INTERESTED IN THIS RESEARCH?

Contact our analysts for inquiries, samples, and expert insights.

REPORT OUTLOOK

| Market Size | CAGR | Dominating Region |

|---|---|---|

| USD 62.07 Billion by 2030 | 31.50 % | North America |

| by Type | by Farming Environment | by End-use Application |

|---|---|---|

|

|

|

SCOPE OF THE REPORT

Agriculture Robots Market Overview

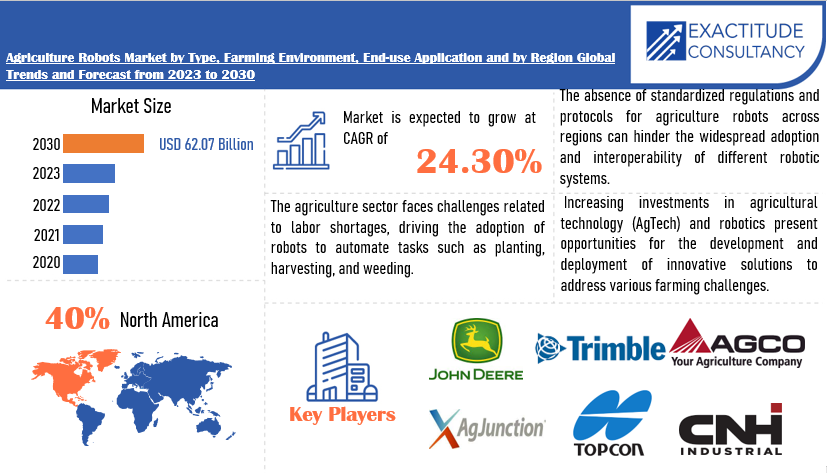

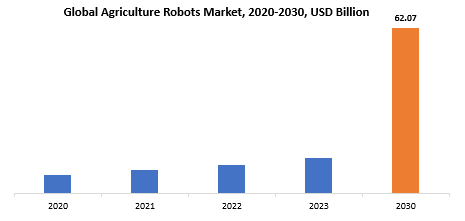

The global agriculture robots market is anticipated to grow from USD 13.54 Billion in 2023 to USD 62.07 Billion by 2030, at a CAGR of 31.50 % during the forecast period.

Agriculture robots, also known as agri-robots or agbots, represent a transformative technological advancement in the field of agriculture. These robots are designed and deployed to perform a variety of tasks across different stages of the agricultural cycle, aiming to enhance efficiency, productivity, and sustainability in farming practices. Agriculture robots can be classified into various types, each serving specific purposes such as precision farming, planting, harvesting, weeding, and monitoring crop health. Equipped with advanced technologies, including sensors, GPS systems, and machine learning algorithms, these robots enable farmers to automate traditionally labor-intensive tasks, optimize resource utilization, and make data-driven decisions.

Precision agriculture, enabled by agriculture robots, allows for targeted and controlled farming practices, minimizing environmental impact and maximizing yield. From autonomous tractors and drones to robotic arms for picking fruits, agriculture robots contribute to overcoming challenges such as labor shortages, rising global food demand, and the need for sustainable farming practices. The integration of robotics in agriculture signifies a shift towards smart farming, where technology plays a pivotal role in reshaping and modernizing traditional farming methods to meet the demands of a rapidly evolving world.

The increasing global population has led to a rising demand for food, necessitating higher agricultural productivity. Agriculture robots address this need by offering efficient and automated solutions for various farming tasks. Precision agriculture is another driving factor, where farmers seek to optimize resource usage and minimize environmental impact. Agriculture robots equipped with advanced sensors and imaging technologies contribute to precision farming, allowing for targeted and data-driven decision-making.

Labor shortages in the agriculture sector are a significant driver, prompting the adoption of robots to perform tasks such as planting, harvesting, and weeding. As traditional farming practices face challenges in securing an adequate workforce, robots provide a solution for maintaining and increasing productivity. Moreover, continuous technological advancements, including developments in artificial intelligence, machine learning, and robotics, contribute to the sophistication of agriculture robots. These technological enhancements result in robots that are more capable, efficient, and adaptable to diverse farming environments.

Environmental concerns and the need for sustainable agriculture practices also drive the adoption of agriculture robots. These robots enable farmers to implement eco-friendly and precise farming methods, reducing the use of pesticides and optimizing resource utilization. Governments and agricultural organizations supporting the integration of advanced technologies in farming through subsidies and incentives further propel the market.

Agriculture robots play a pivotal role in meeting this demand by offering automated and efficient solutions across various farming activities. Moreover, the Agriculture Robots market is crucial for mitigating labor challenges in the agriculture sector. As traditional farming faces labor shortages and an aging workforce, robots provide a viable solution to perform labor-intensive tasks such as planting, harvesting, and weeding.

The adoption of agriculture robots is essential for the advancement of precision agriculture. By leveraging advanced technologies like sensors, GPS, and artificial intelligence, these robots enable precise and data-driven decision-making. They contribute to optimized resource utilization, reduced environmental impact, and increased crop yield. This emphasis on precision agriculture aligns with the broader goal of sustainable farming practices, making agriculture robots instrumental in fostering environmental stewardship.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2030 |

| Base year | 2022 |

| Estimated year | 2023 |

| Forecasted year | 2023-2030 |

| Historical period | 2019-2021 |

| Unit | Value (USD Billion) Volume (Thousand Units) |

| Segmentation | By Type, Farming Environment, End-use Application and Region |

|

By Type |

|

|

By End-use Application |

|

|

By Farming Environment |

|

|

By Region

|

|

Agriculture Robots Market Segmentation Analysis

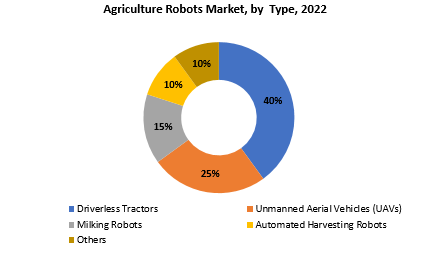

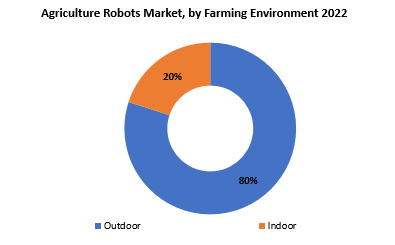

The global Agriculture Robots market is divided into three segments, type, End-use Application, Farming Environment and region. By type the market is divided Driverless Tractors, Unmanned Aerial Vehicles (UAVs), Milking Robots, Automated Harvesting Robots, Others. By End-use Application the market is classified into Field Farming, Harvest Management, Livestock Management, Other Applications. By Farming Environment, the market is classified into Outdoor, Indoor.

Based on type, driverless tractors segment dominating in the agriculture robots market. The driverless tractors segment stands out as a dominant force in the agriculture robots market, spearheading the transformation of traditional farming practices. These advanced autonomous vehicles represent a significant technological leap in the agriculture sector, offering a range of benefits that contribute to their dominance. Driverless tractors leverage cutting-edge technologies such as GPS, sensors, and artificial intelligence to operate autonomously in the field.

The key factors driving the dominance of driverless tractors is their ability to address the pressing issue of labor shortages in agriculture. As the availability of skilled labor for farming tasks becomes increasingly scarce, autonomous tractors provide a reliable solution for performing essential activities such as plowing, seeding, and harvesting without the need for human intervention. Precision agriculture is another crucial driver for the prominence of driverless tractors. These machines can navigate fields with exceptional accuracy, optimizing the use of resources such as water, fertilizers, and pesticides. The precise application of these resources contributes to increased efficiency, reduced environmental impact, and improved overall crop yield.

The efficiency and time-saving capabilities of driverless tractors are significant contributors to their dominance. With the ability to work continuously and navigate fields efficiently, these autonomous machines enhance operational productivity and allow farmers to cover larger areas in shorter timeframes. This efficiency is particularly valuable during critical farming seasons, such as planting and harvesting, where timing is crucial.

Based on farming environment, outdoor segment dominating in the agriculture robots market. The outdoor segment asserts its dominance in the agriculture robots market, representing a significant advancement in the automation of farming practices within open-field environments. This dominance can be attributed to the versatile and expansive applications of robots in outdoor farming scenarios. Agricultural tasks such as planting, harvesting, and weeding are traditionally labor-intensive and time-consuming, and the integration of robots in outdoor environments addresses these challenges effectively. The outdoor segment’s dominance is particularly evident in large-scale farming operations where vast fields are cultivated. Outdoor agriculture robots, equipped with advanced sensors, GPS technology, and robust navigation systems, demonstrate exceptional adaptability to varying terrains and weather conditions. They can navigate through expansive fields autonomously, optimizing operational efficiency and overcoming the limitations of human labor.

Precision agriculture practices, essential for maximizing crop yield and minimizing resource usage, further contribute to the outdoor segment’s dominance. Robots operating in outdoor environments can precisely apply fertilizers, pesticides, and water, ensuring targeted and efficient use of resources. This capability aligns with the growing emphasis on sustainability and environmental stewardship in modern agriculture. The outdoor segment’s dominance is also propelled by the need to address labor shortages in vast agricultural landscapes. By automating tasks that traditionally require substantial human labor, outdoor agriculture robots provide a solution to the challenges associated with workforce availability, especially during peak farming seasons.

Agriculture Robots Market Dynamics

Driver

Precise application of fertilizers, pesticides, and water can increase efficiency and reduce environmental impact is a key driver for the agriculture robots market.

The precise application of fertilizers, pesticides, and water facilitated by agriculture robots stands out as a pivotal driver for the market, offering multifaceted benefits that enhance efficiency while mitigating environmental impact. In traditional farming, blanket applications of these inputs often lead to overuse, resulting in wastage, environmental pollution, and increased production costs. Agriculture robots equipped with advanced sensing technologies, including GPS, sensors, and data analytics, enable farmers to implement precision agriculture practices.

By precisely targeting and delivering fertilizers, pesticides, and water only where and when needed, agriculture robots optimize resource utilization. This targeted approach ensures that crops receive the necessary nutrients and protection while minimizing excess usage, ultimately contributing to improved crop yield and quality. The reduction in resource wastage aligns with sustainability goals, as it minimizes environmental pollution and conserves vital resources. Moreover, the efficiency gained through the precise application of inputs results in cost savings for farmers. Reduced input costs and increased operational efficiency contribute to the overall economic viability of farming operations. This economic benefit is a crucial aspect, especially for small-scale and large-scale farmers alike, driving the adoption of agriculture robots as a strategic investment for long-term sustainability.

Restraint

Technical complexity and operational challenges can hinder the agriculture robots market during the forecast period.

The agriculture robots market, while offering transformative solutions for the farming industry, faces challenges associated with technical complexity and operational hurdles that could potentially impede its growth during the forecast period. The intricate nature of robotics technology, incorporating elements such as artificial intelligence, sensors, and advanced machinery, introduces technical complexities in the design, manufacturing, and integration of agriculture robots. Developing robots capable of seamlessly navigating diverse terrains, performing intricate tasks, and adapting to various environmental conditions poses substantial engineering challenges.

Operational challenges further compound the hindrances faced by the agriculture robots market. Integrating these sophisticated robotic systems into existing farming practices requires a comprehensive understanding of diverse agricultural environments and practices. Farmers may encounter difficulties in the installation, calibration, and maintenance of these advanced technologies, highlighting the need for specialized technical expertise. The lack of standardized protocols for interoperability across different robotic systems exacerbates operational complexities, as seamless integration becomes a critical factor for widespread adoption.

Moreover, factors such as weather variability, uneven terrains, and unpredictable crop conditions pose operational challenges for agriculture robots. Adapting robotic solutions to dynamic and unpredictable scenarios in real-time necessitates advanced algorithms and sensing capabilities, adding layers of complexity to their operational functionality.

Opportunities

Development of cost-effective solutions is projected to boost the demand for agriculture robots market.

The development of cost-effective solutions emerges as a driving force expected to significantly boost the demand for the agriculture robots market. Historically, one of the challenges hindering the widespread adoption of agriculture robots has been the associated high costs, which may act as a barrier for farmers, particularly those with smaller-scale operations. However, as technological advancements continue and the industry matures, there is a concerted effort to develop more affordable and accessible robotic solutions tailored to meet the diverse needs of farmers.

The projected boost in demand stems from the recognition that cost-effectiveness is a pivotal factor influencing the adoption of agricultural robotic technology. Innovations aimed at reducing the overall cost of robotic systems include advancements in manufacturing processes, materials, and components. These developments contribute to more economical production without compromising the performance and capabilities of the robots.

Furthermore, economies of scale, driven by increasing adoption and production volumes, are expected to play a crucial role in driving down costs. As the demand for agriculture robots rises, manufacturers can benefit from higher production efficiency, reduced per-unit costs, and increased affordability for end-users. This, in turn, enhances the feasibility of adoption across a broader spectrum of farms, regardless of their scale or financial capacity.

Agriculture Robots Market Trends

-

Agriculture robots have been increasingly incorporating artificial intelligence (AI) and machine learning (ML) algorithms. These technologies enhance the robots’ ability to make real-time decisions, analyze data for precision agriculture, and adapt to changing environmental conditions.

-

The use of autonomous vehicles, particularly driverless tractors, has been a notable trend. These vehicles are equipped with advanced navigation systems, allowing them to operate autonomously in the field. This trend aligns with the goal of reducing labor dependency and increasing operational efficiency.

-

Drones equipped with imaging and sensing technologies have gained traction for monitoring crop health and optimizing field management. They provide farmers with aerial views of their fields, allowing for quick and efficient analysis of crop conditions.

-

The concept of swarm robotics, where multiple small robots work collaboratively to perform tasks, has gained attention. This approach allows for more flexibility and efficiency in handling various agricultural activities.

-

Agriculture robots are increasingly contributing to data-driven farming practices. The collection and analysis of data related to soil health, weather conditions, and crop status enable farmers to make informed decisions for better crop management.

-

With the aim of reducing the reliance on herbicides, there has been a trend towards the development of robots designed for targeted weed control. These robots can identify and eliminate weeds with precision, minimizing the impact on the surrounding crops.

Competitive Landscape

The competitive landscape of the agriculture robots market was dynamic, with several prominent companies competing to provide innovative and advanced agriculture robots solutions.

- Deere & Company

- Trimble Inc.

- AGCO Corporation

- AgJunction Inc.

- Topcon Positioning Systems

- CNH Industrial

- Kubota Corporation

- Harvest Automation

- Autonomous Solutions Inc.

- Clearpath Robotics

- Naio Technologies

- Vision Robotics Corporation

- Yamaha Motor Co., Ltd.

- CLAAS KGaA mbH

- 3D Robotics

- GEA Group

- Blue River Technology

- PrecisionHawk

- Kinze Manufacturing

- Autonomous Tractor Corporation

Recent Developments:

-

28, 2024: John Deere (NYSE: DE) introduced the new S7 Series of combines, a family of harvesters designed for efficiency, harvest quality and operator friendliness. Harvest time is no time to let up in the chase for efficiency. The new S7 Series of combines helps farmers and custom operators perform at the maximum to make the most of the season’s efforts.

-

12, 2024: Trimble (NASDAQ: TRMB) announced the integration of the Trimble Applanix POSPac CloudⓇ post-processed kinematic (PPK) GNSS positioning service, featuring CenterPointⓇ RTX, with the drone mapping and data collection capabilities of DroneDeploy’s reality capture platform. With the Trimble cloud positioning service, DroneDeploy customers can expect centimeter-level accuracy and an automated, streamlined workflow when performing reality capture with drones.

Regional Analysis

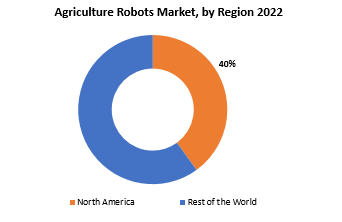

North America accounted for the largest market in the agriculture robots market. North America accounted for 40 % market share of the global market value. North America boasts extensive and large-scale farming operations, particularly in the United States and Canada. The vast expanses of farmland necessitate innovative solutions to address challenges such as labor shortages and operational efficiency, making agriculture robots a strategic choice for modernizing farming practices. Moreover, the region has embraced a culture of technological innovation, positioning itself at the forefront of research and development in the agriculture sector. This commitment to technological advancement has led North American farmers and agribusinesses to readily adopt robotics and automation technologies to optimize various aspects of crop management, from planting and harvesting to monitoring and data analysis.

The supportive regulatory environment in North America has also played a pivotal role in fostering the growth of the agriculture robots market. Clear and accommodating regulations facilitate the deployment of robotic solutions in agriculture, providing a conducive atmosphere for companies to invest in and farmers to adopt cutting-edge technologies. Precision agriculture practices have gained significant traction in North America, aligning seamlessly with the capabilities of agriculture robots. These robots contribute to precision farming by enabling targeted and data-driven decision-making. The region’s emphasis on optimizing the use of resources, minimizing environmental impact, and enhancing overall crop yield aligns well with the capabilities of agriculture robots.

In the agriculture robots market, Europe has emerged as a significant and dynamic region characterized by a blend of traditional farming practices and a proactive adoption of cutting-edge agricultural technologies. The region’s agriculture robots market is driven by several key factors. European farmers, particularly in countries such as Germany, France, and the Netherlands, have embraced precision agriculture, emphasizing data-driven decision-making and resource optimization. This has led to a growing demand for agriculture robots that can enhance efficiency in tasks such as planting, weeding, and harvesting.

The agriculture robots market in the Asia-Pacific region is characterized by a diverse agricultural landscape, ranging from smallholder farms to extensive plantations. Countries such as Japan, China, and Australia have been at the forefront of adopting robotics and automation in agriculture. In Japan, for example, the aging farming population and labor shortages have accelerated the adoption of robotics for tasks like planting and harvesting. China, with its vast agricultural sector, is witnessing increased investments in agricultural technology, including robots, to enhance productivity and address labor challenges. The Asia-Pacific region’s agriculture robots market is also influenced by the adoption of smart farming practices and the integration of technologies like AI and IoT in agricultural operations.

Target Audience for Agriculture Robots Market

- Agricultural Cooperative Societies

- Agribusinesses

- Farm Equipment Manufacturers

- Agricultural Technology Companies

- Research and Development Institutions

- Government Agricultural Departments

- Precision Agriculture Service Providers

- Horticulturists

- Agricultural Consultants

Import & Export Data for Agriculture Robots Market

Exactitude consultancy provides import and export data for the recent years. It also offers insights on production and consumption volume of the product. Understanding the import and export data is pivotal for any player in the agriculture robots market. This knowledge equips businesses with strategic advantages, such as:

- Identifying emerging markets with untapped potential.

- Adapting supply chain strategies to optimize cost-efficiency and market responsiveness.

- Navigating competition by assessing major players’ trade dynamics.

Key insights

-

Trade volume trends: our report dissects import and export data spanning the last five years to reveal crucial trends and growth patterns within the global agriculture robots This data-driven exploration empowers readers with a deep understanding of the market’s trajectory.

-

Market players: gain insights into the leading players driving the agriculture robots From established giants to emerging contenders, our analysis highlights the key contributors to the import and export landscape.

-

Geographical dynamics: delve into the geographical distribution of trade activities. Uncover which regions dominate exports and which ones hold the reins on imports, painting a comprehensive picture of the industry’s global footprint.

-

Product breakdown: by segmenting data based on agriculture robots Product Types –– we provide a granular view of trade preferences and shifts, enabling businesses to align strategies with the evolving technological landscape.

Import and export data is crucial in reports as it offers insights into global market trends, identifies emerging opportunities, and informs supply chain management. By analyzing trade flows, businesses can make informed decisions, manage risks, and tailor strategies to changing demand. This data aids government in policy formulation and trade negotiations, while investors use it to assess market potential. Moreover, import and export data contributes to economic indicators, influences product innovation, and promotes transparency in international trade, making it an essential component for comprehensive and informed analyses.

Segments Covered in the Agriculture Robots Market Report

Agriculture Robots Market by Type

- Driverless Tractors

- Unmanned Aerial Vehicles (UAVs)

- Milking Robots

- Automated Harvesting Robots

- Others

Agriculture Robots Market by Farming Environment

- Outdoor

- Indoor

Agriculture Robots Market by End-use Application

- Field Farming

- Harvest Management

- Livestock Management

- Other Applications

Agriculture Robots Market by Region

- North America

- Europe

- Asia Pacific

- South America

- Middle East and Africa

Key Question Answered

- What is the expected growth rate of the agriculture robots market over the next 7 years?

- Who are the major players in the agriculture robots market and what is their market share?

- What are the end-user industries driving market demand and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-Pacific, the middle east, and Africa?

- How is the economic environment affecting the agriculture robots market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the agriculture robots market?

- What is the current and forecasted size and growth rate of the global agriculture robots market?

- What are the key drivers of growth in the agriculture robots market?

- Who are the major players in the market and what is their market share?

- What are the distribution channels and supply chain dynamics in the agriculture robots market?

- What are the technological advancements and innovations in the agriculture robots market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the agriculture robots market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the agriculture robots market?

- What are the product offerings and specifications of leading players in the market?

Table of Content

- INTRODUCTION

- MARKET DEFINITION

- MARKET SEGMENTATION

- RESEARCH TIMELINES

- ASSUMPTIONS AND LIMITATIONS

- RESEARCH METHODOLOGY

- DATA MINING

- SECONDARY RESEARCH

- PRIMARY RESEARCH

- SUBJECT-MATTER EXPERTS’ ADVICE

- QUALITY CHECKS

- FINAL REVIEW

- DATA TRIANGULATION

- BOTTOM-UP APPROACH

- TOP-DOWN APPROACH

- RESEARCH FLOW

- DATA SOURCES

- DATA MINING

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- AGRICULTURE ROBOTS MARKET OUTLOOK

- MARKET DRIVERS

- MARKET RESTRAINTS

- MARKET OPPORTUNITIES

- IMPACT OF COVID-19 ON AGRICULTURE ROBOTS MARKET

- PORTER’S FIVE FORCES MODEL

- THREAT FROM NEW ENTRANTS

- THREAT FROM SUBSTITUTES

- BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER OF CUSTOMERS

- DEGREE OF COMPETITION

- INDUSTRY VALUE CHAIN ANALYSIS

- AGRICULTURE ROBOTS MARKET OUTLOOK

- GLOBAL AGRICULTURE ROBOTS MARKET BY TYPE, 2020-2030, (USD BILLION) (THOUSAND UNITS)

- DRIVERLESS TRACTORS

- UNMANNED AERIAL VEHICLES (UAVS)

- MILKING ROBOTS

- AUTOMATED HARVESTING ROBOTS

- OTHERS

- GLOBAL AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT, 2020-2030, (USD BILLION) (THOUSAND UNITS)

- OUTDOOR

- INDOOR

- GLOBAL AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION, 2020-2030, (USD BILLION) (THOUSAND UNITS)

- FIELD FARMING

- HARVEST MANAGEMENT

- LIVESTOCK MANAGEMENT

- OTHER APPLICATIONS

- GLOBAL AGRICULTURE ROBOTS MARKET BY REGION, 2020-2030, (USD BILLION) (THOUSAND UNITS)

- NORTH AMERICA

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

- COMPANY PROFILES*

(BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCTS OFFERED, RECENT DEVELOPMENTS)

- DEERE & COMPANY

- TRIMBLE INC.

- AGCO CORPORATION

- AGJUNCTION INC.

- TOPCON POSITIONING SYSTEMS

- CNH INDUSTRIAL

- KUBOTA CORPORATION

- HARVEST AUTOMATION

- AUTONOMOUS SOLUTIONS INC.

- CLEARPATH ROBOTICS

- NAIO TECHNOLOGIES

- VISION ROBOTICS CORPORATION

- YAMAHA MOTOR CO., LTD.

- CLAAS KGAA MBH

- 3D ROBOTICS

- GEA GROUP

- BLUE RIVER TECHNOLOGY

- PRECISIONHAWK

- KINZE MANUFACTURING

- AUTONOMOUS TRACTOR CORPORATION *THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 2 GLOBAL AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 3 GLOBAL AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 4 GLOBAL AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 5 GLOBAL AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 6 GLOBAL AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 7 GLOBAL AGRICULTURE ROBOTS MARKET BY REGION (USD BILLION) 2020-2030

TABLE 8 GLOBAL AGRICULTURE ROBOTS MARKET BY REGION (THOUSAND UNITS) 2020-2030

TABLE 9 NORTH AMERICA AGRICULTURE ROBOTS MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 10 NORTH AMERICA AGRICULTURE ROBOTS MARKET BY COUNTRY (THOUSAND UNITS) 2020-2030

TABLE 11 NORTH AMERICA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 12 NORTH AMERICA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 13 NORTH AMERICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 14 NORTH AMERICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 15 NORTH AMERICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 16 NORTH AMERICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 17 US AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 18 US AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 19 US AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 20 US AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 21 US AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 22 US AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 23 CANADA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 24 CANADA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 25 CANADA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 26 CANADA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 27 CANADA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 28 CANADA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 29 MEXICO AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 30 MEXICO AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 31 MEXICO AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 32 MEXICO AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 33 MEXICO AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 34 MEXICO AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 35 SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 36 SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY COUNTRY (THOUSAND UNITS) 2020-2030

TABLE 37 SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 38 SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 39 SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 40 SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 41 SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 42 SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 43 BRAZIL AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 44 BRAZIL AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 45 BRAZIL AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 46 BRAZIL AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 47 BRAZIL AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 48 BRAZIL AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 49 ARGENTINA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 50 ARGENTINA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 51 ARGENTINA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 52 ARGENTINA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 53 ARGENTINA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 54 ARGENTINA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 55 COLOMBIA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 56 COLOMBIA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 57 COLOMBIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 58 COLOMBIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 59 COLOMBIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 60 COLOMBIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 61 REST OF SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 62 REST OF SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 63 REST OF SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 64 REST OF SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 65 REST OF SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 66 REST OF SOUTH AMERICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 67 ASIA-PACIFIC AGRICULTURE ROBOTS MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 68 ASIA-PACIFIC AGRICULTURE ROBOTS MARKET BY COUNTRY (THOUSAND UNITS) 2020-2030

TABLE 69 ASIA-PACIFIC AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 70 ASIA-PACIFIC AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 71 ASIA-PACIFIC AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 72 ASIA-PACIFIC AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 73 ASIA-PACIFIC AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 74 ASIA-PACIFIC AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 75 INDIA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 76 INDIA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 77 INDIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 78 INDIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 79 INDIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 80 INDIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 81 CHINA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 82 CHINA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 83 CHINA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 84 CHINA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 85 CHINA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 86 CHINA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 87 JAPAN AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 88 JAPAN AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 89 JAPAN AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 90 JAPAN AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 91 JAPAN AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 92 JAPAN AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 93 SOUTH KOREA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 94 SOUTH KOREA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 95 SOUTH KOREA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 96 SOUTH KOREA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 97 SOUTH KOREA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 98 SOUTH KOREA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 99 AUSTRALIA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 100 AUSTRALIA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 101 AUSTRALIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 102 AUSTRALIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 103 AUSTRALIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 104 AUSTRALIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 105 SOUTH-EAST ASIA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 106 SOUTH-EAST ASIA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 107 SOUTH-EAST ASIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 108 SOUTH-EAST ASIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 109 SOUTH-EAST ASIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 110 SOUTH-EAST ASIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 111 REST OF ASIA PACIFIC AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 112 REST OF ASIA PACIFIC AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 113 REST OF ASIA PACIFIC AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 114 REST OF ASIA PACIFIC AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 115 REST OF ASIA PACIFIC AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 116 REST OF ASIA PACIFIC AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 117 EUROPE AGRICULTURE ROBOTS MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 118 EUROPE AGRICULTURE ROBOTS MARKET BY COUNTRY (THOUSAND UNITS) 2020-2030

TABLE 119 EUROPE AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 120 EUROPE AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 121 EUROPE AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 122 EUROPE AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 123 EUROPE AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 124 EUROPE AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 125 GERMANY AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 126 GERMANY AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 127 GERMANY AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 128 GERMANY AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 129 GERMANY AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 130 GERMANY AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 131 UK AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 132 UK AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 133 UK AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 134 UK AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 135 UK AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 136 UK AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 137 FRANCE AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 138 FRANCE AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 139 FRANCE AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 140 FRANCE AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 141 FRANCE AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 142 FRANCE AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 143 ITALY AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 144 ITALY AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 145 ITALY AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 146 ITALY AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 147 ITALY AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 148 ITALY AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 149 SPAIN AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 150 SPAIN AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 151 SPAIN AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 152 SPAIN AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 153 SPAIN AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 154 SPAIN AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 155 RUSSIA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 156 RUSSIA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 157 RUSSIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 158 RUSSIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 159 RUSSIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 160 RUSSIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 161 REST OF EUROPE AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 162 REST OF EUROPE AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 163 REST OF EUROPE AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 164 REST OF EUROPE AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 165 REST OF EUROPE AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 166 REST OF EUROPE AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 167 MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 168 MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY COUNTRY (THOUSAND UNITS) 2020-2030

TABLE 169 MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 170 MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 171 MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 172 MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 173 MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 174 MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 175 UAE AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 176 UAE AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 177 UAE AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 178 UAE AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 179 UAE AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 180 UAE AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 181 SAUDI ARABIA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 182 SAUDI ARABIA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 183 SAUDI ARABIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 184 SAUDI ARABIA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 185 SAUDI ARABIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 186 SAUDI ARABIA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 187 SOUTH AFRICA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 188 SOUTH AFRICA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 189 SOUTH AFRICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 190 SOUTH AFRICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 191 SOUTH AFRICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 192 SOUTH AFRICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

TABLE 193 REST OF MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 194 REST OF MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY TYPE (THOUSAND UNITS) 2020-2030

TABLE 195 REST OF MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

TABLE 196 REST OF MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (THOUSAND UNITS) 2020-2030

TABLE 197 REST OF MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

TABLE 198 REST OF MIDDLE EAST AND AFRICA AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (THOUSAND UNITS) 2020-2030

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2020-2030

FIGURE 9 GLOBAL AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2020-2030

FIGURE 10 GLOBAL AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2020-2030

FIGURE 11 GLOBAL AGRICULTURE ROBOTS MARKET BY REGION (USD BILLION) 2020-2030

FIGURE 12 PORTER’S FIVE FORCES MODEL

FIGURE 13 GLOBAL AGRICULTURE ROBOTS MARKET BY TYPE (USD BILLION) 2022

FIGURE 14 GLOBAL AGRICULTURE ROBOTS MARKET BY FARMING ENVIRONMENT (USD BILLION) 2022

FIGURE 15 GLOBAL AGRICULTURE ROBOTS MARKET BY END-USE APPLICATION (USD BILLION) 2022

FIGURE 16 GLOBAL AGRICULTURE ROBOTS MARKET BY REGION (USD BILLION) 2021

FIGURE 17 MARKET SHARE ANALYSIS

FIGURE 18 DEERE & COMPANY: COMPANY SNAPSHOT

FIGURE 19 TRIMBLE INC.: COMPANY SNAPSHOT

FIGURE 20 AGCO CORPORATION: COMPANY SNAPSHOT

FIGURE 21 AGJUNCTION INC.: COMPANY SNAPSHOT

FIGURE 22 TOPCON POSITIONING SYSTEMS: COMPANY SNAPSHOT

FIGURE 23 CNH INDUSTRIAL: COMPANY SNAPSHOT

FIGURE 24 KUBOTA CORPORATION: COMPANY SNAPSHOT

FIGURE 25 HARVEST AUTOMATION: COMPANY SNAPSHOT

FIGURE 26 AUTONOMOUS SOLUTIONS INC.: COMPANY SNAPSHOT

FIGURE 27 CLEARPATH ROBOTICS: COMPANY SNAPSHOT

FIGURE 28 NAIO TECHNOLOGIES: COMPANY SNAPSHOT

FIGURE 29 VISION ROBOTICS CORPORATION: COMPANY SNAPSHOT

FIGURE 30 YAMAHA MOTOR CO., LTD.: COMPANY SNAPSHOT

FIGURE 31 CLAAS KGAA MBH: COMPANY SNAPSHOT

FIGURE 32 3D ROBOTICS: COMPANY SNAPSHOT

FIGURE 33 GEA GROUP: COMPANY SNAPSHOT

FIGURE 34 BLUE RIVER TECHNOLOGY: COMPANY SNAPSHOT

FIGURE 35 PRECISIONHAWK: COMPANY SNAPSHOT

FIGURE 36 KINZE MANUFACTURING: COMPANY SNAPSHOT

FIGURE 37 AUTONOMOUS TRACTOR CORPORATION: COMPANY SNAPSHOT

FAQ

The global agriculture robots market is anticipated to grow from USD 13.54 Billion in 2023 to USD 62.07 Billion by 2030, at a CAGR of 31.50 % during the forecast period.

North America accounted for the largest market in the agriculture robots market. North America accounted for 40 % market share of the global market value.

Deere & Company, Trimble Inc., AGCO Corporation, AgJunction Inc., Topcon Positioning Systems, CNH Industrial, Kubota Corporation, Harvest Automation, Autonomous Solutions Inc., Clearpath Robotics, Naio Technologies, Vision Robotics Corporation, Yamaha Motor Co., Ltd., CLAAS KGaA mbH, 3D Robotics, GEA Group, Blue River Technology, PrecisionHawk, Kinze Manufacturing, Autonomous Tractor Corporation.

Key trends in the agriculture robots market include the increasing integration of artificial intelligence and machine learning for advanced decision-making, the rise of swarm robotics for collaborative and efficient farming tasks, and the growing adoption of drones equipped with advanced sensors for precise crop monitoring and management.

In-Depth Database

Our Report’s database covers almost all topics of all regions over the Globe.

Recognised Publishing Sources

Tie ups with top publishers around the globe.

Customer Support

Complete pre and post sales

support.

Safe & Secure

Complete secure payment

process.