INTERESTED IN THIS RESEARCH?

Contact our analysts for inquiries, samples, and expert insights.

REPORT OUTLOOK

| Market Size | CAGR | Dominating Region |

|---|---|---|

| USD 11.42 billion by 2029 | 13% | North America |

| Market By Product | Market By Service | |

|---|---|---|

|

|

|

SCOPE OF THE REPORT

Healthcare IT Integration Market Overview

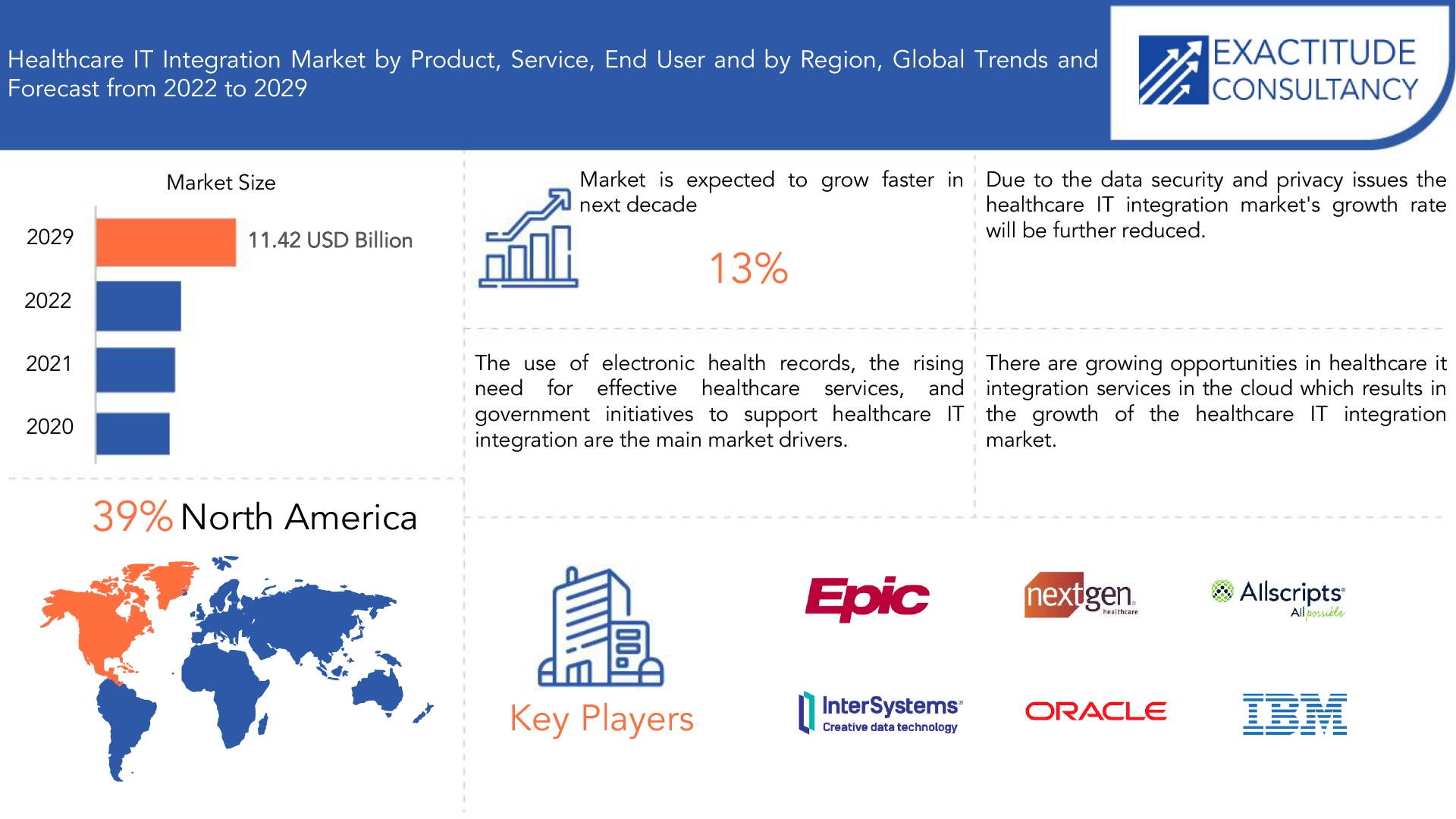

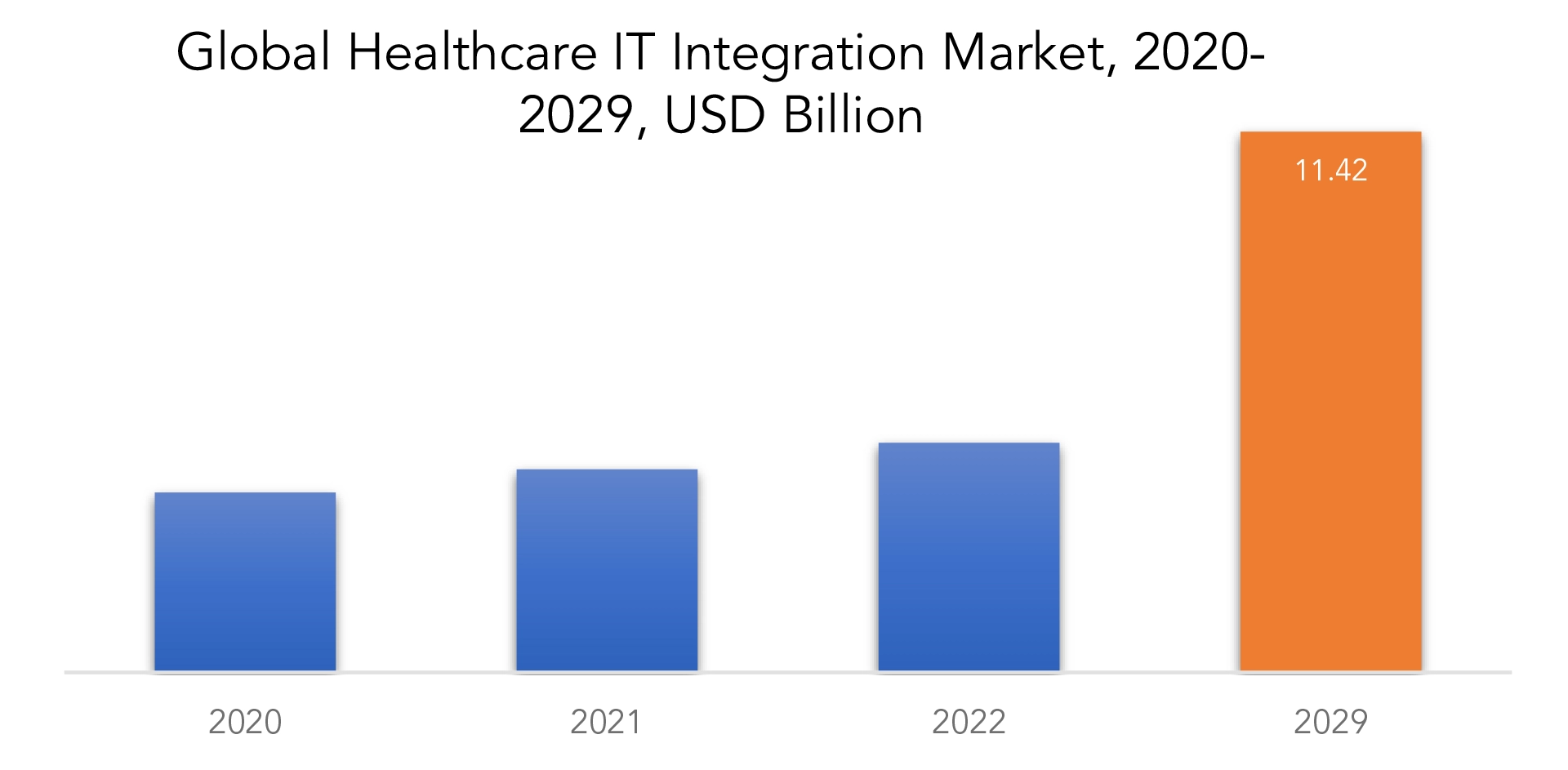

Healthcare IT integration market is expected to grow at 13% CAGR from 2022 to 2029. It was valued 3.80 billion at 2020. It is expected to reach above USD 11.42 billion by 2029.

The use of electronic health records, the rising need for effective healthcare services, and government initiatives to support healthcare IT integration are the main market drivers.

The process of linking various healthcare information systems and apps to build a unified and coordinated infrastructure that enables seamless patient data and information sharing among various healthcare stakeholders and providers is referred to as healthcare IT integration. By improving data administration, lowering mistakes, and providing real-time data access and analysis, healthcare IT integration seeks to optimize clinical workflows, improve patient care, and increase operational efficiency.

Application programming interfaces (APIs), middleware, data integration and management tools, electronic health record (EHR) systems, health information exchanges (HIEs), and interface engines are just a few of the many goods and services that make up the healthcare IT integration sector. These products make it possible for healthcare organisations to handle and integrate data from various sources, including electronic medical records (EMRs), laboratory systems, imaging systems, billing and coding systems, and more.

The market for healthcare IT integration is being propelled by elements like the expanding demand for patient-centered care models, the emergence of advanced technologies like artificial intelligence (AI) and machine learning (ML), and the growing need for interoperability and data exchange. The market is quite competitive, with many vendors providing a wide variety of solutions, and it is anticipated to grow over the next several years as healthcare organisations increase their investment in IT integration to support their aspirations for digital transformation.

The growing desire for interoperability and data exchange across various healthcare systems and platforms is one of several important trends driving the market for healthcare IT integration. Healthcare organisations are increasingly investing in IT integration solutions that enable real-time data sharing and analysis, as well as the seamless coordination of care across various providers and locations, as they aim to enhance patient outcomes and save costs.

The increasing adoption of cloud-based solutions, which provide various advantages like scalability, flexibility, and cost-effectiveness, is another major factor driving the healthcare IT integration market. Healthcare organisations may securely store and access patient data via cloud-based integration solutions from any location, at any time, and on any device, enabling more effective and efficient care delivery. The development of cutting-edge technologies like artificial intelligence (AI) and machine learning (ML), which can assist healthcare organisations in better analyzing and utilizing patient data to improve care outcomes, is also anticipated to fuel the growth of the healthcare IT integration market.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2029 |

| Base year | 2021 |

| Estimated year | 2022 |

| Forecasted year | 2022-2029 |

| Historical period | 2018-2020 |

| Unit | Value (USD Billion, Thousand Units) |

| Segmentation | By Product, By Services, By End User |

| By Product |

|

| By Service |

|

| By End User |

|

| By Region |

|

Healthcare IT Integration Market Segment Analysis

By product the market is segmented into interface/integration engines, medical device integration software, media integration software, other integration tools. By offering the required infrastructure and technology to enable the seamless exchange and management of healthcare data across various systems and platforms, these solutions play a critical role in the development of the healthcare IT integration industry. These technologies enable healthcare organisations to successfully manage and analyze data to support clinical decision-making, care coordination, and patient engagement from a variety of sources, including electronic health records (EHRs), medical devices, and imaging systems. The need for these integration solutions is anticipated to expand in the future years as healthcare organisations continue to prioritize digital transformation and interoperability.

By service the market is segmented into support and maintenance services, implementation and integration services. In order to ensure the successful deployment and operation of integration solutions, support and maintenance services, as well as implementation and integration services, are crucial elements of the healthcare IT integration industry. These services cover things like system setup, testing, troubleshooting, maintenance, and support on an ongoing basis. In the upcoming years, market expansion is anticipated to be driven by rising demand for these services as healthcare organisations embrace more IT integration solutions. Additionally, the success of suppliers and solutions on the market depends critically on the effectiveness and quality of support and implementation services, which can affect the adoption and satisfaction rates of healthcare IT integration solutions.

By end user the market is segmented into hospitals, laboratories, clinics, diagnostic imaging centers, others. By deploying integration solutions to enhance their operations, patient care, and outcomes, hospitals, laboratories, clinics, diagnostic imaging centres, and other healthcare providers play a critical role in fostering the growth of the healthcare IT integration market. These organisations have a variety of needs and demands, from the integration of medical devices and electronic health records (EHR) to interoperability with external stakeholders like insurance companies and public health organisations. As healthcare organisations prioritize digital transformation and data-driven decision-making, the need for IT integration solutions is anticipated to increase, opening up potential for vendors and service providers in the industry.

Healthcare IT Integration Market Key Players

Healthcare IT integration market key players include Epic Systems Corporation, NextGen Healthcare, Inc., Allscripts Healthcare Solutions, Inc., InterSystems Corporation, Oracle Corporation, iNTERFACEWARE Inc., Orion Health Group Ltd., Summit Healthcare Services, Inc., IBM, Capsule Technologies Inc., GE Healthcare, Koninklijke Philips, Lyniate.

Recent Development:

December 09, 2022: Epic Launched Connection Hub: Open to All Developers.

September 14, 2022: NextGen Healthcare Announced New Foster Care Functionality in Behavioral Health Suite.

Who Should Buy? Or Key stakeholders

- Healthcare providers

- Health information exchanges

- Healthcare payers

- Medical device manufacturers

- Healthcare IT vendors and solution providers

- Healthcare regulatory bodies

- Patients

- Healthcare researchers

- Healthcare consultants

- End users

- Government agencies

- Research Organizations

- Others

Healthcare IT Integration Market Regional Analysis

Healthcare IT integration market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).

- North America: includes the US, Canada, Mexico

- Asia Pacific: includes China, Japan, South Korea, India, Australia, ASEAN and Rest of APAC

- Europe: includes UK, Germany, France, Italy, Spain, Russia, and Rest of Europe

- South America: includes Brazil, Argentina and Rest of South America

- Middle East & Africa: includes Turkey, UAE, Saudi Arabia, South Africa, and Rest of MEA

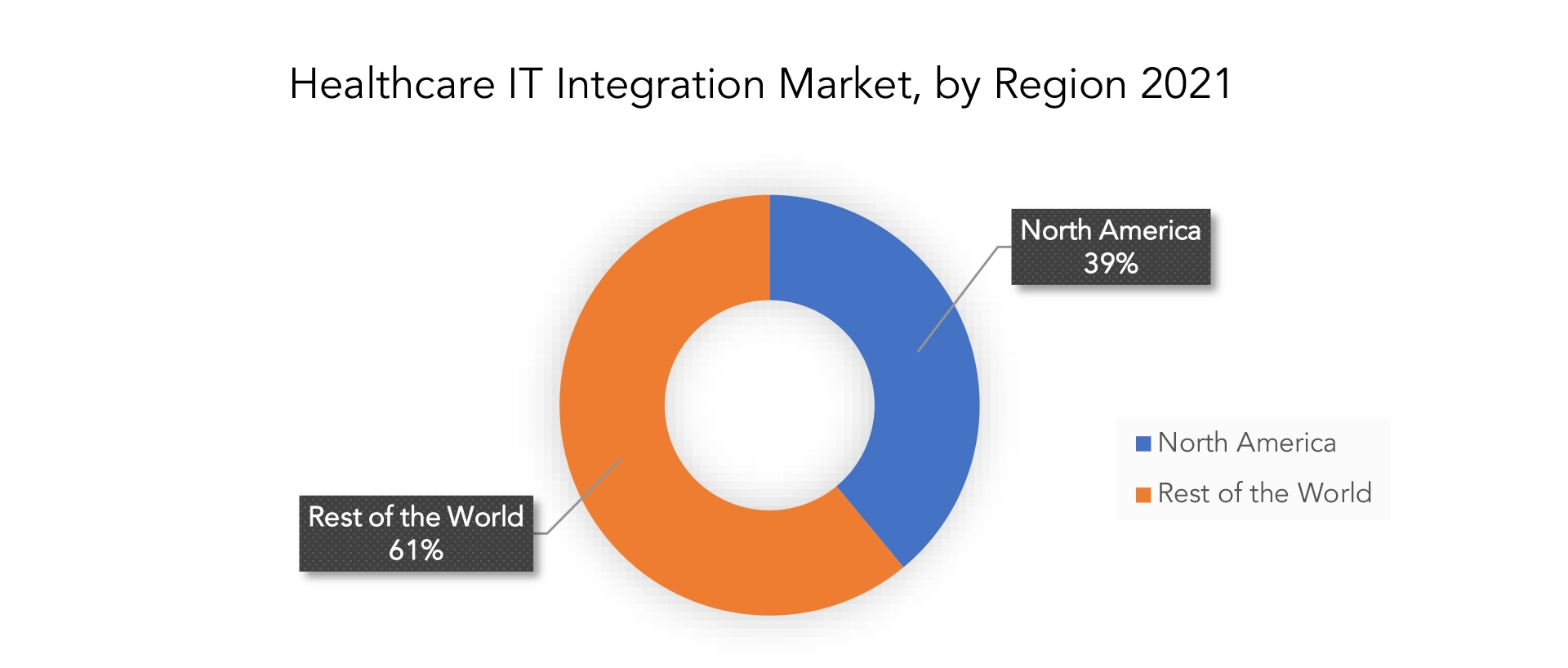

With the greatest market share in 2021, North America dominated the Healthcare IT Integration Market, and it is anticipated that it will continue to do so throughout the forecast period. The region’s superior reimbursement infrastructure and well-established healthcare sector are credited for the dominance. The market for healthcare IT integration is expanding as a result of factors like the expanding use of clinical device connectivity and interoperability solutions to lower rising healthcare costs, as well as the strict regulations and guidelines imposed by various government and non-government authorities like the Federal Communications Commission (FCC) and the Centres for Medicare and Medicaid Services (CMS).

Due to the growing adoption of digital healthcare in the US and the rising investments made by the big firms, the US currently controls the majority of the industry in the North American region. For instance, the Department of Veterans Affairs (VA), Department of Defence (DOD), and Department of Homeland Security’s US Coast Guard (USCG) expanded their joint health information exchange (HIE) network in the 2020 update, according to the Federal Electronic Health Record Modernization (FEHRM) programme office.

Key Market Segments: Healthcare IT Integration Market

Healthcare IT Integration Market By Product, 2020-2029, (USD Billion, Thousand Units)

- Interface/Integration Engines

- Medical Device Integration Software

- Media Integration Software

- Other Integration Tools

Healthcare IT Integration Market By Service, 2020-2029, (USD Billion, Thousand Units)

- Support And Maintenance Services

- Implementation And Integration Services

Healthcare IT Integration Market By End User, 2020-2029, (USD Billion, Thousand Units)

- Hospitals

- Laboratories

- Clinics

- Diagnostic Imaging Centers

- Others

Healthcare IT Integration Market By Region, 2020-2029, (USD Billion, Thousand Units)

- North America

- Asia Pacific

- Europe

- South America

- Middle East And Africa

Important Countries In All Regions Are Covered.

Exactitude Consultancy Services Key Objectives

- Increasing sales and market share

- Developing new technology

- Improving profitability

- Entering new markets

- Enhancing brand reputation

Key Question Answered

- What is the expected growth rate of the healthcare IT integration market over the next 7 years?

- Who are the major players in the healthcare IT integration market and what is their market share?

- What are the end-user industries driving demand for market and what is their outlook?

- What are the opportunities for growth in emerging markets such as asia-pacific, middle east, and africa?

- How is the economic environment affecting the healthcare IT integration market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the healthcare IT integration market?

- What is the current and forecasted size and growth rate of the global healthcare IT integration market?

- What are the key drivers of growth in the healthcare IT integration market?

- Who are the major players in the market and what is their market share?

- What are the distribution channels and supply chain dynamics in the healthcare IT integration market?

- What are the technological advancements and innovations in the healthcare IT integration market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the healthcare IT integration market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the healthcare IT integration market?

- What are the product products and specifications of leading players in the market?

- What is the pricing trend of healthcare IT integration market in the market and what is the impact of raw material prices on the price trend?

Table of Content

- INTRODUCTION

- MARKET DEFINITION

- MARKET SEGMENTATION

- RESEARCH TIMELINES

- ASSUMPTIONS AND LIMITATIONS

- RESEARCH METHODOLOGY

- DATA MINING

- SECONDARY RESEARCH

- PRIMARY RESEARCH

- SUBJECT-MATTER EXPERTS’ ADVICE

- QUALITY CHECKS

- FINAL REVIEW

- DATA TRIANGULATION

- BOTTOM-UP APPROACH

- TOP-DOWN APPROACH

- RESEARCH FLOW

- DATA SOURCES

- DATA MINING

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- GLOBAL HEALTHCARE IT INTEGRATION MARKET OUTLOOK

- MARKET DRIVERS

- MARKET RESTRAINTS

- MARKET OPPORTUNITIES

- IMPACT OF COVID-19 ON HEALTHCARE IT INTEGRATION MARKET

- PORTER’S FIVE FORCES MODEL

- THREAT FROM NEW ENTRANTS

- THREAT FROM SUBSTITUTES

- BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER OF CUSTOMERS

- DEGREE OF COMPETITION

- INDUSTRY VALUE CHAIN ANALYSIS

- GLOBAL HEALTHCARE IT INTEGRATION MARKET OUTLOOK

- GLOBAL HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION, THOUSAND UNITS), 2020-2029

- INTERFACE/INTEGRATION ENGINES

- MEDICAL DEVICE INTEGRATION SOFTWARE

- MEDIA INTEGRATION SOFTWARE

- OTHER INTEGRATION TOOLS

- GLOBAL HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION, THOUSAND UNITS), 2020-2029

- SUPPORT AND MAINTENANCE SERVICES

- IMPLEMENTATION AND INTEGRATION SERVICES

- GLOBAL HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION, THOUSAND UNITS), 2020-2029

- HOSPITALS

- LABORATORIES

- CLINICS

- DIAGNOSTIC IMAGING CENTERS

- OTHERS

- GLOBAL HEALTHCARE IT INTEGRATION MARKET BY REGION (USD BILLION, THOUSAND UNITS), 2020-2029

- NORTH AMERICA

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

- COMPANY PROFILES*(BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCTS OFFERED, RECENT DEVELOPMENTS)

- EPIC SYSTEMS CORPORATION

- NEXTGEN HEALTHCARE, INC.

- ALLSCRIPTS HEALTHCARE SOLUTIONS, INC.

- INTERSYSTEMS CORPORATION

- ORACLE CORPORATION

- INTERFACEWARE INC.

- ORION HEALTH GROUP LTD.

- SUMMIT HEALTHCARE SERVICES, INC.

- IBM

- CAPSULE TECHNOLOGIES INC.

- GE HEALTHCARE

- KONINKLIJKE PHILIPS

- LYNIATE *THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 2 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 3 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 4 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 5 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 6 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 7 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY REGION (USD BILLION), 2020-2029

TABLE 8 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY REGION (THOUSAND UNITS), 2020-2029

TABLE 9 NORTH AMERICA HEALTHCARE IT INTEGRATION BY COUNTRY (USD BILLION), 2020-2029

TABLE 10 NORTH AMERICA HEALTHCARE IT INTEGRATION BY COUNTRY (THOUSAND UNITS), 2020-2029

TABLE 11 NORTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 12 NORTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 13 NORTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 14 NORTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 15 NORTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 16 NORTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY END USER INDUSTRY (THOUSAND UNITS), 2020-2029

TABLE 17 US HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 18 US HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 19 US HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 20 US HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 21 US HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 22 US HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 23 CANADA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 24 CANADA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 25 CANADA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 26 CANADA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 27 CANADA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 28 CANADA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 29 MEXICO HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 30 MEXICO HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 31 MEXICO HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 32 MEXICO HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 33 MEXICO HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 34 MEXICO HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 35 SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 36 SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY COUNTRY (THOUSAND UNITS), 2020-2029

TABLE 37 SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 38 SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 39 SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 40 SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 41 SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 42 SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 43 BRAZIL HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 44 BRAZIL HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 45 BRAZIL HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 46 BRAZIL HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 47 BRAZIL HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 48 BRAZIL HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 49 ARGENTINA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 50 ARGENTINA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 51 ARGENTINA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 52 ARGENTINA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 53 ARGENTINA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 54 ARGENTINA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 55 COLOMBIA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 56 COLOMBIA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 57 COLOMBIA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 58 COLOMBIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 59 COLOMBIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 60 COLOMBIA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 61 COLOMBIA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 62 REST OF SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 63 REST OF SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 64 REST OF SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 65 REST OF SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 66 REST OF SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 67 REST OF SOUTH AMERICA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 68 ASIA-PACIFIC HEALTHCARE IT INTEGRATION MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 69 ASIA-PACIFIC HEALTHCARE IT INTEGRATION MARKET BY COUNTRY (THOUSAND UNITS), 2020-2029

TABLE 70 ASIA-PACIFIC HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 71 ASIA-PACIFIC HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 72 ASIA-PACIFIC HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 73 ASIA-PACIFIC HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 74 ASIA-PACIFIC HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 75 ASIA-PACIFIC HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 76 INDIA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 77 INDIA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 78 INDIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 79 INDIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 80 INDIA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 81 INDIA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 82 CHINA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 83 CHINA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 84 CHINA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 85 CHINA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 86 CHINA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 87 CHINA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 88 JAPAN HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 89 JAPAN HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 90 JAPAN HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 91 JAPAN HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 92 JAPAN HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 93 JAPAN HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 94 SOUTH KOREA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 95 SOUTH KOREA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 96 SOUTH KOREA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 97 SOUTH KOREA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 98 SOUTH KOREA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 99 SOUTH KOREA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 100 AUSTRALIA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 101 AUSTRALIA HEALTHCARE IT INTEGRATION BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 102 AUSTRALIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 103 AUSTRALIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 104 AUSTRALIA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 105 AUSTRALIA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 106 SOUTH EAST ASIA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD MI LLION), 2020-2029

TABLE 107 SOUTH EAST ASIA HEALTHCARE IT INTEGRATION BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 108 SOUTH EAST ASIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 109 SOUTH EAST ASIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 110 SOUTH EAST ASIA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 111 SOUTH EAST ASIA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 112 REST OF ASIA PACIFIC HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 113 REST OF ASIA PACIFIC HEALTHCARE IT INTEGRATION BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 114 REST OF ASIA PACIFIC HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 115 REST OF ASIA PACIFIC HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 116 REST OF ASIA PACIFIC HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 117 REST OF ASIA PACIFIC HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 118 EUROPE HEALTHCARE IT INTEGRATION MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 119 EUROPE HEALTHCARE IT INTEGRATION MARKET BY COUNTRY (THOUSAND UNITS), 2020-2029

TABLE 120 EUROPE HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 121 EUROPE HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 122 EUROPE HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 123 EUROPE HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 124 EUROPE HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 125 EUROPE HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 126 GERMANY HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 127 GERMANY HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 128 GERMANY HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 129 GERMANY HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 130 GERMANY HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 131 GERMANY HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 132 UK HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 133 UK HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 134 UK HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 135 UK HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 136 UK HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 137 UK HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 138 FRANCE HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 139 FRANCE HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 140 FRANCE HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 141 FRANCE HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 142 FRANCE HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 143 FRANCE HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 144 ITALY HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 145 ITALY HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 146 ITALY HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 147 ITALY HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 148 ITALY HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 149 ITALY HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 150 SPAIN HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 151 SPAIN HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 152 SPAIN HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 153 SPAIN HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 154 SPAIN HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 155 SPAIN HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 156 RUSSIA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 157 RUSSIA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 158 RUSSIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 159 RUSSIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 160 RUSSIA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 161 RUSSIA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 162 REST OF EUROPE HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 163 REST OF EUROPE HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 164 REST OF EUROPE HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 165 REST OF EUROPE HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 166 REST OF EUROPE HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 167 REST OF EUROPE HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 168 MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY COUNTRY (USD BILLION), 2020-2029

TABLE 169 MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY COUNTRY (THOUSAND UNITS), 2020-2029

TABLE 170 MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 171 MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 172 MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 173 MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 174 MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 175 MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 176 UAE HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 177 UAE HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 178 UAE HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 179 UAE HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 180 UAE HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 181 UAE HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 182 SAUDI ARABIA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 183 SAUDI ARABIA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 184 SAUDI ARABIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 185 SAUDI ARABIA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 186 SAUDI ARABIA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 187 SAUDI ARABIA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 188 SOUTH AFRICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 189 SOUTH AFRICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 190 SOUTH AFRICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 191 SOUTH AFRICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 192 SOUTH AFRICA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 193 SOUTH AFRICA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

TABLE 194 REST OF MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (USD BILLION), 2020-2029

TABLE 195 REST OF MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY PRODUCT (THOUSAND UNITS), 2020-2029

TABLE 196 REST OF MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (USD BILLION), 2020-2029

TABLE 197 REST OF MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY SERVICE (THOUSAND UNITS), 2020-2029

TABLE 198 REST OF MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY END USER (USD BILLION), 2020-2029

TABLE 199 REST OF MIDDLE EAST AND AFRICA HEALTHCARE IT INTEGRATION MARKET BY END USER (THOUSAND UNITS), 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL HEALTHCARE IT INTEGRATION BY PRODUCT, USD BILLION, 2020-2029

FIGURE 9 GLOBAL HEALTHCARE IT INTEGRATION BY SERVICE, USD BILLION, 2020-2029

FIGURE 10 GLOBAL HEALTHCARE IT INTEGRATION BY END USER, USD BILLION, 2020-2029

FIGURE 11 GLOBAL HEALTHCARE IT INTEGRATION BY REGION, USD BILLION, 2020-2029

FIGURE 12 PORTER’S FIVE FORCES MODEL

FIGURE 13 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY PRODUCT, USD BILLION, 2021

FIGURE 14 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY SERVICE, USD BILLION, 2021

FIGURE 15 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY END USER, USD BILLION, 2021

FIGURE 16 GLOBAL HEALTHCARE IT INTEGRATION MARKET BY REGION, USD BILLION, 2021

FIGURE 17 MARKET SHARE ANALYSIS

FIGURE 18 EPIC SYSTEMS CORPORATION: COMPANY SNAPSHOT

FIGURE 19 NEXTGEN HEALTHCARE, INC: COMPANY SNAPSHOT

FIGURE 20 ALLSCRIPTS HEALTHCARE SOLUTIONS, INC: COMPANY SNAPSHOT

FIGURE 21 INTERSYSTEMS CORPORATION: COMPANY SNAPSHOT

FIGURE 22 ORACLE CORPORATION: COMPANY SNAPSHOT

FIGURE 23 INTERFACEWARE INC: COMPANY SNAPSHOT

FIGURE 24 ORION HEALTH GROUP LTD: COMPANY SNAPSHOT

FIGURE 25 SUMMIT HEALTHCARE SERVICES, INC: COMPANY SNAPSHOT

FIGURE 26 IBM: COMPANY SNAPSHOT

FIGURE 27 CAPSULE TECHNOLOGIES INC: COMPANY SNAPSHOT

FIGURE 28 GE HEALTHCARE: COMPANY SNAPSHOT

FIGURE 29 KONINKLIJKE PHILIPS: COMPANY SNAPSHOT

FIGURE 30 LYNIATE: COMPANY SNAPSHOT

FAQ

Healthcare IT integration market is expected to grow at 7.3% CAGR from 2022 to 2029. it is expected to reach above USD 4.57 billion by 2029

North America held more than 39% of Healthcare IT integration market revenue share in 2021 and will witness expansion in the forecast period.

The use of electronic health records, the rising need for effective healthcare services, and government initiatives to support healthcare IT integration are the main market drivers.

By offering the required infrastructure and technology to enable the seamless exchange and management of healthcare data across various systems and platforms, these solutions play a critical role in the development of the healthcare IT integration industry. These technologies enable healthcare organisations to successfully manage and analyze data to support clinical decision-making, care coordination, and patient engagement from a variety of sources, including electronic health records (EHRs), medical devices, and imaging systems. The need for these integration solutions is anticipated to expand in the future years as healthcare organisations continue to prioritize digital transformation and interoperability.

In-Depth Database

Our Report’s database covers almost all topics of all regions over the Globe.

Recognised Publishing Sources

Tie ups with top publishers around the globe.

Customer Support

Complete pre and post sales

support.

Safe & Secure

Complete secure payment

process.