INTERESTED IN THIS RESEARCH?

Contact our analysts for inquiries, samples, and expert insights.

REPORT OUTLOOK

| Market Size | CAGR | Dominating Region |

|---|---|---|

| USD 32.21 billion by 2030 | 12.5% | Asia Pacific |

| by Type | by Product |

|---|---|

|

|

SCOPE OF THE REPORT

Market Overview

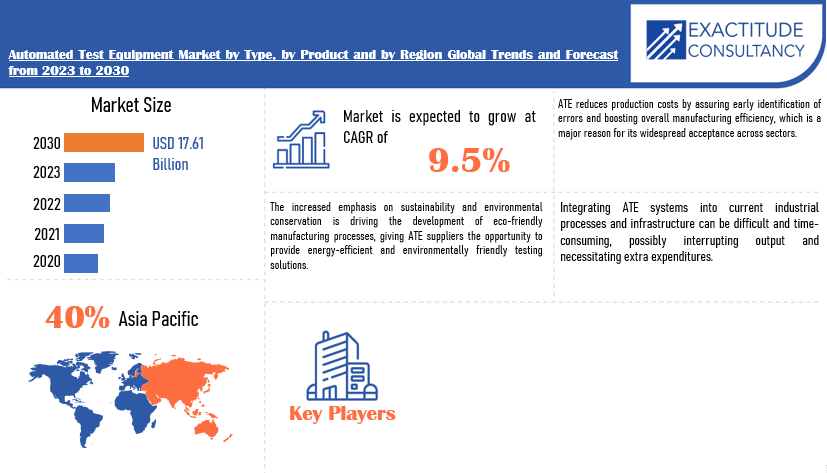

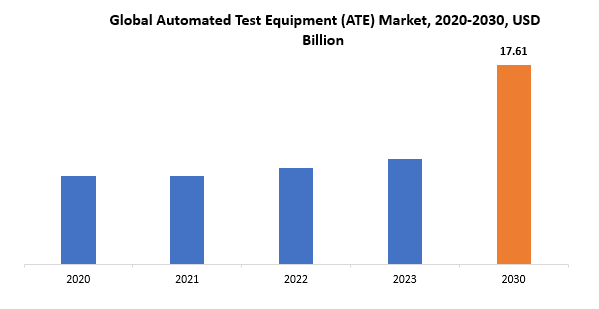

The global automated test equipment market size is projected to grow from USD 9.33 billion in 2023 to USD 17.61 billion by 2030, exhibiting a CAGR of 9.5% during the forecast period.

Automated test equipment (ATE) denotes a sophisticated suite of tools devised for conducting tests on electronic components, systems, or devices with minimal human intervention. ATE finds extensive application across diverse industries like electronics manufacturing, semiconductor production, aerospace, automotive, and telecommunications. These systems are furnished with specialized hardware and software tailored to execute specific tests efficiently and accurately. They encompass a broad spectrum of test procedures, including functional testing, performance testing, reliability testing, and fault detection. ATE is proficient in handling intricate tasks such as applying stimuli, measuring responses, analyzing data, and generating comprehensive reports automatically. Typically, ATE comprises instruments like signal generators, oscilloscopes, mustimeters, and power supplies, integrated with control units and software interfaces. These systems have the capability to test multiple units simultaneously, thereby significantly enhancing throughput and reducing testing duration compared to manual methods. ATE assumes a critical role in assuring the quality, reliability, and functionality of electronic products, aiding manufacturers in meeting rigorous industry standards and customer expectations. By automating testing processes, ATE enhances productivity, curtails labor costs, and mitigates the risk of human error, ultimately fostering heightened efficiency and superior product quality within the manufacturing milieu.

Automated test equipment (ATE) holds considerable significance across diverse industries owing to its capacity to streamline testing procedures, heighten efficiency, and uphold product quality. By automating testing protocols, ATE diminishes reliance on human intervention, thereby reducing the probability of errors and inconsistencies inherent in manual testing methodologies. Consequently, this not only enhances the precision and dependability of test outcomes but also expedites the testing cycle, resulting in quicker time-to-market for products. Furthermore, ATE empowers manufacturers to execute a broad spectrum of tests, encompassing functional testing, performance assessment, reliability analysis, and fault detection, with exactitude and consistency. This comprehensive testing capability aids in pinpointing defects, weaknesses, or irregularities in electronic components or systems, facilitating prompt remedial measures. Consequently, ATE assumes a pivotal role in elevating product quality, mitigating the chances of defects reaching end-users, and fortifying brand integrity.

Moreover, ATE significantly contributes to cost reduction by optimizing resource allocation, minimizing labour expenditures, and maximizing throughput. Its capability to simultaneously test multiple units and automatically generate detailed reports augments productivity and operational efficacy within manufacturing facilities. Furthermore, in industries where stringent adherence to regulatory mandates is imperative, such as aerospace, automotive, and medical devices, ATE ensures compliance with standards and specifications, thereby expediting compliance and certification processes. In summary, Automated Test Equipment is indispensable as it empowers manufacturers to achieve heightened levels of efficiency, precision, and reliability in testing procedures, ultimately resulting in enhanced product quality, reduced costs, and amplified competitiveness in the marketplace.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2030 |

| Base year | 2022 |

| Estimated year | 2023 |

| Forecasted year | 2023-2030 |

| Historical period | 2019-2021 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Product and Region |

|

By Type |

|

|

By Product |

|

|

By Region

|

|

Automated Test Equipment Market Segmentation Analysis

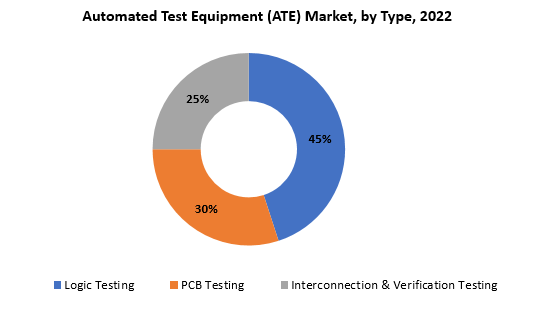

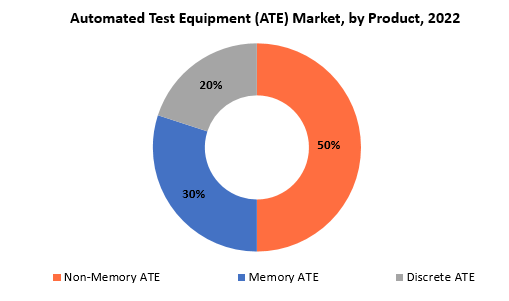

The global automated test equipment market is divided into three segments, by type, product and region. By type, the market is divided into logic testing, PCB testing, interconnection & verification testing. By product, the market is divided into non-memory ATE, memory ATE, discrete and by region.

The automated test equipment market is segmented into logic testing, PCB testing, and interconnection & verification testing. Logic testing involves evaluating the functionality and performance of digital circuits, processors, and integrated circuits (ICs) to ensure they adhere to prescribed logic rules and standards. This type of testing is essential for confirming the accuracy of digital designs and identifying any logical errors or malfunctions during operation. PCB testing concentrates on assessing the quality and reliability of printed circuit boards (PCBs), which serve as the fundamental framework for electronic devices. PCB testing encompasses various examinations such as electrical continuity testing, signal integrity analysis, and insulation resistance testing to detect defects, faults, or deficiencies in PCBs that may compromise their functionality or product quality.

Interconnection & verification testing focuses on validating the integrity and efficacy of connections between different components, modules, or subsystems within electronic systems. This testing ensures the proper functioning of interfaces, communication protocols, and data transfer mechanisms, thereby guaranteeing smooth interaction and interoperability among system elements. Each segment of the ATE market plays a crucial role in maintaining the quality, reliability, and performance of electronic products across diverse industries. Logic testing verifies the correct operation of digital circuits and ICs, PCB testing confirms the integrity of circuit board assemblies, and interconnection & verification testing validates the connectivity and functionality of interconnected components within electronic systems. Together, these testing categories contribute to enhancing the overall efficiency, functionality, and competitiveness of electronic products in the market.

The automated test equipment (ATE) market is segmented by product into non-memory ATE, memory ATE, and discrete ATE. Non-memory ATE includes testing equipment primarily intended for assessing various electronic components and devices excluding memory components. This category encompasses solutions tailored for integrated circuits (ICs), microprocessors, digital signal processors (DSPs), and other non-memory electronic components. Its role is pivotal in verifying the functionality, performance, and reliability of these components to ensure compliance with specified standards and requirements. Memory ATE, on the other hand, comprises testing equipment specifically designed for evaluating memory components like dynamic random-access memory (DRAM), static random-access memory (SRAM), flash memory, and other memory devices. These solutions are engineered to conduct a range of tests aimed at assessing memory capacity, speed, access time, and other critical parameters. Such tests are vital for guaranteeing the quality and reliability of memory components in electronic devices and systems. Lastly, discrete ATE encompasses testing equipment tailored for evaluating discrete electronic components such as transistors, diodes, resistors, capacitors, and other individual electronic parts. These solutions facilitate comprehensive testing of these components to confirm their electrical characteristics, performance specifications, and reliability under various operational conditions. Discrete ATE plays a crucial role in ensuring the quality and functionality of discrete electronic components utilized in electronic circuits and systems. Each product segment within the ATE market serves a specific function in testing different types of electronic components and devices, contributing to the overall quality, reliability, and performance of electronic products across diverse industries. Together, non-memory ATE, memory ATE, and discrete ATE solutions address the varied testing requirements of manufacturers, empowering them to deliver electronic products that meet stringent quality standards and exceed customer expectations.

Automated Test Equipment Market Dynamics

Driver

The growing demand for smartphones, tablets, wearables, and other consumer electronics devices is driving.

The burgeoning consumer electronics market, encompassing smartphones, tablets, wearables, and other gadgets, is fueling a pressing need for more effective and top-tier testing processes, consequently amplifying the demand for Automated Test Equipment (ATE). With consumers worldwide embracing technological advancements and seamlessly integrating electronic devices into their daily routines, manufacturers face mounting pressure to deliver products that not only meet but surpass expectations in terms of functionality, reliability, and performance. This burgeoning need for excellence necessitates stringent testing procedures throughout the manufacturing journey to promptly identify and rectify any defects or shortcomings before products hit the shelves.

ATE assumes a pivotal role in meeting these testing demands by furnishing comprehensive and automated testing solutions adept at efficiently assessing the functionality, performance, and durability of electronic components and systems. Given the escalating complexity of consumer electronics propelled by technological strides like 5G, Internet of Things (IoT), and artificial intelligence (AI), conventional testing methodologies often fall short in ensuring the reliability and quality of these intricate devices. ATE addresses this challenge by offering advanced testing capabilities tailor-made to navigate the intricacies of modern electronic systems, including integrated circuits and semiconductor components. Furthermore, as the consumer electronics sector continues its expansion and diversification, manufacturers find themselves embroiled in heightened competition and confronted with shorter product life cycles, underscoring the urgency for streamlined and expedited testing processes. ATE empowers manufacturers to optimize production efficiency, curtail time-to-market, and trim costs by detecting defects early in the manufacturing cycle, thereby averting the risk of costly recalls or warranty claims in the future. Moreover, ATE facilitates scalability and adaptability, enabling manufacturers to pivot in response to evolving market dynamics and technological advancements without compromising testing precision or throughput. In essence, the surging demand for consumer electronics underscores the indispensable role of ATE in safeguarding the quality, reliability, and performance of electronic devices. By harnessing advanced testing technologies and automation prowess, ATE equips manufacturers to meet consumer expectations for cutting-edge, top-quality products while enhancing operational efficiency and fortifying competitiveness in the dynamic consumer electronics landscape.

Restraint

The initial investment required for implementing ATE solutions can be significant, especially for small and medium-sized enterprises (SMEs), which may act as a barrier to adoption.

The significant initial investment needed to implement Automated Test Equipment (ATE) solutions presents a notable obstacle, particularly for small and medium-sized enterprises (SMEs), potentially hindering their adoption. ATE systems are intricate and specialized, demanding substantial financial resources not only for procuring the equipment but also for upgrading infrastructure, training personnel, and integrating the systems into existing manufacturing processes. For SMEs operating with constrained budgets and resources, this upfront financial commitment may appear daunting and could dissuade them from embracing ATE solutions, despite recognizing their potential advantages. Furthermore, the complexity of ATE systems often entails ongoing expenses beyond the initial investment, including maintenance, calibration, and software updates, further increasing the financial strain. These recurrent costs can burden SMEs financially, making the prospect of ATE adoption seem even more challenging. Additionally, allocating funds to ATE implementation may represent an opportunity cost, diverting resources from other critical areas of business operations and exacerbating financial pressures for SMEs. Moreover, SMEs may encounter difficulties in securing financing or investment capital to support ATE adoption, particularly if they lack a strong track record or sufficient collateral to support funding applications. This limited access to capital can prolong the adoption process or compel SMEs to explore less effective testing solutions to maintain competitiveness. Despite these financial obstacles, the long-term benefits of ATE adoption, such as enhanced product quality, increased productivity, and reduced manufacturing costs, are undeniable. Therefore, it is crucial for SMEs to carefully assess the return on investment and explore strategies to mitigate initial financial barriers, such as leasing arrangements, government incentives, or partnerships with ATE vendors. In conclusion, while the high initial investment required for ATE implementation may present a formidable challenge for SMEs, proactive measures to evaluate and address financial barriers can pave the way for realizing the substantial benefits that ATE offers in terms of bolstering competitiveness and fostering business growth.

Opportunities

The increasing adoption of electronic devices in emerging markets presents significant growth opportunities for ATE vendors.

The rising uptake of electronic devices in emerging markets offers substantial growth prospects for Automated Test Equipment (ATE) vendors, particularly amidst ongoing modernization and industrialization trends. As economies in these regions progress, there’s a growing demand for consumer electronics fueled by factors like increasing incomes, urbanization, and technological advancements. This surge in consumer base underscores the necessity for effective testing processes to ensure the quality and dependability of electronic products. ATE vendors can capitalize on this trend by providing tailored testing solutions that cater to the specific needs of emerging markets. These solutions span various applications, including semiconductor testing, printed circuit board (PCB) testing, and device-level testing. By offering adaptable and comprehensive ATE solutions, vendors can tap into the opportunities presented by the expanding consumer electronics sector in emerging economies. Furthermore, with emerging markets embracing advanced manufacturing practices and initiatives like Industry 4.0, the demand for sophisticated testing technologies is poised to escalate. ATE vendors can leverage this momentum by delivering cutting-edge solutions equipped with features such as automation, data analytics, and remote monitoring capabilities. These innovations not only enhance testing precision and efficiency but also align with broader objectives of enhancing productivity and competitiveness across emerging market industries.

Additionally, ATE vendors can explore collaboration opportunities and strategic partnerships with local manufacturers, governmental bodies, and industry stakeholders in emerging markets. By forging such alliances and leveraging local expertise, vendors can gain valuable insights into market dynamics, regulatory landscapes, and consumer preferences. This, in turn, enables them to tailor their offerings effectively and strengthen their foothold in the rapidly evolving electronics industry within emerging economies. In summary, the increasing adoption of electronic devices in emerging markets presents fertile ground for ATE vendors to expand their operations and capitalize on new growth avenues. Through the provision of innovative solutions, strategic partnerships, and a keen understanding of market trends, vendors can position themselves as key players in driving advancements within the burgeoning electronics sector across emerging economies.

Automated Test Equipment Market Trends

-

The rising adoption of Industry 4.0 principles and the widespread use of Internet of Things (IoT) devices are driving the demand for ATE solutions capable of testing intricate interconnected systems. ATE systems with improved connectivity, automation, and data analytics capabilities are sought after to meet the testing needs of IoT devices and facilitate smart manufacturing practices.

-

The integration of artificial intelligence (AI) and machine learning technologies into ATE systems is enhancing testing efficiency, accuracy, and predictive maintenance capabilities. These technologies empower ATE systems to analyze vast volumes of test data, detect patterns, and optimize testing procedures, resulting in expedited time-to-market and heightened product quality.

-

The proliferation of high-speed communication standards and high-frequency electronic components is fueling demand for ATE solutions capable of testing such components at speed. ATE providers are investing in the development of specialized equipment for high-speed and high-frequency testing to cater to the needs of industries like telecommunications, aerospace, and automotive.

-

Manufacturers are gravitating towards modular and scalable ATE solutions that offer flexibility to adapt to changing testing requirements and scalability to accommodate future expansion. Modular ATE platforms enable seamless integration of additional testing capabilities and facilitate the expansion of testing capacity, offering cost-effective solutions for evolving manufacturing needs.

-

With increasing awareness of environmental sustainability, there is a growing emphasis on developing energy-efficient ATE systems that minimize power consumption and environmental impact. ATE providers are integrating energy-saving features such as power management algorithms, intelligent cooling systems, and eco-friendly materials into their offerings to align with the sustainability objectives of their clientele.

-

The rising adoption of advanced packaging technologies such as 3D ICs, fan-out wafer-level packaging (FOWLP), and system-in-package (SiP) is driving the need for ATE solutions capable of testing these intricate packaging configurations. ATE providers are innovating to develop specialized equipment tailored for testing advanced packaging technologies, addressing the unique challenges posed by these packaging formats.

Competitive Landscape

The competitive landscape of the automated test equipment market was dynamic, with several prominent companies competing to provide innovative and advanced automated test equipment solutions.

- Astronics Corporation

- Chroma ATE Inc.

- Cobham Limited

- Cohu, Inc

- Danaher

- MAC Panel Company

- Marvin Test Solutions, Inc.

- National Instruments Corporation

- Roos Instruments

- SPEA S.p.A.

- STAr Technologies Inc.

- Teradyne Inc.

- TESEC Corporation

- Testamatic Systems Pvt. Ltd.

- Theta Measurement & Control Solutions Pvt Ltd.

- VIAVI Solutions Inc.

- Virginia Panel Corporation

- Xcerra Corporation

Recent Developments:

Feb. 22, 2024 — Danaher Corporation (NYSE: DHR) (Danaher) announced today it has committed to set science-based greenhouse gas (GHG) emission reduction targets in line with the Science Based Targets initiative (SBTi), including a long-term target to reach net-zero value chain emissions by no later than 2050.

Regional Analysis

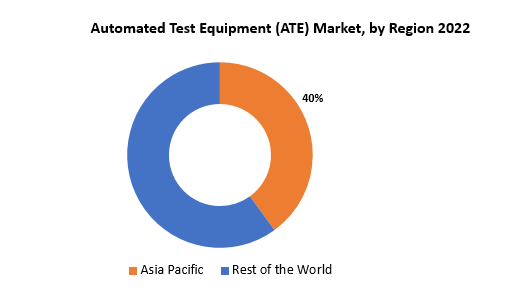

Asia Pacific currently leads the automated test equipment (ATE) market, owing to various factors such as technological advancements, manufacturing prowess, and economic vitality. The region, encompassing countries like China, Japan, South Korea, and Taiwan, boasts extensive electronics manufacturing capabilities, including semiconductor fabrication facilities and assembly plants. This robust infrastructure drives significant demand for ATE solutions to cater to the diverse testing needs of electronic components and devices manufactured in the region. Moreover, Asia Pacific is experiencing rapid technological progression and widespread adoption of advanced technologies like 5G, artificial intelligence, and Internet of Things (IoT). Consequently, there is a heightened requirement for sophisticated ATE systems capable of testing intricate and high-speed electronic components and systems. ATE providers in Asia Pacific are thus focusing on innovation to develop state-of-the-art testing solutions to meet the evolving demands of the electronics industry.

Additionally, Asia Pacific benefits from favorable economic conditions, including lower labor costs and government initiatives aimed at fostering manufacturing and innovation. These factors contribute to making the region an attractive destination for electronics manufacturing companies seeking to optimize production costs while upholding stringent quality standards. Consequently, the demand for ATE solutions in Asia Pacific remains robust, propelling growth in the regional ATE market. Overall, Asia Pacific emerges as the dominant region in the Automated Test Equipment market, propelled by its strong electronics manufacturing ecosystem, technological innovation, and favorable economic environment. With the global demand for electronic components and devices expected to continue rising, Asia Pacific is poised to maintain its leadership position in the ATE market in the foreseeable future.

Target Audience for Automated Test Equipment Market

- Research and Development Teams

- Marketing Agencies

- Consulting Firms

- Consumer electronics companies

- Defense and military contractors

- Research institutions

- Testing laboratories

- Government agencies

- Original equipment manufacturer

- Automotive industry

Segments Covered in the Automated Test Equipment Market Report

Automated Test Equipment Market by Type

- Logic Testing

- PCB Testing

- Interconnection & Verification Testing

Automated Test Equipment Market by Product

- Non-Memory ATE

- Memory ATE

- Discrete ATE

Automated Test Equipment Market by Region

- North America

- Europe

- Asia Pacific

- South America

- Middle East and Africa

Key Question Answered

- What is the expected growth rate of the Automated Test Equipment market over the next 7 years?

- Who are the key market participants in Automated Test Equipment, and what are their market share?

- What are the end-user industries driving market demand and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-Pacific, the Middle East, and Africa?

- How is the economic environment affecting the Automated Test Equipment market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the Automated Test Equipment market?

- What is the current and forecasted size and growth rate of the global Automated Test Equipment market?

- What are the key drivers of growth in the Automated Test Equipment market?

- Who are the major players in the market and what is their market share?

- What are the distribution channels and supply chain dynamics in the Automated Test Equipment market?

- What are the technological advancements and innovations in the Automated Test Equipment market and their impact on product development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the Automated Test Equipment market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the Automated Test Equipment market?

- What are the product offerings and specifications of leading players in the market?

Table of Content

- INTRODUCTION

- MARKET DEFINITION

- MARKET SEGMENTATION

- RESEARCH TIMELINES

- ASSUMPTIONS AND LIMITATIONS

- RESEARCH METHODOLOGY

- DATA MINING

- SECONDARY RESEARCH

- PRIMARY RESEARCH

- SUBJECT-MATTER EXPERTS’ ADVICE

- QUALITY CHECKS

- FINAL REVIEW

- DATA TRIANGULATION

- BOTTOM-UP APPROACH

- TOP-DOWN APPROACH

- RESEARCH FLOW

- DATA SOURCES

- DATA MINING

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- AUTOMATED TEST EQUIPMENT MARKET OUTLOOK

- MARKET DRIVERS

- MARKET RESTRAINTS

- MARKET OPPORTUNITIES

- IMPACT OF COVID-19 ON AUTOMATED TEST EQUIPMENT MARKET

- PORTER’S FIVE FORCES MODEL

- THREAT FROM NEW ENTRANTS

- THREAT FROM SUBSTITUTES

- BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER OF CUSTOMERS

- DEGREE OF COMPETITION

- INDUSTRY VALUE CHAIN ANALYSIS

- AUTOMATED TEST EQUIPMENT MARKET OUTLOOK

- GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY TYPE, 2020-2030, (USD BILLION)

- LOGIC TESTING

- PCB TESTING

- INTERCONNECTION & VERIFICATION TESTING

- GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT, 2020-2030, (USD BILLION)

- NON-MEMORY ATE

- MEMORY ATE

- DISCRETE ATE

- GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY REGION, 2020-2030, (USD BILLION)

- NORTH AMERICA

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

- COMPANY PROFILES*

(BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCTS OFFERED, RECENT DEVELOPMENTS)

- ADVANTEST CORPORATION

- AEMULUS CORPORATION

- ASTRONICS CORPORATION

- CHROMA ATE INC.

- COBHAM LIMITED

- COHU, INC

- DANAHER

- MAC PANEL COMPANY

- MARVIN TEST SOLUTIONS, INC.

- NATIONAL INSTRUMENTS CORPORATION

- ROOS INSTRUMENTS

- SPEA S.P.A.

- STAR TECHNOLOGIES INC.

- TERADYNE INC.

- TESEC CORPORATION

- TESTAMATIC SYSTEMS PVT. LTD.

- THETA MEASUREMENT & CONTROL SOLUTIONS PVT LTD.

- VIAVI SOLUTIONS INC.

- VIRGINIA PANEL CORPORATION

- XCERRA CORPORATION*THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 2 GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 3 GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY REGION (USD BILLION) 2020-2030

TABLE 4 NORTH AMERICA AUTOMATED TEST EQUIPMENT MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 5 NORTH AMERICA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 6 NORTH AMERICA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 7 US AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 8 US AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 9 CANADA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 10 CANADA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 11 MEXICO AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 12 MEXICO AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 13 SOUTH AMERICA AUTOMATED TEST EQUIPMENT MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 14 SOUTH AMERICA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 15 SOUTH AMERICA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 16 BRAZIL AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 17 BRAZIL AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 18 ARGENTINA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 19 ARGENTINA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 20 COLOMBIA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 21 COLOMBIA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 22 REST OF SOUTH AMERICA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 23 REST OF SOUTH AMERICA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 24 ASIA-PACIFIC AUTOMATED TEST EQUIPMENT MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 25 ASIA-PACIFIC AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 26 ASIA-PACIFIC AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 27 INDIA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 28 INDIA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 29 CHINA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 30 CHINA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 31 JAPAN AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 32 JAPAN AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 33 SOUTH KOREA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 34 SOUTH KOREA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 35 AUSTRALIA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 36 AUSTRALIA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 37 SOUTH-EAST ASIA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 38 SOUTH-EAST ASIA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 39 REST OF ASIA PACIFIC AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 40 REST OF ASIA PACIFIC AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 41 EUROPE AUTOMATED TEST EQUIPMENT MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 42 EUROPE AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 43 EUROPE AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 44 GERMANY AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 45 GERMANY AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 46 UK AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 47 UK AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 48 FRANCE AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 49 FRANCE AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 50 ITALY AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 51 ITALY AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 52 SPAIN AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 53 SPAIN AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 54 RUSSIA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 55 RUSSIA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 56 REST OF EUROPE AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 57 REST OF EUROPE AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 58 MIDDLE EAST AND AFRICA AUTOMATED TEST EQUIPMENT MARKET BY COUNTRY (USD BILLION) 2020-2030

TABLE 59 MIDDLE EAST AND AFRICA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 60 MIDDLE EAST AND AFRICA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 61 UAE AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 62 UAE AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 63 SAUDI ARABIA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 64 SAUDI ARABIA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 65 SOUTH AFRICA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 66 SOUTH AFRICA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

TABLE 67 REST OF MIDDLE EAST AND AFRICA AUTOMATED TEST EQUIPMENT MARKET BY TYPE (USD BILLION) 2020-2030

TABLE 68 REST OF MIDDLE EAST AND AFRICA AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT (USD BILLION) 2020-2030

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY TYPE, USD BILLION, 2022-2030

FIGURE 9 GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT, USD BILLION, 2022-2030

FIGURE 10 GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY REGION, USD BILLION, 2022-2030

FIGURE 11 PORTER’S FIVE FORCES MODEL

FIGURE 12 GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY TYPE, USD BILLION,2022

FIGURE 13 GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY PRODUCT, USD BILLION,2022

FIGURE 14 GLOBAL AUTOMATED TEST EQUIPMENT MARKET BY REGION, USD BILLION,2022

FIGURE 15 MARKET SHARE ANALYSIS

FIGURE 16 ADVANTEST CORPORATION: COMPANY SNAPSHOT

FIGURE 17 AEMULUS CORPORATION: COMPANY SNAPSHOT

FIGURE 18 ASTRONICS CORPORATION: COMPANY SNAPSHOT

FIGURE 19 CHROMA ATE INC.: COMPANY SNAPSHOT

FIGURE 20 COBHAM LIMITED: COMPANY SNAPSHOT

FIGURE 21 COHU, INC: COMPANY SNAPSHOT

FIGURE 22 DANAHER: COMPANY SNAPSHOT

FIGURE 23 MAC PANEL COMPANY: COMPANY SNAPSHOT

FIGURE 24 MARVIN TEST SOLUTIONS, INC.: COMPANY SNAPSHOT

FIGURE 25 NATIONAL INSTRUMENTS CORPORATION: COMPANY SNAPSHOT

FIGURE 26 ROOS INSTRUMENTS: COMPANY SNAPSHOT

FIGURE 27 SPEA S.P.A.: COMPANY SNAPSHOT

FIGURE 28 STAR TECHNOLOGIES INC.: COMPANY SNAPSHOT

FIGURE 29 TERADYNE INC.: COMPANY SNAPSHOT

FIGURE 30 TESEC CORPORATION: COMPANY SNAPSHOT

FIGURE 31 TESTAMATIC SYSTEMS PVT. LTD.: COMPANY SNAPSHOT

FIGURE 32 THETA MEASUREMENT & CONTROL SOLUTIONS PVT LTD.: COMPANY SNAPSHOT

FIGURE 33 VIAVI SOLUTIONS INC.: COMPANY SNAPSHOT

FIGURE 34 VIRGINIA PANEL CORPORATION: COMPANY SNAPSHOT

FIGURE 35 XCERRA CORPORATION: COMPANY SNAPSHOT

FAQ

The global automated test equipment market size is projected to grow from USD 64.79 billion in 2023 to USD 32.21 billion by 2030, exhibiting a CAGR of 12.5% during the forecast period.

Asia Pacific accounted for the largest market in the automated test equipment market.

Astronics Corporation, Chroma ATE Inc., Cobham Limited, Cohu, Inc, Danaher,MAC Panel Company, Marvin Test Solutions, Inc., National Instruments Corporation, Roos Instruments, SPEA S.p.A.,STAr Technologies Inc., Teradyne Inc.,TESEC Corporation.

With the escalating threat of cyberattacks targeting connected devices and systems, there is heightened attention to cybersecurity in ATE solutions. Manufacturers are incorporating robust security features such as encryption, authentication, and secure communication protocols into ATE systems to safeguard sensitive test data and ensure the integrity of testing processes.

In-Depth Database

Our Report’s database covers almost all topics of all regions over the Globe.

Recognised Publishing Sources

Tie ups with top publishers around the globe.

Customer Support

Complete pre and post sales

support.

Safe & Secure

Complete secure payment

process.