Base Year Value ()

x.x %

x.x %

CAGR ()

x.x %

x.x %

Forecast Year Value ()

x.x %

x.x %

Historical Data Period

Largest Region

Forecast Period

Marché des mèches en fibre de verre par type de produit (mèches à une extrémité, mèches à plusieurs extrémités, mèches hachées), par type de verre (verre E, verre ECR, verre H, verre AR, verre S), par utilisateur final (transport, construction et infrastructure, électricité et électronique, tuyaux et réservoirs, marine, aérospatiale et défense, énergie éolienne) et région, tendances mondiales et prévisions de 2022 à 2029

Instant access to hundreds of data points and trends

- Market estimates from 2014-2029

- Competitive analysis, industry segmentation, financial benchmarks

- Incorporates SWOT, Porter's Five Forces and risk management frameworks

- PDF report or online database with Word, Excel and PowerPoint export options

- 100% money back guarantee

Aperçu du marché des mèches en fibre de verre

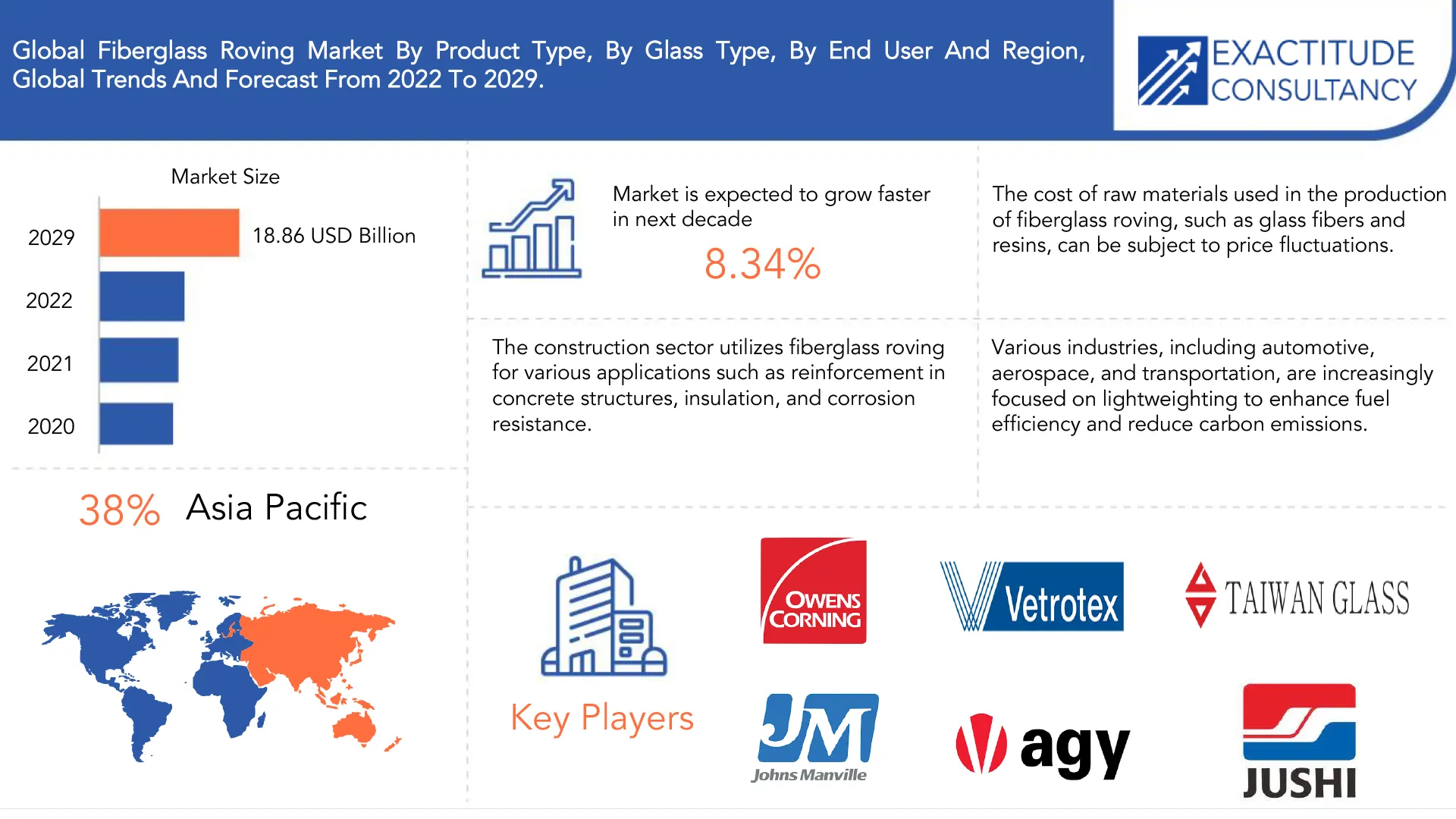

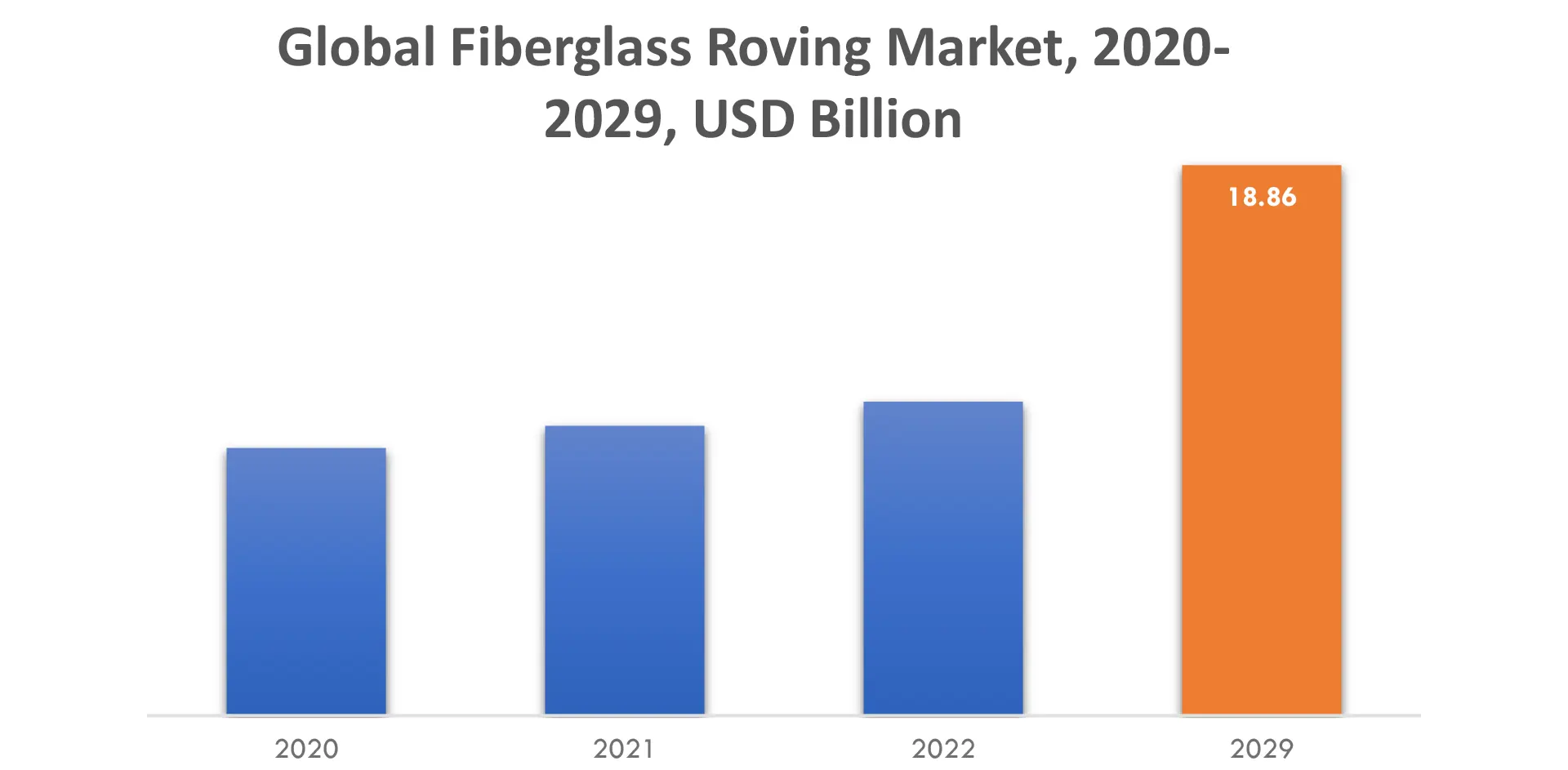

Le marché des mèches en fibre de verre devrait croître à un TCAC de 8,34 % entre 2022 et 2029. Il devrait atteindre plus de 18,86 milliards USD d'ici 2029, contre 9,17 milliards USD en 2020.

La fibre de verre est un matériau de renforcement utilisé dans la production de composites . Elle est fabriquée en tirant du verre fondu à travers de fines bagues, ce qui donne des filaments de verre continus . Ces filaments sont ensuite rassemblés pour former un brin appelé mèche. La fibre de verre est connue pour sa résistance élevée à la traction, sa résistance thermique, sa résistance à la corrosion et ses propriétés d'isolation électrique. Elle est largement utilisée dans diverses industries, telles que l'automobile, l'aérospatiale, la construction, l'énergie éolienne et la marine, pour renforcer et améliorer les propriétés des produits composites, notamment les panneaux de carrosserie, les coques de bateau, les pales d'éoliennes, les tuyaux et les réservoirs.

[caption id="attachment_26418" align="aligncenter" width="1920"]

La demande croissante de matériaux résistants à la corrosion est un facteur important pour le marché des mèches en fibre de verre. Les mèches en fibre de verre présentent une excellente résistance à la corrosion, ce qui les rend très recherchées par les industries telles que le pétrole et le gaz, le traitement chimique et la marine . Ces secteurs nécessitent des matériaux capables de résister aux environnements difficiles et à l'exposition à des substances corrosives. Les propriétés de résistance à la corrosion des mèches en fibre de verre permettent leur utilisation dans la production de composants, de structures et d'équipements résistants à la corrosion. Les industries se concentrant sur l'amélioration de la durabilité et de la longévité de leurs produits, la demande de mèches en fibre de verre en tant que matériau de renforcement résistant à la corrosion continue d'augmenter. Ce facteur ouvre des opportunités pour le marché des mèches en fibre de verre pour répondre aux besoins croissants des industries sujettes à la corrosion.

The volatility in raw material prices poses a significant restraint on the fiberglass roving market. The cost of raw materials used in the production of fiberglass roving, such as glass fibers and resins, can fluctuate unpredictably. These price fluctuations can impact the profitability and cost structure of fiberglass roving manufacturers, making it challenging to maintain stable pricing and margins. Sudden increases in raw material prices can lead to higher production costs, which may be difficult to pass on to customers. Moreover, the uncertainty in raw material costs can affect long-term planning, investments, and decision-making in the fiberglass roving industry. Managing and mitigating the impact of raw material price volatility becomes crucial for sustained growth and profitability in the market.

Lightweighting initiatives present a significant opportunity for the fiberglass roving market. Various industries, including automotive, aerospace, and transportation, are increasingly focused on reducing weight to improve fuel efficiency and reduce carbon emissions. Fiberglass roving, known for its high strength-to-weight ratio, can be a preferred reinforcement material in lightweighting applications. By incorporating fiberglass roving into composite structures, manufacturers can achieve substantial weight reduction while maintaining structural integrity and performance. This opportunity allows the fiberglass roving market to cater to the growing demand for lightweight materials in industries that prioritize sustainability and efficiency. By providing a solution for lightweighting initiatives, fiberglass roving can contribute to the development of more fuel-efficient vehicles, aerospace components, and transportation systems.

The COVID-19 pandemic had a significant negative impact on the fiberglass roving market. The outbreak led to disruptions in global supply chains, manufacturing operations, and reduced economic activity. The construction industry, a major consumer of fiberglass roving, experienced slowdowns and project delays due to lockdowns and social distancing measures. The automotive and aerospace sectors, which also utilize fiberglass roving, faced a decline in demand as consumer spending and travel were severely affected. Additionally, the closure of manufacturing facilities and restrictions on international trade disrupted the supply of raw materials, impacting production capabilities. Uncertainty and reduced investments during the pandemic further affected market growth. While the fiberglass roving market is expected to recover as economies stabilize, the short-term negative impact of COVID-19 on the industry had significant.

| ATTRIBUTE | DETAILS |

| Study period | 2020-2029 |

| Base year | 2021 |

| Estimated year | 2022 |

| Forecasted year | 2022-2029 |

| Historical period | 2018-2020 |

| Unit | Value (USD Billion), (Kilotons) |

| Segmentation | By Product Type, By Glass Type, By End User, By Region. |

| By Product Type |

|

| By Glass Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

• What is the worth of fiberglass roving market?

The fiberglass roving market is expected to grow at 8.34 % CAGR from 2022 to 2029. It is expected to reach above USD 18.86 Billion by 2029 from USD 9.17 Billion in 2020.

• What is the size of the Asia Pacific fiberglass roving industry?

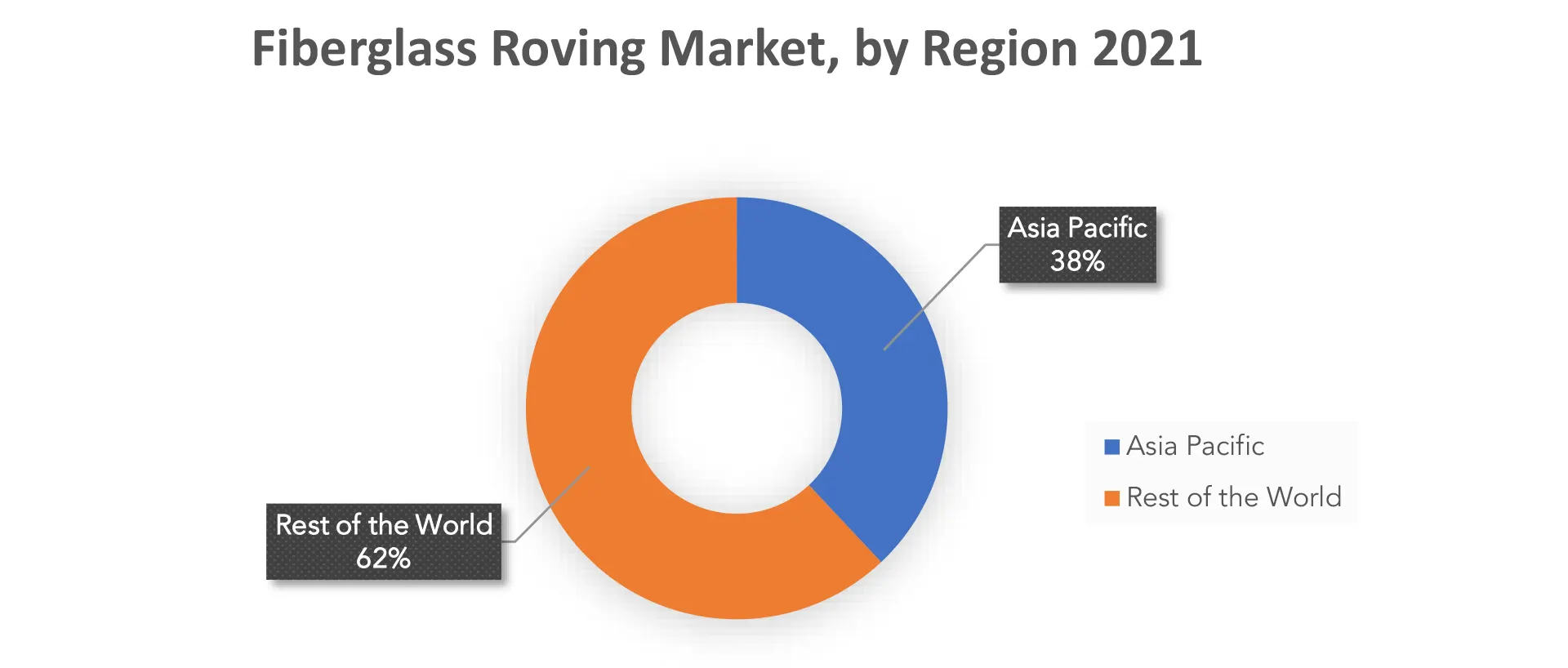

Asia Pacific held more than 38% of the fiberglass roving market revenue share in 2021 and will witness expansion in the forecast period.

• What are some of the market's driving forces?

Fiberglass roving is used as a reinforcement material in the production of lightweight composites. With increasing emphasis on fuel efficiency and reducing vehicle weight in industries like automotive and aerospace, there is a rising demand for fiberglass roving to manufacture lightweight components.

• Which are the top companies to hold the market share in fiberglass roving market?

The fiberglass roving market key players include Taiwan Glass Industry Corp., Owens Corning, China Beihai Fiberglass Co. Ltd., Saint-Gobain S.A., AGY Holdings Corp, Binani Industries Ltd, Nippon Electrical Glass Co. Ltd, Taishan Fiberglass Inc., Jushi India Fiberglass (P) Ltd, Johns Manville

• What is the leading application of fiberglass roving market?

The transportation industry is major sector where the application of fiberglass roving has seen more.

• Which is the largest regional market for fiberglass roving market?

The markets largest share is in the Asia Pacific region.

Fiberglass Roving Market Segment Analysis

The single-end roving product type is the dominant segment in the fiberglass roving market. Single-end roving consists of individual continuous filaments of glass that are gathered together into a single strand. This product type offers flexibility and ease of handling during the manufacturing process. It is widely used in various applications across industries such as automotive, construction, aerospace, and wind energy. The dominance of single-end roving in the market can be attributed to its versatility, cost-effectiveness, and suitability for a wide range of composite manufacturing processes.

[caption id="attachment_26419" align="aligncenter" width="1920"]

The E-glass fiber segment holds a significant share in the global fiberglass roving market. E-glass fiber is the most commonly used type of glass fiber for reinforcement purposes. It offers excellent properties such as high strength, good electrical insulation, and corrosion resistance, making it suitable for various applications. E-glass fiber is widely utilized in industries such as automotive, construction, aerospace, and electrical and electronics. Its dominance in the fiberglass roving market is attributed to its versatile properties, availability, and established manufacturing processes.

The transportation end-use industry segment holds the largest share in the fiberglass roving market. This sector encompasses applications in automotive, aerospace, and other transportation-related industries. The demand for fiberglass roving in transportation is driven by the need for lightweight materials that provide strength, durability, and fuel efficiency. Fiberglass roving finds extensive usage in automotive body panels, interior components, aircraft parts, and other transportation applications. The transportation industry's reliance on fiberglass roving makes it a key contributor to the overall market size and growth.

Who Should Buy? Or Key Stakeholders

- Chemicals Companies

- Transportation Companies

- Raw Material Manufacturer

- Market Research

- Research and Development Institutes

- Consulting Firms

- Venture capitalists

- Investors

- Supplier and Distributor

- Others

Fiberglass Roving Market Regional Analysis

The Fiberglass Roving market by region includes North America, Asia-Pacific (APAC), Europe, South America, and Middle East & Africa (MEA).

- North America: includes the US, Canada, Mexico

- Asia Pacific: includes China, Japan, South Korea, India, Australia, ASEAN and Rest of APAC

- Europe: includes UK, Germany, France, Italy, Spain, Russia, and Rest of Europe

- South America: includes Brazil, Argentina and Rest of South America

- Middle East & Africa: includes Turkey, UAE, Saudi Arabia, South Africa, and Rest of MEA

Asia Pacific is a key consumer of fiberglass roving, representing a significant market share. The region's strong demand for fiberglass roving is driven by various factors. The rapid industrialization and infrastructure development in countries like China, India, and Southeast Asian nations contribute to the increased consumption of fiberglass roving in construction, automotive, and other industries. Additionally, the growing manufacturing sector, rising population, and urbanization drive the demand for fiberglass roving in the Asia Pacific region. The presence of major end-use industries and the continuous growth of emerging economies in the region further solidify its position as a key consumer of fiberglass roving.

North America is a prominent market for fiberglass roving. The region encompasses the US, Canada, and Mexico, all of which contribute to the demand for fiberglass roving. North America's strong construction industry, advanced automotive sector, and aerospace industry create substantial opportunities for fiberglass roving usage. Additionally, the region's emphasis on renewable energy, including wind power, drives the need for fiberglass roving in wind turbine manufacturing. North America's commitment to technological advancements, innovation, and sustainability further supports the growth of the fiberglass roving market in the region.

Key Market Segments: Fiberglass Roving Market

Fiberglass Roving Market by Product Type, 2020-2029, (USD Billion), (Kilotons).- Single-End Roving

- Multi-End Roving

- Chopped Roving

- E-Glass

- ECR-Glass

- H-Glass

- AR-Glass

- S-Glass

- Transportation

- Construction & Infrastructure

- Electrical & Electronics

- Pipes & Tanks

- Marine

- Aerospace & Defense

- Wind Energy

- North America

- Asia Pacific

- Europe

- South America

- Middle East and Africa

Exactitude Consultancy Services Key Objectives:

- Increasing sales and market share

- Developing new technology

- Improving profitability

- Entering new markets

- Enhancing brand reputation

Key Question Answered

- What is the expected growth rate of the fiberglass roving market over the next 7 years?

- Who are the major players in the fiberglass roving market and what is their market share?

- What are the end-user industries driving demand for market and what is their outlook?

- What are the opportunities for growth in emerging markets such as Asia-pacific, middle east, and Africa?

- How is the economic environment affecting the fiberglass roving market, including factors such as interest rates, inflation, and exchange rates?

- What is the expected impact of government policies and regulations on the fiberglass roving market?

- What is the current and forecasted size and growth rate of the global fiberglass roving market?

- What are the key drivers of growth in the fiberglass roving market?

- What are the distribution channels and supply chain dynamics in the fiberglass roving market?

- What are the technological advancements and innovations in the fiberglass roving market and their impact on material development and growth?

- What are the regulatory considerations and their impact on the market?

- What are the challenges faced by players in the fiberglass roving market and how are they addressing these challenges?

- What are the opportunities for growth and expansion in the fiberglass roving market?

- What are the products offerings and specifications of leading players in the market?

- What is the pricing trend of fiberglass roving in the market and what is the impact of raw material prices on the price trend?

- INTRODUCTION

- MARKET DEFINITION

- MARKET SEGMENTATION

- RESEARCH TIMELINES

- ASSUMPTIONS AND LIMITATIONS

- RESEARCH METHODOLOGY

- DATA MINING

- SECONDARY RESEARCH

- PRIMARY RESEARCH

- SUBJECT-MATTER EXPERTS’ ADVICE

- QUALITY CHECKS

- FINAL REVIEW

- DATA TRIANGULATION

- BOTTOM-UP APPROACH

- TOP-DOWN APPROACH

- RESEARCH FLOW

- DATA SOURCES

- DATA MINING

- EXECUTIVE SUMMARY

- MARKET OVERVIEW

- GLOBAL FIBERGLASS ROVING MARKET OUTLOOK

- MARKET DRIVERS

- MARKET RESTRAINTS

- MARKET OPPORTUNITIES

- IMPACT OF COVID-19 ON FIBERGLASS ROVING MARKET

- PORTER’S FIVE FORCES MODEL

- THREAT FROM NEW ENTRANTS

- THREAT FROM SUBSTITUTES

- BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER OF CUSTOMERS

- DEGREE OF COMPETITION

- INDUSTRY VALUE CHAIN ANALYSIS

- GLOBAL FIBERGLASS ROVING MARKET OUTLOOK

- GLOBAL FIBERGLASS ROVING MARKET BY PRODUCT TYPE, 2020-2029, (USD BILLION), (KILOTONS)

- SINGLE-END ROVING

- MULTI-END ROVING

- CHOPPED ROVING

- GLOBAL FIBERGLASS ROVING MARKET BY GLASS TYPE, 2020-2029, (USD BILLION), (KILOTONS)

- E-GLASS

- ECR-GLASS

- H-GLASS

- AR-GLASS

- S-GLASS

- GLOBAL FIBERGLASS ROVING MARKET BY END USER, 2020-2029, (USD BILLION), (KILOTONS)

- TRANSPORTATION

- CONSTRUCTION & INFRASTRUCTURE

- ELECTRICAL & ELECTRONICS

- PIPES & TANKS

- MARINE

- AEROSPACE & DEFENSE

- WIND ENERGY

- GLOBAL FIBERGLASS ROVING MARKET BY REGION, 2020-2029, (USD BILLION), (KILOTONS)

- NORTH AMERICA

- US

- CANADA

- MEXICO

- SOUTH AMERICA

- BRAZIL

- ARGENTINA

- COLOMBIA

- REST OF SOUTH AMERICA

- EUROPE

- GERMANY

- UK

- FRANCE

- ITALY

- SPAIN

- RUSSIA

- REST OF EUROPE

- ASIA PACIFIC

- INDIA

- CHINA

- JAPAN

- SOUTH KOREA

- AUSTRALIA

- SOUTH-EAST ASIA

- REST OF ASIA PACIFIC

- MIDDLE EAST AND AFRICA

- UAE

- SAUDI ARABIA

- SOUTH AFRICA

- REST OF MIDDLE EAST AND AFRICA

- NORTH AMERICA

COMPANY PROFILES* (BUSINESS OVERVIEW, COMPANY SNAPSHOT, PRODUCT OFFERED, RECENT DEVELOPMENTS)

- TAIWAN GLASS INDUSTRY CORP.

- OWENS CORNING

- CHINA BEIHAI FIBERGLASS CO. LTD.

- SAINT-GOBAIN S.A.

- AGY HOLDINGS CORP

- BINANI INDUSTRIES LTD

- NIPPON ELECTRICAL GLASS CO. LTD

- TAISHAN FIBERGLASS INC.

- JUSHI INDIA FIBERGLASS (P) LTD.

- JOHNS MANVILLE *THE COMPANY LIST IS INDICATIVE

LIST OF TABLES

TABLE 1 GLOBAL FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 2 GLOBAL FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 3 GLOBAL FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 4 GLOBAL FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 5 GLOBAL FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 6 GLOBAL FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 7 GLOBAL FIBERGLASS ROVING MARKET BY REGION (USD BILLION) 2020-2029

TABLE 8 GLOBAL FIBERGLASS ROVING MARKET BY REGION (KILOTONS) 2020-2029

TABLE 9 NORTH AMERICA FIBERGLASS ROVING MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 10 NORTH AMERICA FIBERGLASS ROVING MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 11 NORTH AMERICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 12 NORTH AMERICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 13 NORTH AMERICA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 14 NORTH AMERICA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 15 NORTH AMERICA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 16 NORTH AMERICA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 17 US FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 18 US FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 19 US FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 20 US FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 21 US FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 22 US FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 23 CANADA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 24 CANADA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 25 CANADA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 26 CANADA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 27 CANADA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 28 CANADA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 29 MEXICO FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 30 MEXICO FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 31 MEXICO FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 32 MEXICO FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 33 MEXICO FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 34 MEXICO FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 35 SOUTH AMERICA FIBERGLASS ROVING MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 36 SOUTH AMERICA FIBERGLASS ROVING MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 37 SOUTH AMERICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 38 SOUTH AMERICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 39 SOUTH AMERICA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 40 SOUTH AMERICA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 41 SOUTH AMERICA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 42 SOUTH AMERICA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 43 BRAZIL FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 44 BRAZIL FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 45 BRAZIL FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 46 BRAZIL FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 47 BRAZIL FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 48 BRAZIL FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 49 ARGENTINA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 50 ARGENTINA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 51 ARGENTINA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 52 ARGENTINA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 53 ARGENTINA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 54 ARGENTINA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 55 COLOMBIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 56 COLOMBIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 57 COLOMBIA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 58 COLOMBIA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 59 COLOMBIA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 60 COLOMBIA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 61 REST OF SOUTH AMERICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 62 REST OF SOUTH AMERICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 63 REST OF SOUTH AMERICA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 64 REST OF SOUTH AMERICA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 65 REST OF SOUTH AMERICA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 66 REST OF SOUTH AMERICA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 67 ASIA-PACIFIC FIBERGLASS ROVING MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 68 ASIA-PACIFIC FIBERGLASS ROVING MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 69 ASIA-PACIFIC FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 70 ASIA-PACIFIC FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 71 ASIA-PACIFIC FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 72 ASIA-PACIFIC FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 73 ASIA-PACIFIC FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 74 ASIA-PACIFIC FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 75 INDIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 76 INDIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 77 INDIA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 78 INDIA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 79 INDIA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 80 INDIA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 81 CHINA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 82 CHINA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 83 CHINA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 84 CHINA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 85 CHINA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 86 CHINA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 87 JAPAN FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 88 JAPAN FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 89 JAPAN FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 90 JAPAN FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 91 JAPAN FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 92 JAPAN FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 93 SOUTH KOREA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 94 SOUTH KOREA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 95 SOUTH KOREA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 96 SOUTH KOREA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 97 SOUTH KOREA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 98 SOUTH KOREA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 99 AUSTRALIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 100 AUSTRALIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 101 AUSTRALIA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 102 AUSTRALIA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 103 AUSTRALIA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 104 AUSTRALIA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 105 SOUTH-EAST ASIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 106 SOUTH-EAST ASIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 107 SOUTH-EAST ASIA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 108 SOUTH-EAST ASIA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 109 SOUTH-EAST ASIA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 110 SOUTH-EAST ASIA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 111 REST OF ASIA PACIFIC FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 112 REST OF ASIA PACIFIC FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 113 REST OF ASIA PACIFIC FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 114 REST OF ASIA PACIFIC FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 115 REST OF ASIA PACIFIC FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 116 REST OF ASIA PACIFIC FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 117 EUROPE FIBERGLASS ROVING MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 118 EUROPE FIBERGLASS ROVING MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 119 EUROPE FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 120 EUROPE FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 121 EUROPE FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 122 EUROPE FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 123 EUROPE FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 124 EUROPE FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 125 GERMANY FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 126 GERMANY FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 127 GERMANY FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 128 GERMANY FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 129 GERMANY FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 130 GERMANY FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 131 UK FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 132 UK FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 133 UK FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 134 UK FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 135 UK FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 136 UK FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 137 FRANCE FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 138 FRANCE FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 139 FRANCE FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 140 FRANCE FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 141 FRANCE FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 142 FRANCE FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 143 ITALY FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 144 ITALY FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 145 ITALY FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 146 ITALY FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 147 ITALY FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 148 ITALY FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 149 SPAIN FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 150 SPAIN FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 151 SPAIN FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 152 SPAIN FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 153 SPAIN FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 154 SPAIN FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 155 RUSSIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 156 RUSSIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 157 RUSSIA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 158 RUSSIA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 159 RUSSIA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 160 RUSSIA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 161 REST OF EUROPE FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 162 REST OF EUROPE FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 163 REST OF EUROPE FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 164 REST OF EUROPE FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 165 REST OF EUROPE FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 166 REST OF EUROPE FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 167 MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY COUNTRY (USD BILLION) 2020-2029

TABLE 168 MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY COUNTRY (KILOTONS) 2020-2029

TABLE 169 MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 170 MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 171 MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 172 MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 173 MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 174 MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 175 UAE FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 176 UAE FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 177 UAE FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 178 UAE FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 179 UAE FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 180 UAE FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 181 SAUDI ARABIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 182 SAUDI ARABIA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 183 SAUDI ARABIA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 184 SAUDI ARABIA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 185 SAUDI ARABIA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 186 SAUDI ARABIA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 187 SOUTH AFRICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 188 SOUTH AFRICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 189 SOUTH AFRICA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 190 SOUTH AFRICA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 191 SOUTH AFRICA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 192 SOUTH AFRICA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

TABLE 193 REST OF MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (USD BILLION) 2020-2029

TABLE 194 REST OF MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY PRODUCT TYPE (KILOTONS) 2020-2029

TABLE 195 REST OF MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY GLASS TYPE (USD BILLION) 2020-2029

TABLE 196 REST OF MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY GLASS TYPE (KILOTONS) 2020-2029

TABLE 197 REST OF MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY END USER (USD BILLION) 2020-2029

TABLE 198 REST OF MIDDLE EAST AND AFRICA FIBERGLASS ROVING MARKET BY END USER (KILOTONS) 2020-2029

LIST OF FIGURES

FIGURE 1 MARKET DYNAMICS

FIGURE 2 MARKET SEGMENTATION

FIGURE 3 REPORT TIMELINES: YEARS CONSIDERED

FIGURE 4 DATA TRIANGULATION

FIGURE 5 BOTTOM-UP APPROACH

FIGURE 6 TOP-DOWN APPROACH

FIGURE 7 RESEARCH FLOW

FIGURE 8 GLOBAL FIBERGLASS ROVING MARKET BY PRODUCT TYPE, USD BILLION, 2020-2029

FIGURE 9 GLOBAL FIBERGLASS ROVING MARKET BY GLASS TYPE, USD BILLION, 2020-2029

FIGURE 10 GLOBAL FIBERGLASS ROVING MARKET BY END USER, USD BILLION, 2020-2029

FIGURE 11 GLOBAL FIBERGLASS ROVING MARKET BY REGION, USD BILLION, 2020-2029

FIGURE 12 PORTER’S FIVE FORCES MODEL

FIGURE 13 GLOBAL FIBERGLASS ROVING MARKET BY PRODUCT TYPE, USD BILLION, 2021

FIGURE 14 GLOBAL FIBERGLASS ROVING MARKET BY GLASS TYPE, USD BILLION, 2021

FIGURE 15 GLOBAL FIBERGLASS ROVING MARKET BY END USER, USD BILLION, 2021

FIGURE 16 GLOBAL FIBERGLASS ROVING MARKET BY REGION, USD BILLION, 2021

FIGURE 17 NORTH AMERICA FIBERGLASS ROVING MARKET SNAPSHOT

FIGURE 18 EUROPE FIBERGLASS ROVING MARKET SNAPSHOT

FIGURE 19 SOUTH AMERICA FIBERGLASS ROVING MARKET SNAPSHOT

FIGURE 20 ASIA PACIFIC FIBERGLASS ROVING MARKET SNAPSHOT

FIGURE 21 MIDDLE EAST ASIA AND AFRICA FIBERGLASS ROVING MARKET SNAPSHOT

FIGURE 22 MARKET SHARE ANALYSIS

FIGURE 23 TAIWAN GLASS INDUSTRY CORP.: COMPANY SNAPSHOT

FIGURE 24 OWENS CORNING: COMPANY SNAPSHOT

FIGURE 25 CHINA BEIHAI FIBERGLASS CO. LTD.: COMPANY SNAPSHOT

FIGURE 26 SAINT-GOBAIN S.A.: COMPANY SNAPSHOT

FIGURE 27 AGY HOLDINGS CORP: COMPANY SNAPSHOT

FIGURE 28 BINANI INDUSTRIES LTD.: COMPANY SNAPSHOT

FIGURE 29 NIPPON ELECTRICAL GLASS CO. LTD.: COMPANY SNAPSHOT

FIGURE 30 TAISHAN FIBERGLASS INC.: COMPANY SNAPSHOT

FIGURE 31 JUSHI INDIA FIBERGLASS (P) LTD.: COMPANY SNAPSHOT

FIGURE 32 JOHNS MANVILLE: COMPANY SNAPSHOT

DOWNLOAD FREE SAMPLE REPORT

License Type

SPEAK WITH OUR ANALYST

Want to know more about the report or any specific requirement?

WANT TO CUSTOMIZE THE REPORT?

Our Clients Speak

We asked them to research ‘ Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te

Yosuke Mitsui

Senior Associate Construction Equipment Sales & Marketing

We asked them to research ‘Equipment market’ all over the world, and their whole arrangement was helpful to us. thehealthanalytics.com insightful analysis and reports contributed to our current analysis and in creating a future strategy. Besides, the te