INTERESTED IN THIS RESEARCH?

Contact our analysts for inquiries, samples, and expert insights.

Report Outlook

| Market Size | CAGR | Dominating Region |

|---|---|---|

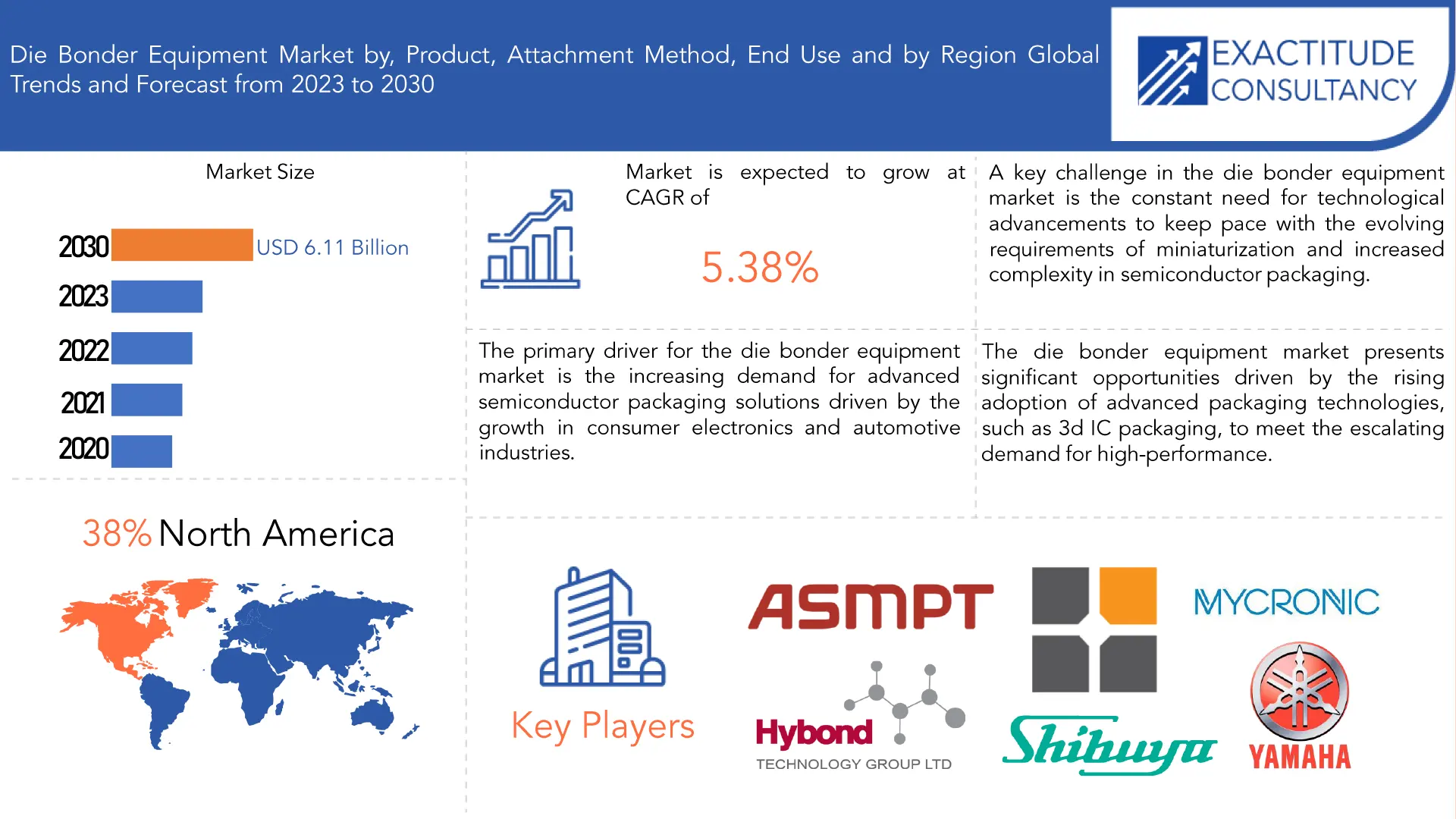

| USD 6.11 Billion by 2030 | 5.38% | North America |

| By Product | By Attachment Method | By End Use |

|---|---|---|

|

|

|

SCOPE OF THE REPORT

Die Bonder Equipment Market Overview

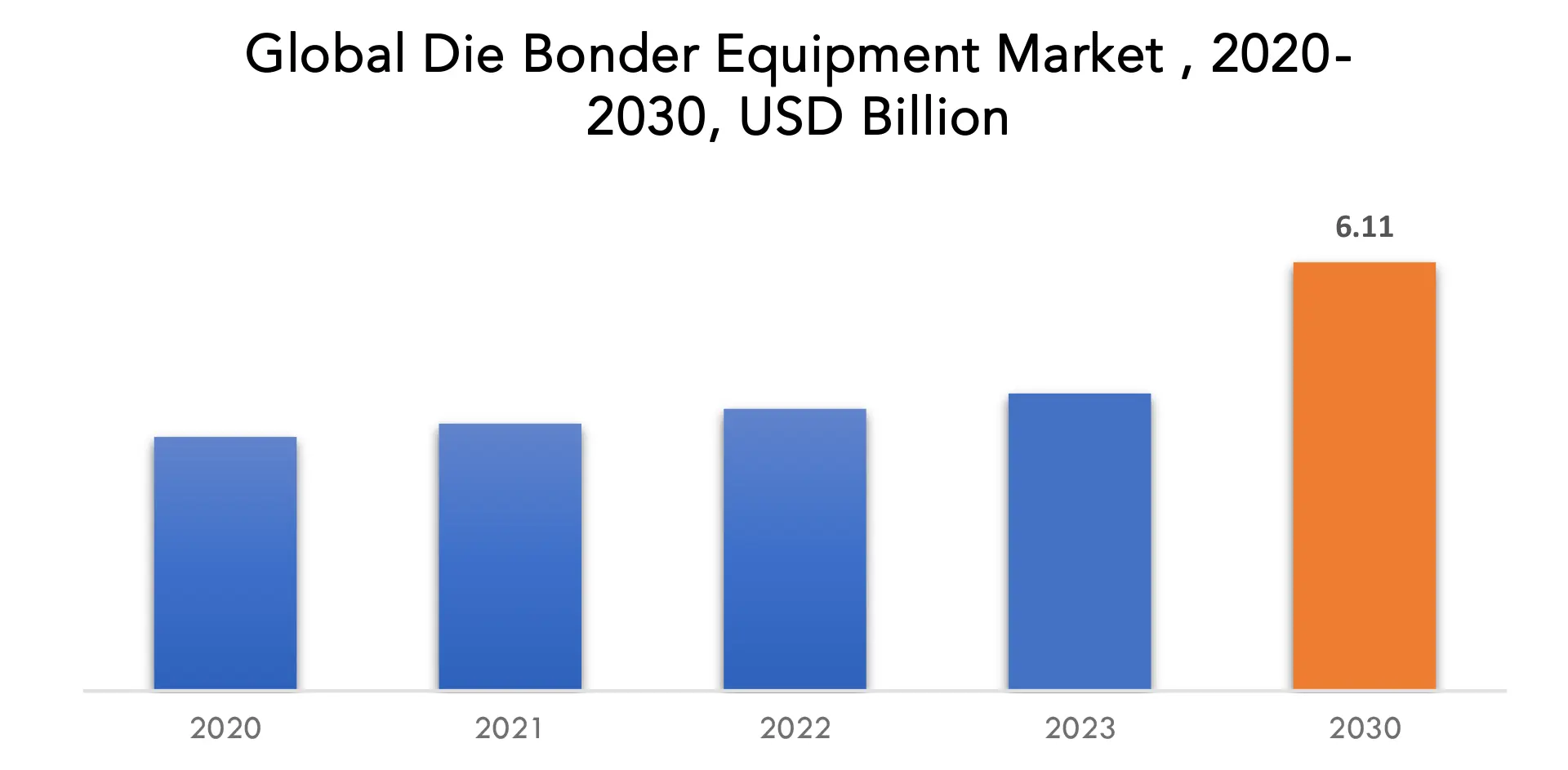

The global die bonder equipment market is anticipated to grow from USD 4.24 Billion in 2023 to USD 6.11 Billion by 2030, at a CAGR of 5.38% during the forecast period.

A type of semiconductor packaging and assembly tool called a die binder is used to attach a chip to a substrate or container. Die bonder equipment is therefore often used in the production of semiconductor devices. Die attachment equipment and die binders are interchangeable terminology. The main function of die attachment equipment is to choose the die from the wafer or waffle tray and attach it to the substrate. A variety of techniques, including flip chip, eutectic, epoxy, and soft solder, are also used to join the die to the substrate. Die bonding is most commonly accomplished by pushing the desired die away from the tape using a pin. Die bonding involves a number of procedures, such as glass/silver-glass bonding, eutectic bonding, soldering, and adhesive bonding.

Due to technical advancements that have made high-end electronic gadgets more accessible to the general public, the semiconductor sector is expanding significantly, which is fueling the demand for die bonder equipment. Electronics goods have shrunk in size over the past few decades, making them lighter, smaller, and more portable. Furthermore, every electronic item has made the switch from analogue to digital. These elements have reduced the cost of electrical equipment. As a result, throughout the past several decades, there has been a massive growth in demand for consumer electronics such as wearables, PCs, tablets, smartphones, augmented and virtual reality devices, and other gadgets. Additionally, the need for very complex semiconductor. The semiconductor business is also being driven by other developments including the increase in automation in various sectors, which has improved industrial processes like manufacturing, warehousing, industrial data management, and other industry 4.0 technologies.

Die bonder equipment is in high demand due to the growing need for electronics products, as these devices are essential for connecting the die to the chip substrate. However, it is projected that factors like the changing cost of raw materials needed to build die bonder equipment and the scarcity of necessary components like silicon would limit the growth of the die bonder equipment market. Furthermore, a significant die bonder equipment market potential for the expansion of the leading companies is the rise in government support for the development of the local semiconductor sector and the growing use of LED circuits. Numerous nations, including the United States, China, India, Japan, South Korea, United Arab Emirates, and others, have revealed numerous financial initiatives for the expansion of the domestic.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2030 |

| Base year | 2022 |

| Estimated year | 2023 |

| Forecasted year | 2023-2030 |

| Historical period | 2019-2021 |

| Unit | Value (USD Billion) (Thousand Units) |

| Segmentation | By Product, By Attachment Method, By End Use and By Region |

| By Product |

|

| By Attachment Method |

|

| By End Use |

|

| By Region |

|

Die Bonder Equipment Market Segmentation Analysis

The Die Bonder Equipment market is divided into four categories: product, attachment method, end use and region. The Die Bonder Equipment market exhibits diverse dynamics, with a range of products including manual, semi-automatic, and fully automatic variants, catering to various attachment methods such as epoxy, eutectic, soft solder, and flip chip, and serving the needs of both Integrated Device Manufacturers (IDMs) and Outsourced Semiconductor Assembly and Test (OSAT) providers.

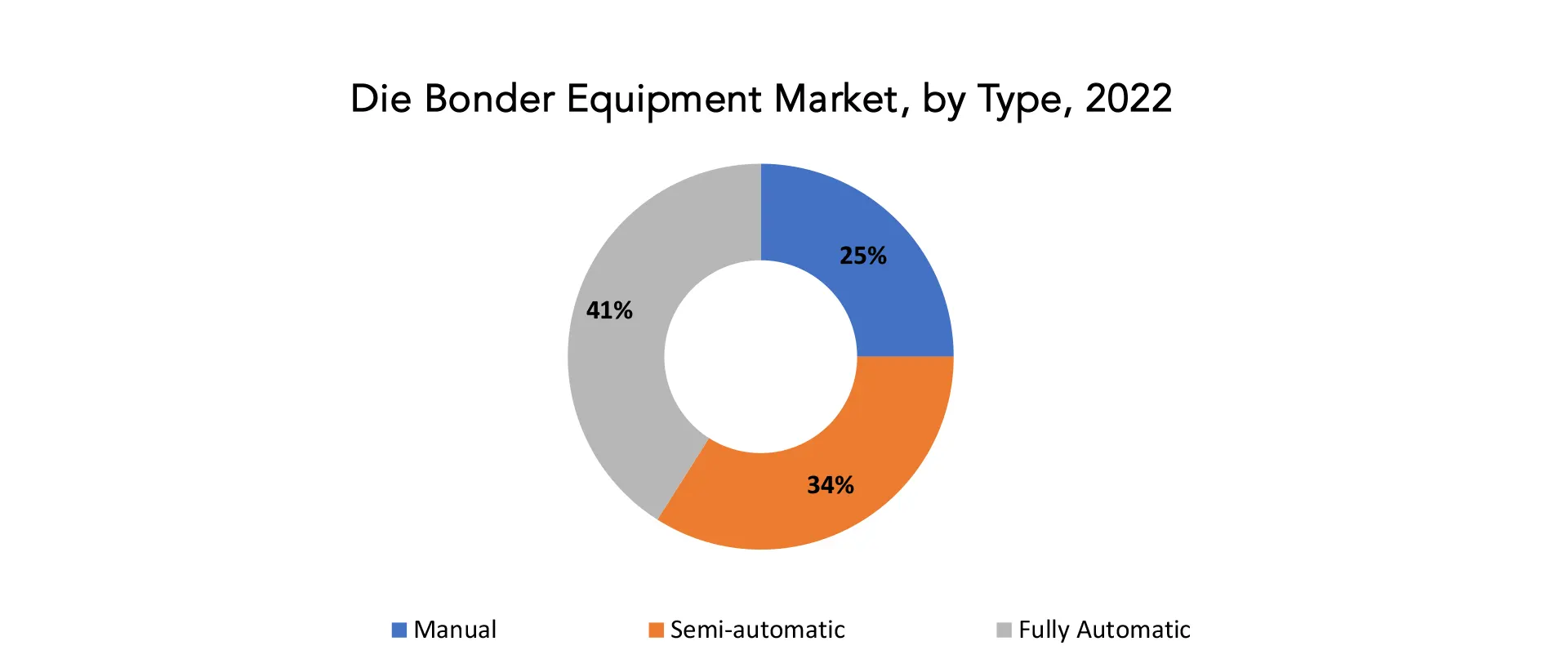

With 41% of the market, the fully automatic die bonder equipment sector is made up of advanced, highly automated semiconductor packing gear. These cutting-edge devices automate every step of the die bonding process, from material handling to accurate die positioning. They perform well in high-throughput applications because integrated vision systems guarantee precision, which makes them essential for modern semiconductor packing methods and mass manufacturing. Fully automated die bonders are widely used in the semiconductor and electronics sectors. Despite the fact that they may need more complicated setup processes and a larger initial investment, they offer enhanced productivity, consistency, and efficiency. Their main benefit is that they can serve large-scale production settings that need accuracy and dependability.

Three product categories comprise the die bonder equipment market. A quarter of the market is made up of manual die bonder equipment, which uses manual procedures to place semiconductor devices onto substrates. These bonders, with their hands-on control and flexibility and accuracy, are perfect for low-volume or research environments. Die bonder equipment that is semi-automatic (34%), balances automated and manual processes. They are appropriate for medium-scale production since operators load substrates and dies manually, with the equipment taking over for perfect bonding. Within the semiconductor packaging sector, this segmentation represents a heterogeneous market that accommodates different production sizes and technological needs.

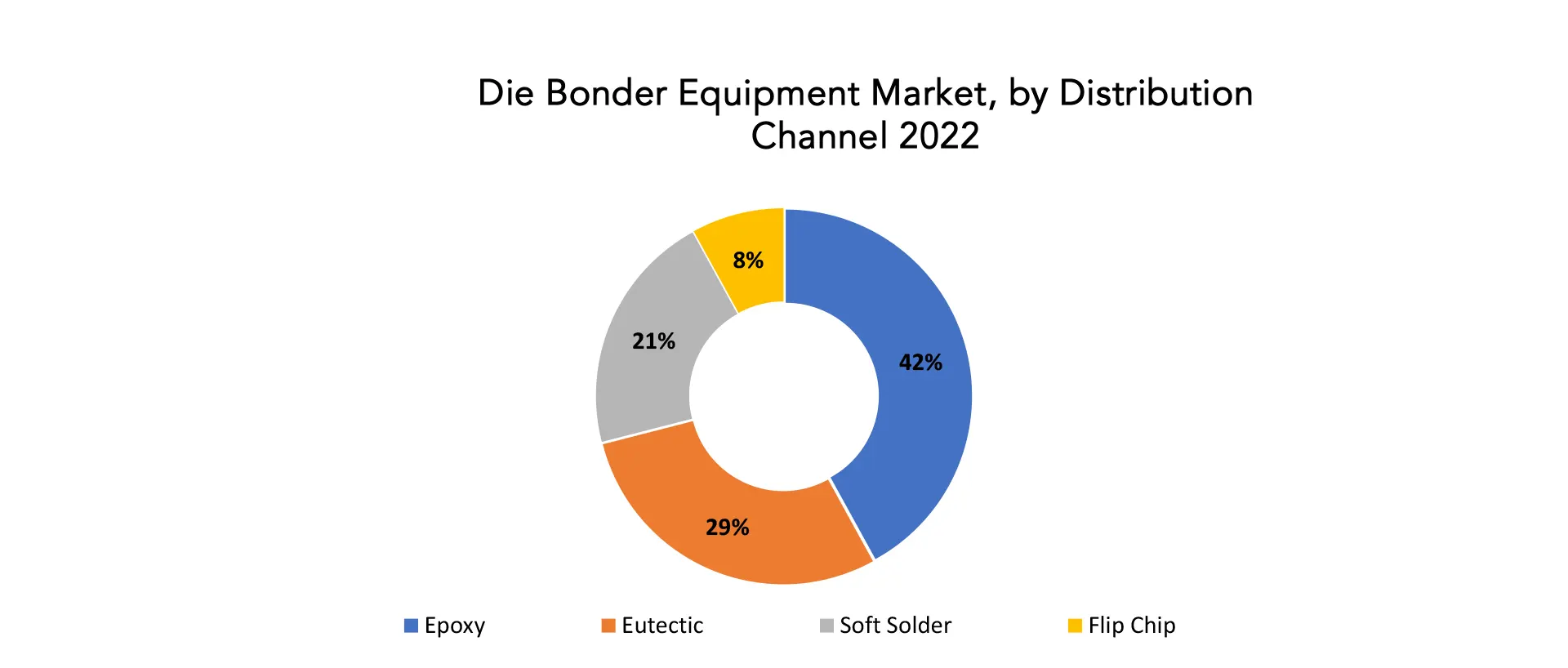

According to the market segmentation by attachment technique, epoxy bonding accounts for 42% of the die bonder equipment market. Epoxy bonding is the process of attaching semiconductor dies to substrates or packaging by utilizing epoxy resin as an adhesive. This technique is well-known for its dependability, robust bond strength, and adaptability to a variety of substrate and die materials. Epoxy bonding is frequently used in integrated circuits and microelectronics, among other semiconductor packaging applications, as it guarantees a strong and durable connection. In the semiconductor sector, where a stable and long-lasting die attachment is essential to the entire functionality and dependability of electronic products, its broad acceptance rate of 42% highlights its importance.

Different approaches are available in the die bonder equipment market, which is classified by attachment method. Eutectic bonding, which involves melting and solidifying alloys simultaneously to provide tight die attachment, accounts for a sizable portion (29%). Twenty-one percent of soldering is done using soft solder bonding, which uses low-temperature solder to connect semiconductor dies to substrates. At 8%, flip chip bonding is a specialized method in which the substrate is directly attached to the semiconductor die after it has been reversed. While Flip Chip is preferred for its small design in cutting-edge semiconductor packing, Eutectic and Soft Solder offer dependability in a variety of electronic devices. Each approach caters to a particular set of application needs. This market segmentation shows how flexible the semiconductor industry’s bonding demands are.

Die Bonder Equipment Market Dynamics

Driver

The proliferation of wireless technologies, such as 5G and Wi-Fi 6, is prompting the development of die bonder equipment optimized for high-frequency.

The die bonder equipment market is undergoing a major shift as a result of the quick spread of wireless technologies, particularly 5G and Wi-Fi 6. Die bonder equipment optimized for high-frequency applications has to be developed in response to the need for improved communication capabilities. Due to the need for accurate and dependable semiconductor component assembly for these cutting-edge wireless technologies, the industry has turned its attention to die bonder equipment that can meet the exacting specifications of high-frequency designs. In order to design die bonders that can handle the complexities of high-frequency materials and guarantee optimal performance in wireless applications, manufacturers are spending in research and development. This pattern highlights how important die bonder equipment is to the smooth integration of parts that are essential to the development of wireless communication technologies, which helps to the evolution and expansion of the broader semiconductor industry.

Restraint

Mechanical unbalance of moving parts is expected to cause a slow-down in die bonder equipment market growth to a certain extent going ahead.

One possible issue that might hinder the die bonder equipment market’s future growth trajectory is the expected mechanical imbalance of moving components. Die bonder machines have complex moving parts for accurate assembly, therefore any mechanical imbalance might result in lower performance and inefficiencies. In the context of semiconductor production, where accuracy is critical, this issue becomes much more important. To maintain the smooth operation of die bonder equipment, modern engineering solutions and ongoing innovation are required to address mechanical imbalance concerns. The industry’s capacity to proactively minimize and manage these mechanical issues will, in part, determine how slowly the market grows. This emphasizes the necessity for strong design approaches and maintenance procedures to uphold die bonder equipment in the evolving landscape of semiconductor manufacturing.

Opportunities

The development of quantum computing and neuromorphic computing, is expected to create new opportunities for the die bonder equipment market.

The market for die bonder equipment may see new opportunities as a result of the development of quantum and neuromorphic computing. There will be an increase in demand for specialized semiconductor components with cutting-edge functionality as these innovative computing paradigms become more popular. Die bonding procedures must be precise in order to support quantum computing, which has special requirements for qubit assembly, and neuromorphic computing, which models brain-inspired architectures. Die bonder equipment designed to meet the unique requirements of both quantum and neuromorphic computing is anticipated to see a rise in use. This offers the die bonder market a chance to be a major player in the manufacturing of parts that are essential to the development of neuromorphic and quantum computing technologies. As the semiconductor industry aligns itself with these transformative computing models, the die bonder equipment market stands poised to capitalize on the demand for high-precision assembly solutions, ushering in a new era of growth and innovation.

Die Bonder Equipment Market Trends

- Increasing Demand for Miniaturization: The relentless pursuit of miniaturization in electronic devices is fueling the need for sophisticated die bonder equipment. Smaller chips require precise placement and bonding techniques to ensure optimal performance and yield. This trend is particularly evident in the mobile electronics and Internet of Things (IoT) sectors.

- Rise of 3D Packaging and Heterogeneous Integration: Traditional die stacking methods are giving way to more complex 3D packaging solutions. These involve stacking multiple dies vertically, enabling increased functionality and performance in a smaller footprint. Die bonder equipment needs to adapt to handle the challenges of bonding dissimilar materials and complex chip geometries.

- Adoption of Advanced Technologies: Artificial intelligence (AI) and machine learning (ML) are making inroads into die bonder equipment. These technologies are used for process optimization, real-time defect detection, and predictive maintenance. Additionally, the integration of robotics is enhancing automation and precision in the bonding process.

- Growing demand for flip-chip technology: This method offers advantages like improved thermal performance and higher density, but requires specialized die bonder equipment for precise alignment and bonding.

- Integration of sensors and vision systems: These technologies enable real-time monitoring and control of the bonding process, further enhancing accuracy and yield.

Competitive Landscape

The competitive landscape of the die bonder equipment market was dynamic, with several prominent companies competing to provide innovative and die bonder equipment.

- ASMPT Ltd.

- BE Semiconductor Industries NV

- DIAS Automation HK Ltd.

- Tresky AG

- ficonTEC Service GmbH

- Finetech GmbH and Co. KG

- Four Technos Co. Ltd.

- HYBOND Inc.

- Indubond

- Kulicke and Soffa Industries Inc.

- MicroAssembly Technologies Ltd.

- Mycronic AB

- Palomar Technologies Inc.

- Panasonic Holdings Corp.

- Paroteq GmbH

- SHIBUYA Corp.

- UniTemp GmbH

- WestBond Inc.

- Yamaha Motor Co. Ltd.

- SHIBAURA MECHATRONICS CORP.

Recent Developments:

27 November 2023 – Yamaha Motor Co., Ltd. announced that the Company is adding the new clean type YK-XEC series to its YK-XE series – high operational and cost performance SCARA robots. This model is ideal for automated work in clean rooms and will be released on a rolling basis starting February 1, 2024.

21 APRIL 2022 – The Hong Kong Applied Science and Technology Research Institute (ASTRI), ASM Pacific Technology Limited (ASMPT) and Alpha Power Solutions Co., Ltd. (APS) announced that they are jointly developing the industry’s first ‘Made in Hong Kong’ Silicon Carbide (SiC) Intelligent Power Module (IPM) for electric vehicles (EVs).

Regional Analysis

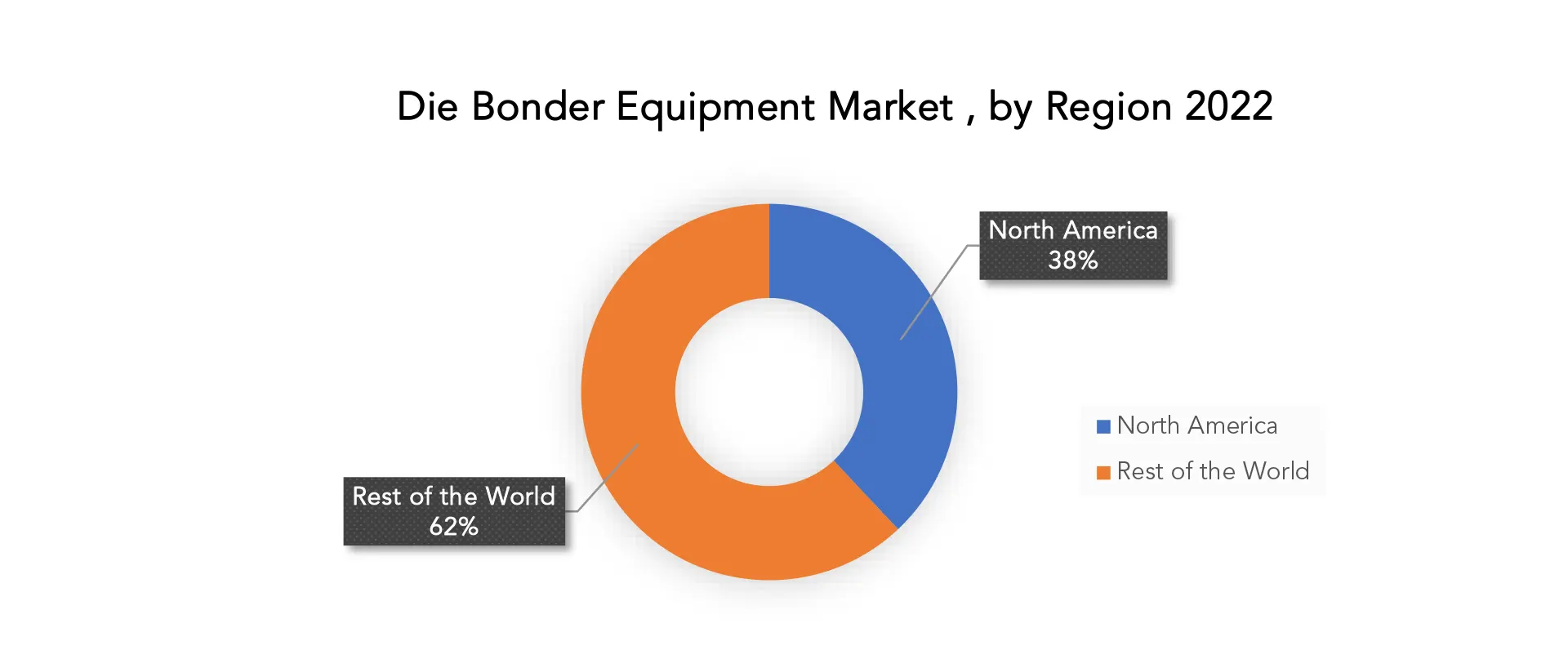

With the greatest revenue share of 38%, North America emerged as the leading market for die bonder equipment in 2022. The existence of significant manufacturing businesses and the growing demand for tablets and smartphones are the primary reasons for the revenue growth in the North American market. Numerous top semiconductor firms and electronics manufacturers are based in North America. The area has a strong supply chain for tools and materials, a trained workforce, and research and development facilities. It also has a well-established infrastructure for the production of electronics. Companies in North America place a high priority on technology and make significant investments in the creation of innovative die bonding technologies, which fuels market expansion. In addition to consumer electronics, North America boasts robust aerospace, defense, and medical device sectors that significantly depend on cutting-edge die bonding technology for a range of uses.

Over the course of the forecast period, the die bonder equipment market in Asia Pacific is anticipated to develop at the quickest rate. Major drivers propelling the growth of the APAC market include increased disposable income, rapid urbanisation, and a considerable increase in population that is increasing demand for electronic equipment, particularly in emerging nations like India, China, Malaysia, and Indonesia. Because there are several reputable integrated circuit (IC) manufacturers in the Asia Pacific area, die bonder equipment is anticipated to be in high demand in this market.

Target Audience for Die Bonder Equipment Market

- Semiconductor Manufacturers

- Integrated Device Manufacturers (IDMs)

- Outsourced Semiconductor Assembly and Test (OSAT) Providers

- Research and Development Institutions

- Electronics Manufacturing Companies

- Quantum Computing and Neuromorphic Computing Developers

- Original Equipment Manufacturers (OEMs)

- Technology Enthusiasts and Innovators

- Government Agencies and Regulatory Bodies

- Investors and Financial Institutions in Technology Sector

Import & Export Data for Die Bonder Equipment Market

Exactitude consultancy provides import and export data for the recent years. It also offers insights on production and consumption volume of the product. Understanding the import and export data is pivotal for any player in the die bonder equipment market. This knowledge equips businesses with strategic advantages, such as:

- Identifying emerging markets with untapped potential.

- Adapting supply chain strategies to optimize cost-efficiency and market responsiveness.

- Navigating competition by assessing major players’ trade dynamics.

Key insights

- Trade volume trends: our report dissects import and export data spanning the last five years to reveal crucial trends and growth patterns within the global die bonder equipment market. This data-driven exploration empowers readers with a deep understanding of the market’s trajectory.

- Market players: gain insights into the leading players driving the pet relaxant trade. From established giants to emerging contenders, our analysis highlights the key contributors to the import and export landscape.

- Geographical dynamics: delve into the geographical distribution of trade activities. Uncover which regions dominate exports and which ones hold the reins on imports, painting a comprehensive picture of the industry’s global footprint.

- Product breakdown: by segmenting data based on die bonder equipment types –– we provide a granular view of trade preferences and shifts, enabling businesses to align strategies with the evolving technological landscape.

Import and export data is crucial in reports as it offers insights into global market trends, identifies emerging opportunities, and informs supply chain management. By analyzing trade flows, businesses can make informed decisions, manage risks, and tailor strategies to changing demand. This data aids governments in policy formulation and trade negotiations, while investors use it to assess market potential. Moreover, import and export data contributes to economic indicators, influences product innovation, and promotes transparency in international trade, making it an essential component for comprehensive and informed analyses.

Segments Covered in the Die Bonder Equipment Market Report

Die Bonder Equipment Market by Product

- Manual

- Semi-automatic

- Fully Automatic

Die Bonder Equipment Market by Attachment Method

- Epoxy

- Eutectic

- Soft Solder

- Flip Chip

Die Bonder Equipment Market by End Use

- Integrated Device Manufacturers (IDMs)

- Outsourced Semiconductor Assembly and Test (OSAT)

Die Bonder Equipment Market by Region

- North America

- Europe

- Asia Pacific

- South America

- Middle East and Africa

Key Question Answered

- What is the expected growth rate of the Die Bonder Equipment market over the next 7 years?

- Who are the major players in the Die Bonder Equipment market and what is their market share?

- What are the end-user industries driving market demand and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-pacific, the middle east, and Africa?

- How is the economic environment affecting the Die Bonder Equipment market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the Die Bonder Equipment market?

- What is the current and forecasted size and growth rate of the Die Bonder Equipment market?

- What are the key drivers of growth in the Die Bonder Equipment market?

- Who are the major players in the market and what is their market share?

- What are the distribution channels and supply chain dynamics in the Die Bonder Equipment market?

- What are the technological advancements and innovations in the Die Bonder Equipment market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the Die Bonder Equipment market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the Die Bonder Equipment market?

- What is the product offered and specifications of leading players in the market?

Table of Content

- INTRODUCTION

- MARKET DEFINITION

- MARKET SEGMENTATION

- RESEARCH TIMELINES

- ASSUMPTIONS AND LIMITATIONS

- RESEARCH METHODOLOGY

- DATA MINING

- SECONDARY RESEARCH

- PRIMARY RESEARCH

- SUBJECT-MATTER EXPERTS’ ADVICE

- QUALITY CHECKS

- FINAL REVIEW

- DATA TRIANGULATION

- BOTTOM-UP APPROACH

- TOP-DOWN APPROACH

- RESEARCH FLOW

- DATA PRODUCTS

- DATA MINING

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- DIE BONDER EQUIPMENT MARKET OUTLOOK

- MARKET DRIVERS

- MARKET RESTRAINTS

- MARKET OPPORTUNITIES

- IMPACT OF COVID-19 ON DIE BONDER EQUIPMENT MARKET

- PORTER’S FIVE FORCES MODEL

- THREAT FROM NEW ENTRANTS

- THREAT FROM SUBSTITUTES

- BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER OF CUSTOMERS

- DEGREE OF COMPETITION

- INDUSTRY VALUE CHAIN ANALYSIS

- DIE BONDER EQUIPMENT MARKET OUTLOOK

- GLOBAL DIE BONDER EQUIPMENT MARKET BY PRODUCT, 2020-2030, (USD BILLION) (THOUSAND UNITS)

- MANUAL

- SEMI-AUTOMATIC

- FULLY AUTOMATIC

- GLOBAL DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD, 2020-2030, (USD BILLION) (THOUSAND UNITS)

- EPOXY

- EUTECTIC

- SOFT SOLDER

- FLIP CHIP

- GLOBAL DIE BONDER EQUIPMENT MARKET BY END USE, 2020-2030, (USD BILLION) (THOUSAND UNITS)

- INTEGRATED DEVICE MANUFACTURERS (IDMS)

- OUTSOURCED SEMICONDUCTOR ASSEMBLY AND TEST (OSAT)

- GLOBAL DIE BONDER EQUIPMENT MARKET BY REGION, 2020-2030, (USD BILLION) (THOUSAND UNITS)

- NORTH AMERICA

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

- COMPANY PROFILES*

(BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCTS OFFERED, RECENT DEVELOPMENTS)

- ASMPT LTD.

- BE SEMICONDUCTOR INDUSTRIES NV

- DIAS AUTOMATION HK LTD.

- TRESKY AG

- FICONTEC SERVICE GMBH

- FINETECH GMBH AND CO. KG

- FOUR TECHNOS CO. LTD.

- HYBOND INC.

- INDUBOND

- KULICKE AND SOFFA INDUSTRIES INC.

- MICROASSEMBLY TECHNOLOGIES LTD.

- MYCRONIC AB

- PALOMAR TECHNOLOGIES INC.

- PANASONIC HOLDINGS CORP.

- PAROTEQ GMBH

- SHIBUYA CORP.

- UNITEMP GMBH

- WESTBOND INC.

- YAMAHA MOTOR CO. LTD.

- SHIBAURA MECHATRONICS CORP.

*THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 2 GLOBAL DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 3 GLOBAL DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 4 GLOBAL DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 5 GLOBAL DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 6 GLOBAL DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 7 GLOBAL DIE BONDER EQUIPMENT MARKET BY REGION (USD BILLION) 2020-2030

TABLE 8 GLOBAL DIE BONDER EQUIPMENT MARKET BY REGION (THOUSAND UNITS) 2020-2030

TABLE 9 NORTH AMERICA DIE BONDER EQUIPMENT MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 10 NORTH AMERICA DIE BONDER EQUIPMENT MARKET BY COUNTRY (THOUSAND UNITS) 2020-2030

TABLE 11 NORTH AMERICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 12 NORTH AMERICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 13 NORTH AMERICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 14 NORTH AMERICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 15 NORTH AMERICA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 16 NORTH AMERICA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 17 US DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 18 US DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 19 US DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 20 US DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 21 US DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 22 US DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 23 CANADA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 24 CANADA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 25 CANADA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 26 CANADA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 27 CANADA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 28 CANADA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 29 MEXICO DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 30 MEXICO DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 31 MEXICO DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 32 MEXICO DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 33 MEXICO DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 34 MEXICO DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 35 SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 36 SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY COUNTRY (THOUSAND UNITS) 2020-2030

TABLE 37 SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 38 SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 39 SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 40 SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 41 SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 42 SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 43 BRAZIL DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 44 BRAZIL DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 45 BRAZIL DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 46 BRAZIL DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 47 BRAZIL DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 48 BRAZIL DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 49 ARGENTINA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 50 ARGENTINA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 51 ARGENTINA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 52 ARGENTINA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 53 ARGENTINA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 54 ARGENTINA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 55 COLOMBIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 56 COLOMBIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 57 COLOMBIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 58 COLOMBIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 59 COLOMBIA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 60 COLOMBIA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 61 REST OF SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 62 REST OF SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 63 REST OF SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 64 REST OF SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 65 REST OF SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 66 REST OF SOUTH AMERICA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 67 ASIA-PACIFIC DIE BONDER EQUIPMENT MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 68 ASIA-PACIFIC DIE BONDER EQUIPMENT MARKET BY COUNTRY (THOUSAND UNITS) 2020-2030

TABLE 69 ASIA-PACIFIC DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 70 ASIA-PACIFIC DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 71 ASIA-PACIFIC DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 72 ASIA-PACIFIC DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 73 ASIA-PACIFIC DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 74 ASIA-PACIFIC DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 75 INDIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 76 INDIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 77 INDIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 78 INDIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 79 INDIA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 80 INDIA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 81 CHINA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 82 CHINA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 83 CHINA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 84 CHINA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 85 CHINA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 86 CHINA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 87 JAPAN DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 88 JAPAN DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 89 JAPAN DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 90 JAPAN DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 91 JAPAN DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 92 JAPAN DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 93 SOUTH KOREA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 94 SOUTH KOREA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 95 SOUTH KOREA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 96 SOUTH KOREA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 97 SOUTH KOREA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 98 SOUTH KOREA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 99 AUSTRALIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 100 AUSTRALIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 101 AUSTRALIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 102 AUSTRALIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 103 AUSTRALIA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 104 AUSTRALIA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 105 SOUTH-EAST ASIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 106 SOUTH-EAST ASIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 107 SOUTH-EAST ASIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 108 SOUTH-EAST ASIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 109 SOUTH-EAST ASIA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 110 SOUTH-EAST ASIA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 111 REST OF ASIA PACIFIC DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 112 REST OF ASIA PACIFIC DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 113 REST OF ASIA PACIFIC DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 114 REST OF ASIA PACIFIC DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 115 REST OF ASIA PACIFIC DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 116 REST OF ASIA PACIFIC DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 117 EUROPE DIE BONDER EQUIPMENT MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 118 EUROPE DIE BONDER EQUIPMENT MARKET BY COUNTRY (THOUSAND UNITS) 2020-2030

TABLE 119 EUROPE DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 120 EUROPE DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 121 EUROPE DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 122 EUROPE DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 123 EUROPE DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 124 EUROPE DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 125 GERMANY DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 126 GERMANY DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 127 GERMANY DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 128 GERMANY DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 129 GERMANY DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 130 GERMANY DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 131 UK DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 132 UK DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 133 UK DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 134 UK DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 135 UK DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 136 UK DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 137 FRANCE DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 138 FRANCE DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 139 FRANCE DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 140 FRANCE DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 141 FRANCE DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 142 FRANCE DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 143 ITALY DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 144 ITALY DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 145 ITALY DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 146 ITALY DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 147 ITALY DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 148 ITALY DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 149 SPAIN DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 150 SPAIN DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 151 SPAIN DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 152 SPAIN DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 153 SPAIN DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 154 SPAIN DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 155 RUSSIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 156 RUSSIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 157 RUSSIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 158 RUSSIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 159 RUSSIA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 160 RUSSIA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 161 REST OF EUROPE DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 162 REST OF EUROPE DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 163 REST OF EUROPE DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 164 REST OF EUROPE DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 165 REST OF EUROPE DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 166 REST OF EUROPE DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 167 MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 168 MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY COUNTRY (THOUSAND UNITS) 2020-2030

TABLE 169 MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 170 MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 171 MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 172 MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 173 MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 174 MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 175 UAE DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 176 UAE DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 177 UAE DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 178 UAE DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 179 UAE DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 180 UAE DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 181 SAUDI ARABIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 182 SAUDI ARABIA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 183 SAUDI ARABIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 184 SAUDI ARABIA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 185 SAUDI ARABIA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 186 SAUDI ARABIA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 187 SOUTH AFRICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 188 SOUTH AFRICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 189 SOUTH AFRICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 190 SOUTH AFRICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 191 SOUTH AFRICA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 192 SOUTH AFRICA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

TABLE 193 REST OF MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 194 REST OF MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY PRODUCT (THOUSAND UNITS) 2020-2030

TABLE 195 REST OF MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (USD BILLION) 2020-2030

TABLE 196 REST OF MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD (THOUSAND UNITS) 2020-2030

TABLE 197 REST OF MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY END USE (USD BILLION) 2020-2030

TABLE 198 REST OF MIDDLE EAST AND AFRICA DIE BONDER EQUIPMENT MARKET BY END USE (THOUSAND UNITS) 2020-2030

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL DIE BONDER EQUIPMENT MARKET BY PRODUCT USD BILLION, 2020-2030

FIGURE 9 GLOBAL DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD USD BILLION, 2020-2030

FIGURE 10 GLOBAL DIE BONDER EQUIPMENT MARKET BY END USE, USD BILLION, 2020-2030

FIGURE 11 GLOBAL DIE BONDER EQUIPMENT MARKET BY REGION, USD BILLION, 2020-2030

FIGURE 12 PORTER’S FIVE FORCES MODEL

FIGURE 13 GLOBAL DIE BONDER EQUIPMENT MARKET BY PRODUCT USD BILLION, 2022

FIGURE 14 GLOBAL DIE BONDER EQUIPMENT MARKET BY ATTACHMENT METHOD, USD BILLION, 2022

FIGURE 15 GLOBAL DIE BONDER EQUIPMENT MARKET BY END USE, USD BILLION, 2022

FIGURE 16 GLOBAL DIE BONDER EQUIPMENT MARKET BY REGION, USD BILLION, 2022

FIGURE 17 MARKET SHARE ANALYSIS

FIGURE 18 ASMPT LTD.: COMPANY SNAPSHOT

FIGURE 19 BE SEMICONDUCTOR INDUSTRIES NV: COMPANY SNAPSHOT

FIGURE 20 DIAS AUTOMATION HK LTD.: COMPANY SNAPSHOT

FIGURE 21 DR. TRESKY AG: COMPANY SNAPSHOT

FIGURE 22 FICONTEC SERVICE GMBH: COMPANY SNAPSHOT

FIGURE 23 FINETECH GMBH AND CO. KG: COMPANY SNAPSHOT

FIGURE 24 FOUR TECHNOS CO. LTD.: COMPANY SNAPSHOT

FIGURE 25 HYBOND INC.: COMPANY SNAPSHOT

FIGURE 26 INDUBOND: COMPANY SNAPSHOT

FIGURE 27 KULICKE AND SOFFA INDUSTRIES INC.: COMPANY SNAPSHOT

FIGURE 28 MICROASSEMBLY TECHNOLOGIES LTD.: COMPANY SNAPSHOT

FIGURE 29 MYCRONIC AB: COMPANY SNAPSHOT

FIGURE 30 PALOMAR TECHNOLOGIES INC.: COMPANY SNAPSHOT

FIGURE 31 PANASONIC HOLDINGS CORP.: COMPANY SNAPSHOT

FIGURE 32 PAROTEQ GMBH: COMPANY SNAPSHOT

FIGURE 33 SHIBUYA CORP.: COMPANY SNAPSHOT

FIGURE 34 UNITEMP GMBH: COMPANY SNAPSHOT

FIGURE 35 WESTBOND INC.: COMPANY SNAPSHOT

FIGURE 36 YAMAHA MOTOR CO. LTD.: COMPANY SNAPSHOT

FIGURE 37 SHIBAURA MECHATRONICS CORP.: COMPANY SNAPSHOT

FAQ

The global die bonder equipment market is anticipated to grow from USD 4.24 Billion in 2023 to USD 6.11 Billion by 2030, at a CAGR of 5.38% during the forecast period.

North America accounted for the largest market in the Die Bonder Equipment market. North America accounted for 38% market share of the global market value.

ASMPT Ltd., BE Semiconductor Industries NV, DIAS Automation HK Ltd., Dr. Tresky AG, ficonTEC Service GmbH, Finetech GmbH and Co. KG, Four Technos Co. Ltd., HYBOND Inc., Indubond, Kulicke and Soffa Industries Inc., MicroAssembly Technologies Ltd., Mycronic AB, Palomar Technologies Inc., Panasonic Holdings Corp., Paroteq GmbH, SHIBUYA Corp., UniTemp GmbH, WestBond Inc., Yamaha Motor Co. Ltd., SHIBAURA MECHATRONICS CORP.

Growing demand for flip-chip technology: This method offers advantages like improved thermal performance and higher density, but requires specialized die bonder equipment for precise alignment and bonding.

In-Depth Database

Our Report’s database covers almost all topics of all regions over the Globe.

Recognised Publishing Sources

Tie ups with top publishers around the globe.

Customer Support

Complete pre and post sales

support.

Safe & Secure

Complete secure payment

process.