatory approval to expand the use of the FS-based biosurgery treatment, currently indicated for adults, to children and adolescents as well.

November 3, 2022; Grifols, a global leader in plasma-derived medicines and innovative diagnostic solutions, announced that its AlphaID™ At Home Genetic Health Risk Service, the first-ever free direct-to-consumer program in the U.S. to screen for genetic risk of alpha1-antitrypsin deficiency (alpha-1), has been cleared by the U.S. Food and Drug Administration (FDA). The service, also known as AlphaID™ At Home, is the company’s first FDA clearance for direct-to-consumer use. It will be available beginning in Q2 2023 for U.S. adults to screen for their genetic risk level of developing lung and/or liver disease related to alpha-1 without a medical prescription.

Who Should Buy? Or Key Stakeholders

- Investors

- Chemical Industries

- Blood Banks

- Healthcare Centers

- Medical Industries

- Research Organizations

- Institutional Players

- End user companies

- Others

Plasma Fractionation Market Regional Analysis

The plasma fractionation market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).

- North America: includes the US, Canada, Mexico

- Asia Pacific: includes China, Japan, South Korea, India, Australia, ASEAN and Rest of APAC

- Europe: includes UK, Germany, France, Italy, Spain, Russia, and Rest of Europe

- South America: includes Brazil, Argentina, and Rest of South America

- Middle East & Africa: includes Turkey, UAE, Saudi Arabia, South Africa, and Rest of MEA

Geographically, North America is anticipated to have the greatest market share for plasma fractionation worldwide in 2022 because more people are using plasma fractionated goods on a regular basis and more novel items are being developed. The North America plasma fractionation market accounts of 56% of the total global market share, however, during the forecast period, Asia-Pacific is expected to have the greatest CAGR. Collaborations between nations to establish plasma fractionation facilities, awareness campaigns to promote increased use of plasma and its fractionation, the rise in various medical conditions, such as the rising prevalence of hemophilia in nations like China and India that necessitate the use of plasma fractionation products, and the rising geriatric population in the Asia-Pacific region are what are driving the market growth in that region.

The United States is leading the worldwide plasma fractionation market in North America with the highest CAGR because the population there is more aware of the wide-ranging advantages of plasma. China is the market leader for plasma fractionation in Asia-Pacific because of rising demand for the procedure and rising public health awareness. Due to its high elderly population and immune deficiency diseases, Germany is currently dominating the market in Europe with the highest share.

[caption id="attachment_14905" align="aligncenter" width="1920"]

Key Market Segments: Plasma Fractionation Market

Plasma Fractionation Market By Product, 2022-2029, (USD Billion) (Thousand Units)- Immunoglobulins (Intravenous, Subcutaneous)

- Coagulation Factors

- Albumin

- Immunology

- Hematology

- Neurology

- Hospital

- Clinical Research Lab

- Academic Institutes

- North America

- Asia Pacific

- Europe

- South America

- Middle East and Africa

Exactitude Consultancy Services Key Objectives:

- Increasing sales and market share

- Developing new technology

- Improving profitability

- Entering new markets

- Enhancing brand reputation

Key Question Answered

- What is the expected growth rate of the plasma fractionation market over the next 7 years?

- Who are the major players in the plasma fractionation market and what is their market share?

- What are the end-user industries driving demand for market and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-Pacific, Middle East, and Africa?

- How is the economic environment affecting the plasma fractionation market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the plasma fractionation market?

- What is the current and forecasted size and growth rate of the global plasma fractionation market?

- What are the key drivers of growth in the plasma fractionation market?

- Who are the major players in the market and what is their market share?

- What are the distribution channels and supply chain dynamics in the plasma fractionation market?

- What are the technological advancements and innovations in the plasma fractionation market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the plasma fractionation market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the plasma fractionation market?

- What are the product applications and specifications of leading players in the market?

- Introduction

- Market Definition

- Market Segmentation

- Research Timelines

- Assumptions and Limitations

- Research Methodology

- Data Mining

- Secondary Research

- Primary Research

- Subject-Matter Experts’ Advice

- Quality Checks

- Final Review

- Data Triangulation

- Bottom-Up Approach

- Top-Down Approach

- Research Flow

- Data Sources

- Data Mining

- Executive Summary

- Market Overview

- Global plasma fractionation market outlook

- Market Drivers

- Market Restraints

- Market Opportunities

- Impact of Covid-19 on plasma fractionation market

- Porter’s five forces model

- Threat from new entrants

- Threat from substitutes

- Bargaining power of suppliers

- Bargaining power of customers

- Degree of competition

- Industry value chain Analysis

- Global plasma fractionation market outlook

- GLOBAL PLASMA FRACTIONATION MARKET BY PRODUCT 2022-2029, (USD BILLION) (THOUSAND UNITS)

- Immunoglobulins (Intravenous, Subcutaneous)

- Coagulation Factors

- Albumin

- GLOBAL PLASMA FRACTIONATION MARKET BY APPLICATION 2022-2029, (USD BILLION) (THOUSAND UNITS)

- Immunology

- Hematology

- Neurology

- GLOBAL PLASMA FRACTIONATION MARKET BY END-USER 2022-2029, (USD BILLION) (THOUSAND UNITS)

- Hospital

- Clinical Research Lab

- Academic Institutes

- GLOBAL PLASMA FRACTIONATION MARKET BY REGION 2022-2029, (USD BILLION) (THOUSAND UNITS)

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Rest Of South America

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Rest Of Europe

- Asia Pacific

- India

- China

- Japan

- South Korea

- Australia

- South-East Asia

- Rest Of Asia Pacific

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest Of Middle East and Africa

- North America

- Company Profiles*

(Business Overview, Company Snapshot, Products Offered, Recent Developments)

- Grifols S.A.

- CSL Limited

- Takeda Pharmaceutical Company Limited

- Octapharma AG

- Kedrion S.p.A

- LFB S.A.

- Biotest AG

- Sanquin

- Bio Products Laboratory Ltd.

- Intas Pharmaceuticals Ltd

*The Company List Is Indicative

LIST OF TABLES

TABLE 1 GLOBAL PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 2 GLOBAL PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 3 GLOBAL PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 4 GLOBAL PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 5 GLOBAL PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 6 GLOBAL PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 7 GLOBAL PLASMA FRACTIONATION MARKET BY REGION (THOUSAND UNITS), 2020-2029

TABLE 8 GLOBAL PLASMA FRACTIONATION MARKET BY REGION (THOUSAND UNITS), 2020-2029

TABLE 9 NORTH AMERICA PLASMA FRACTIONATION MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 10 NORTH AMERICA PLASMA FRACTIONATION MARKET BY COUNTRY (THOUSAND UNITS), 2020-2029

TABLE 11 NORTH AMERICA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 12 NORTH AMERICA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 13 NORTH AMERICA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 14 NORTH AMERICA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 15 NORTH AMERICA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 16 NORTH AMERICA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 17 US PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 18 US PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 19 US PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 20 US PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 21 US PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 22 US PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 23 CANADA PLASMA FRACTIONATION MARKET BY PRODUCT (BILLION), 2020-2029

TABLE 24 CANADA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 25 CANADA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 26 CANADA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 27 CANADA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 28 CANADA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 29 MEXICO PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 30 MEXICO PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 31 MEXICO PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 32 MEXICO PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 33 MEXICO PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 34 MEXICO PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 35 SOUTH AMERICA PLASMA FRACTIONATION MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 36 SOUTH AMERICA PLASMA FRACTIONATION MARKET BY COUNTRY (THOUSAND UNITS), 2020-2029

TABLE 37 SOUTH AMERICA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 38 SOUTH AMERICA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 39 SOUTH AMERICA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 40 SOUTH AMERICA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 41 SOUTH AMERICA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 42 SOUTH AMERICA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 43 BRAZIL PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 44 BRAZIL PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 45 BRAZIL PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 46 BRAZIL PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 47 BRAZIL PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 48 BRAZIL PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 49 ARGENTINA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 50 ARGENTINA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 51 ARGENTINA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 52 ARGENTINA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 53 ARGENTINA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 54 ARGENTINA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 55 COLOMBIA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 56 COLOMBIA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 57 COLOMBIA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 58 COLOMBIA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 59 COLOMBIA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 60 COLOMBIA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 61 REST OF SOUTH AMERICA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 62 REST OF SOUTH AMERICA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 63 REST OF SOUTH AMERICA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 64 REST OF SOUTH AMERICA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 65 REST OF SOUTH AMERICA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 66 REST OF SOUTH AMERICA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 67 ASIA-PACIFIC PLASMA FRACTIONATION MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 68 ASIA-PACIFIC PLASMA FRACTIONATION MARKET BY COUNTRY (THOUSAND UNITS), 2020-2029

TABLE 69 ASIA-PACIFIC PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 70 ASIA-PACIFIC PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 71 ASIA-PACIFIC PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 72 ASIA-PACIFIC PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 73 ASIA-PACIFIC PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 74 ASIA-PACIFIC PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 75 INDIA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 76 INDIA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 77 INDIA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 78 INDIA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 79 INDIA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 80 INDIA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 81 CHINA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 82 CHINA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 83 CHINA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 84 CHINA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 85 CHINA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 86 CHINA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 87 JAPAN PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 88 JAPAN PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 89 JAPAN PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 90 JAPAN PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 91 JAPAN PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 92 JAPAN PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 93 SOUTH KOREA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 94 SOUTH KOREA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 95 SOUTH KOREA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 96 SOUTH KOREA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 97 SOUTH KOREA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 98 SOUTH KOREA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 99 AUSTRALIA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 100 AUSTRALIA CONNECTED TRUCKBY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 101 AUSTRALIA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 102 AUSTRALIA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 103 AUSTRALIA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 104 AUSTRALIA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 105 SOUTH EAST ASIA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 106 SOUTH EAST ASIA CONNECTED TRUCKBY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 107 SOUTH EAST ASIA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 108 SOUTH EAST ASIA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 109 SOUTH EAST ASIA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 110 SOUTH EAST ASIA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 111 REST OF ASIA PACIFIC PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 112 REST OF ASIA PACIFIC CONNECTED TRUCKBY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 113 REST OF ASIA PACIFIC PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 114 REST OF ASIA PACIFIC PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 115 REST OF ASIA PACIFIC PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 116 REST OF ASIA PACIFIC PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 117 EUROPE PLASMA FRACTIONATION MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 118 EUROPE PLASMA FRACTIONATION MARKET BY COUNTRY TYPE (THOUSAND UNITS), 2020-2029

TABLE 119 EUROPE PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 120 EUROPE PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 121 EUROPE PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 122 EUROPE PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 123 EUROPE PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 124 EUROPE PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 125 GERMANY PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 126 GERMANY PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 127 GERMANY PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 128 GERMANY PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 129 GERMANY PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 130 GERMANY PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 131 UK PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 132 UK PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 133 UK PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 134 UK PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 135 UK PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 136 UK PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 137 FRANCE PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 138 FRANCE PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 139 FRANCE PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 140 FRANCE PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 141 FRANCE PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 142 FRANCE PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 143 ITALY PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 144 ITALY PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 145 ITALY PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 146 ITALY PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 147 ITALY PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020- 2029

TABLE 148 ITALY PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 149 SPAIN PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 150 SPAIN PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 151 SPAIN PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 152 SPAIN PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 153 SPAIN PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 154 SPAIN PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 155 RUSSIA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 156 RUSSIA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 157 RUSSIA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 158 RUSSIA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 159 RUSSIA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 160 RUSSIA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 161 REST OF EUROPE PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 162 REST OF EUROPE PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 163 REST OF EUROPE PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 164 REST OF EUROPE PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 165 REST OF EUROPE PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 166 REST OF EUROPE PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 167 MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 168 MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY COUNTRY (THOUSAND UNITS), 2020-2029

TABLE 169 MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 170 MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 171 MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 172 MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 173 MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 174 MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 175 UAE PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 176 UAE PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 177 UAE PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 178 UAE PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 179 UAE PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 180 UAE PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 181 SAUDI ARABIA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 182 SAUDI ARABIA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 183 SAUDI ARABIA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 184 SAUDI ARABIA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 185 SAUDI ARABIA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 186 SAUDI ARABIA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 187 SOUTH AFRICA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 188 SOUTH AFRICA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 189 SOUTH AFRICA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 190 SOUTH AFRICA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 191 SOUTH AFRICA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 192 SOUTH AFRICA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

TABLE 193 REST OF MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 194 REST OF MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 195 REST OF MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY APPLICATION (USD BILLION), 2020-2029

TABLE 196 REST OF MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY APPLICATION (THOUSAND UNITS), 2020-2029

TABLE 197 REST OF MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY END-USER (USD BILLION), 2020-2029

TABLE 198 REST OF MIDDLE EAST AND AFRICA PLASMA FRACTIONATION MARKET BY END-USER (THOUSAND UNITS), 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL PLASMA FRACTIONATION MARKET BY PRODUCT, USD BILLION, 2020-2029

FIGURE 9 GLOBAL PLASMA FRACTIONATION MARKET BY APPLICATION, USD BILLION, 2020-2029

FIGURE 10 GLOBAL PLASMA FRACTIONATION MARKET BY END-USER, USD BILLION, 2020-2029

FIGURE 11 GLOBAL PLASMA FRACTIONATION MARKET BY REGION, USD BILLION, 2020-2029

FIGURE 12 PORTER’S FIVE FORCES MODEL

FIGURE 13 GLOBAL PLASMA FRACTIONATION MARKET BY PRODUCT, USD BILLION, 2021

FIGURE 14 GLOBAL PLASMA FRACTIONATION MARKET BY APPLICATION, USD BILLION, 2021

FIGURE 15 GLOBAL PLASMA FRACTIONATION MARKET BY END-USER, USD BILLION, 2021

FIGURE 16 GLOBAL PLASMA FRACTIONATION MARKET BY REGION, USD BILLION, 2021

FIGURE 17 MARKET SHARE ANALYSIS

FIGURE 18 GRIFOLS S.A.: COMPANY SNAPSHOT

FIGURE 19 CSL LIMITED: COMPANY SNAPSHOT

FIGURE 20 TAKEDA PHARMACEUTICAL COMPANY LIMITED: COMPANY SNAPSHOT

FIGURE 21 OCTAPHARMA AG: COMPANY SNAPSHOT

FIGURE 22 KEDRION S.P.A: COMPANY SNAPSHOT

FIGURE 23 LFB S.A.: COMPANY SNAPSHOT

FIGURE 24 BIOTEST AG: COMPANY SNAPSHOT

FIGURE 25 SANQUIN: COMPANY SNAPSHOT

FIGURE 26 BIO PRODUCTS LABORATORY LTD.: COMPANY SNAPSHOT

FIGURE 27 INTAS PHARMACEUTICALS LTD: COMPANY SNAPSHOT

DOWNLOAD FREE SAMPLE REPORT

License Type

SPEAK WITH OUR ANALYST

Want to know more about the report or any specific requirement?

WANT TO CUSTOMIZE THE REPORT?

Our Clients Speak

We asked them to research ‘ Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te

Yosuke Mitsui

Senior Associate Construction Equipment Sales & Marketing

We asked them to research ‘Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te